Refinancing a VA Loan

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

Refinancing a VA Loan

E N D

Presentation Transcript

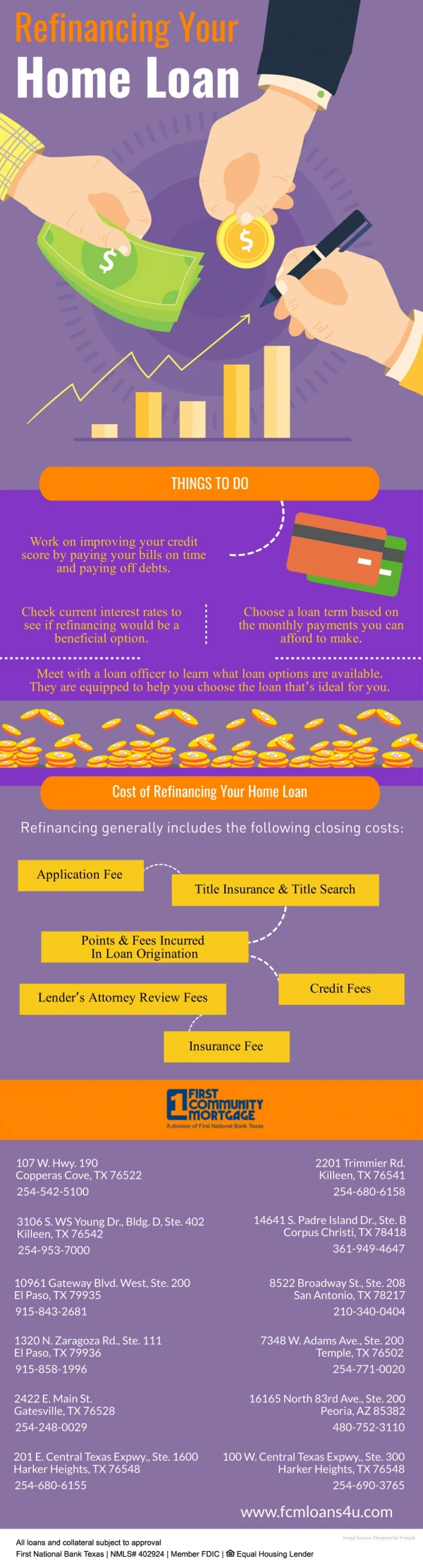

Refinancing a VA Loan Reasons for Refinancing a VA Loan There are many reasons to refinance your current mortgage loan. •Many refinances to take advantage of lower interest rates. Doing so allows them to reduce their monthly payment without adding to their total mortgage. •Others refinance to a shorter-term loan to pay of their home faster. By shortening the term of their loan, the monthly payment goes up and the home is paid for quicker, but much less is paid in interest over the course of the loan. •A third reason to refinance is to take advantage of equity gained in the home. The extra funds gained from a refinance can be used for home repairs, additions, debt consolidation, or children’s education. Some worry that refinancing takes too much time and money, but fortunately the process is simple. Refinancing is simply the process of paying of your existing loan with a new one. Your new loan could be for a better interest rate, a shorter/longer term, or a different amount. In fact, your new loan could be an entirely different type. For example, instead of an adjustable-rate mortgage you could opt for a fixed-rate mortgage. How do I Refinance My Existing Home Loan? The first step to refinancing your home is to identify why you are refinancing. •Do you want lower payments? •Do you want a shorter term? •Do you need extra money? Once you identify why you want to refinance then you are ready to select the proper type of mortgage for you. Some of your choices include: 15-YEAR FIXED-RATE REFINANCE Choose this if: •You want a shorter term and lower rates •Low monthly payments are not your goal •You’re planning to stay in your house for more than 10 years

ROLLDOWN OPTION Choose this if you want to refinance with few upfront fees. While the rate is slightly higher, you will pay only minor upfront fees for your new loan. If the roll-down rate is lower than your existing rate, it makes financial sense to refinance. CASH OUT OPTION If you have equity in your home, you can refinance for an amount higher than your current mortgage. You can use the difference for home improvement, debt consolidation, or whatever you want. 30-YEAR FIXED-RATE REFINANCE Choose this when: •You want low monthly payments that do not change •You want a loan that’s generally easier to qualify for •You’re planning to remain in your house less than 10 years •You want the maximum tax advantages How do I calculate the value of my property? Since a mortgage is secured by a piece of real property, getting a correct value is very important. Remember, property value can be determined in a few different ways. It can be valued based on the market value of the property. The market value is what a buyer will pay for it and what other “like” properties in the neighborhood have recently sold for. Value can also be determined based on the appraised value of the property. The appraised value is what a trained and licensed professional estimate the property to be worth based on an inspection of the property, its neighborhood, and the sale of other comparable homes in the area. After he determines the original value of the home, he then calculates the replacement value by reducing the original value due to factors like deterioration and depreciation. Can I make extra payments so I can pay off the loan more quickly? Depending on your specific loan, and what your state allows, it is often possible to make extra payments to shorten the life of your loan.

Extra payments applied directly to principle can have a huge effect on the amount of interest you ultimately pay.