Download

1 / 35

350 likes | 472 Views

VA Loans for Vets NMLS#184169<br>5050 North 40th Street, Ste 260<br>Phoenix, AZ 85018<br>602-908-5849<br><br>Jimmy Vercellino is one of the nationu2019s top VA Home Loan mortgage originators. A Marine veteran, he and his team work hard to help veterans take advantage of their VA loan benefit and become homeowners. From start to finish, they guide their clients through the process and make it as smooth and stress-free as possible. Visit the site at https://www.valoansforvets.com

E N D

Colloquially referred to as the GI Bill, the Servicemen’s Readjustment Act was passed by Congress in 1944. This act provided transition benefits for returning WWII veterans.

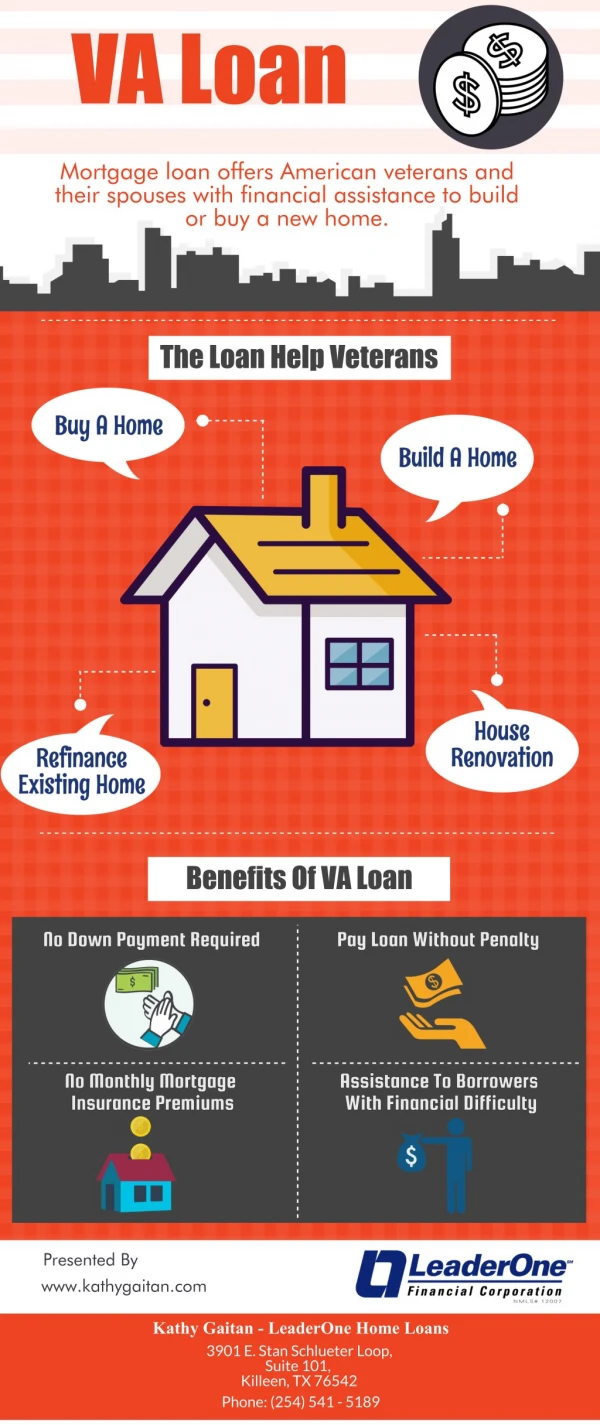

Benefits included: ✓Payments for tuition ✓Living expenses ✓Business loans at low interest rates ✓Low-interest mortgages ✓Nominal unemployment insurance

These benefits were available to all veterans who had met time-in- service requirements and had been discharged with other than a dishonorable discharge.

Of the original benefits in the bill, only the VA home loan guarantee program remains in effect.

From 1944 through 1993, almost 14 million home loans were guaranteed through the VA. The combined loan amounts totaled more than $433 billion.

The first step for veterans wanting to apply for a VA loan is to obtain a certificate of eligibility (COE).

This can be obtained online either at the VA's website or here on our site.

Obtaining a copy of the DD-214 is the second step. Again, it must show other than a dishonorable discharge.

The VA does not lend the money. It provides a guarantee to the lender that the money will be repaid, up to a specific dollar amount.

The guarantee amount can vary, depending on the area of the country.

Those areas with a high cost of living, such as San Francisco or New York City, will have a higher guarantee amount than a smaller town with a lower cost of living.

Once the veteran has these two documents, he or she can begin the process of purchasing a home using the VA home loan eligibility.

The home must be used as a primary residence. The applicant must have a valid COE.

A credit score high enough to qualify for the loan. And also must show income sufficient to make the payments.

VA home mortgages can be used to: ✓Buy a principal home ✓Manufactured home ✓Condominium

✓Buy a fixer-upper and make the necessary improvements ✓Construct a home ✓Make energy-efficient improvements

The program has changed somewhat in recent years. Veterans can now expect to pay some out-of-pocket expenses for some VA home loans.

Once the vet has established eligibility, he or she will need to find a lender. Not Not all financial institutions will lend on a VA loan.

Rates also will vary for interest, points, etc. So each veteran should shop for the best rate for his or her circumstances.

The lender will order an appraisal by the VA. This is not a guarantee of the home's value. Nor is it a home inspection.

All homes should receive a home inspection prior to documents being signed. This is for the veteran's protection.

Once a home is found, loan documents are submitted and reviewed. Then the lender will select a third party such as a title company or an escrow company to conduct the document signing.

Surviving spouses can be entitled to a VA home loan if they are the: ✓Un-remarried spouse of a veteran who died during his or her service or from disabilities incurred during time in service

✓Surviving spouse who remarried after the age of 57 ✓Spouse of a service member who is MIA or a POW

If a veteran has previously used their VA loan eligibility, he or she may be entitled to a restoration of benefit.

This makes them eligible to use the VA loan guarantee for a second time, if: ✓The previous property has been sold and the previous mortgage was completely paid off

✓Another qualified veteran assumes the loan and substitutes his or her loan eligibility for the VA loan guarantee

The VA home loan guarantee program is an excellent method for veterans to procure a home with minimal out-of-pocket costs.

Mortgage Originator Jimmy Vercellino, specializing in VA loans, helps veterans use their VA loan benefit to their greatest advantage.

Be a proud homeowner today. For more details call 480-351-5904 or visit the site www.valoansforvets.com

VA Loans for Vets VA Loans for Vets 7600 E. Doubletree Ranch Road #200 Scottsdale, AZ 85258 Phone: (480) 351-5904 Email: jimmyv@fcbmtg.com