Download

1 / 26

260 likes | 365 Views

Explore Thailand's postwar economy, the impact of the Asian crisis, and the recovery strategies implemented. Learn about macro management, financial reforms, foreign investment, corporate changes, and more. Discover the challenges and triumphs in Thailand's economic landscape.

E N D

Thai capital after the Asian crisis Pasuk Phongpaichit and Chris Baker A Decade After, Bangkok, 12-14 July 2007

Thailand: postwar to crisis • stable macro management • US tutelage • natural and human resources • immigrant entrepreneurs • competitive clientelism • high savings and investment • export orientation • domestic family conglomerates real per capita GDP

Crisis macro • IMF deflationary package (1 year) • consumer stimulus private consumption

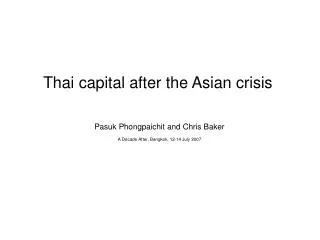

Finance • Collapse of credit culture • Surgery on financial institutions • Selective rescue • Lift bar on foreign investment • Regulation, prudence • Big four survive • Medium and small closed, sold, merged • End of relationship banking • 5-year shrinkage

Fig I.5 Distribution of commercial bank lending, 1990-2006 other overseas government consumer other commercial industry Source: Bank of Thailand

real sector • No policy to rescue • fire-sale of distressed assets • hands-off debt restructuring • lift equity restrictions in manufacturing • selective protection of services

Fig 1.1 Foreign direct investment, 1970-2006 % of GDP, right scale Source: Bank of Thailand

FDI • crisis decade vs boom decade: • x 3 in US$ • x5 in baht • x2 as % of GDP • export manufacturing • finance • construction-related (cement, steel) • big retail • property • services 1988: 122 of top 450 MNCs, 214 projects 2000: 248 of top 500 MNCs, 630 projects

Fig 3.1 Number of hypermarket outlets, 1995-2006 Carrefour Big C Tesco Source: Nipon et al., 2002 and corporate websites.

Companies • Quarter of companies de-listed from exchange • Quarter of top 50 corporate groups slid to bottom ranks • Quarter of top 220 corporate groups disappeared

Win or lose? Sector and structure • Sector • manufacturing partner • secondary finance • Structure • “authoritarian conglomerate” • (unreformed kongsi, absolute patriarch, little/no outside professional management, bank-dependent, non-transparent)

Impacts • Concentration • Export dependence • Capital market • Social development

Concentration • By MNC buyout/expansion • three mega-retail chains • two mobile phone suppliers • etc. • ‘Few winners, many losers’ effect • merger of steel firms • top five banks • liquor/beer • etc

Fig 1.5 Top 150 business groups by assets, 2000 Source: Suehiro database

export dependence • Recovery through exports • currency depreciated • companies reorient to export to replace home market • Almost all growth attributable to exports • Large and growing share by MNCs • Trade:GDP up from 90 to 150%

growth accounting Source: Peter Warr, 2005: 30

Fig I. 11 Export shares by sector, 1985-2006 tech-based industry process industry labour-intensive industry resource-based industry other agriculture

Fig I.10 Trade as percent of GDP, 1995-2006 Exports Imports

capital market • Decline in savings and investment • credit promotion to boost consumption • rising household debt, lower household savings • Banks shrink lending to business • reorient to consumer • Stockmarket no substitute • small, radically affected by speculative i/n flows • political manipulation • values do not reflect company performance

Fig I.8 Gross national savings, 1994-2005 Business Government Households Source : NESDB

Fig I.9 Gross domestic investment, 1994-2005 public private Source: NESDB

Fig I.5 Distribution of commercial bank lending, 1990-2006 other overseas government consumer other commercial industry Source: Bank of Thailand

urban informal white collar agriculture formal industrial other