Download

1 / 43

430 likes | 614 Views

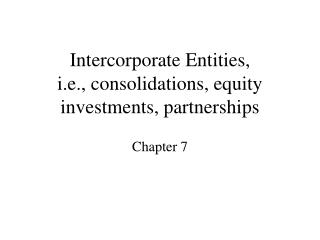

Baker / Lembke / King. Reporting Intercorporate Investments in Common Stock. 2. Electronic Presentation by Douglas Cloud Pepperdine University. Cost Method. Equity Method. Consolidation. Level of Common Stock Ownership. 0%. 20%. 50%. 100%. Significant influence. Control.

E N D

Baker / Lembke / King Reporting Intercorporate Investments in Common Stock 2 Electronic Presentation by Douglas Cloud Pepperdine University

Cost Method Equity Method Consolidation Level of Common Stock Ownership 0% 20% 50% 100% Significant influence Control Influence not significant

The Cost Method Investor Company purchases 20 percent of Investee Company’s common stock for $100,000 at the beginning of 20X1. Influence is determined to be not significant. Investment in XYZ Company Stock 100,000 Cash 100,000 Record purchase of XYZ Company stock.

20% of $20,000 The Cost Method During the year, XYZ has net income of $50,000 and pays dividends of $20,000. Cash 4,000 Dividend Income 4,000 Record dividend income from XYZ Company. Note that ABC records only its share of the distributed earnings of XYZ.

10% of $70,000 Liquidating Dividends Illustrated On January 2, 20X1, Investor Company purchases 10 percent of Investee Company’s common stock. Investee Company’s net income is $100,000 and dividends paid total $70,000. Cash 7,000 Dividend Income 7,000 Record receipt of 20X1 dividend from Investee Company.

10% of $120,000 Liquidating Dividends Illustrated On January 2, 20X2, Investee Company’s net income is $100,000 and dividends paid total $120,000. Thus, Investee had cumulative net income of $200,000 and paid cumulative dividends of $190,000. Cash 12,000 Dividend Income 12,000 Record receipt of 20X1 dividend from Investee Company.

10% of $120,000 ($310,000 - $300,000) x 10% 10% x ($120,000 - $10,000) Liquidating Dividends Illustrated For 20X3, Investee’s net income is $100,000 and $120,000 in dividends are declared and paid. Cumulative net income is now $300,000 and cumulative dividends paid total $310,000. Cash 12,000 Investment in Investee Company Stock 1,000 Dividend Income 11,000 Record receipt of 20X3 dividend from Investee Company.

Equity Method APB Opinion No. 18 requires that the equity method be used for reporting investments, other than temporary, in common stock...

Equity Method ...of the following: • Corporate joint ventures. • Companies in which the investor’s voting stock interest gives the investor the “ability to exercise significant influence over operating and financial policies” of that company.

Equity Method What is significant influence?

Equity Method APB 18 states, “An investment (direct or indirect) of 20% or more of the voting stock of an investee should lead to the presumption that in the absence of evidence to the contrary an investor has the ability to exercise significant influence over an investee.”

20% x $60,000 Equity Method--Recognition of Income ABC Company acquires significant influence over XYZ Company by purchasing 20 percent of the common stock of XYZ at the beginning of the year. XYZ reports net income of $60,000. Investment in XYZ Common Stock 12,000 Income from Investee 12,000 Record income from investment in XYZ Co.

20% x $20,000 Equity Method--Recognition of Dividends XYZ declares and pays a $20,000 dividend. Cash 4,000 Investment in XYZ Company Stock 4,000 Record receipt of dividend from XYZ.

Investment in XYZ Common Stock Dividends ($20,000 x .20) 4,000 Original cost 100,000 Equity accrual ($60,000 x .20) 12,000 Ending balance 108,000 Equity Method--Carrying Amount

Investment in XYZ Common Stock Dividends ($20,000 x .20) 4,000 Original cost 109,000 Equity accrual ($60,000 x 1/4 x .20) 3,000 Ending balance 108,000 Equity Method--Interim Acquisitions ABC Company acquires 20 percent of XYZ’s common stock on October 1 for $109,000. XYZ earns income of $60,000 and pays dividends of $20,000.

Cost of investment to Ajax $200,000 Book value of Ajax’s share of Barclay’s net assets (.40 x $400,000) (160,000) Differential $ 40,000 Equity Method--Cost Exceeds Book Value Ajax Corporation purchases 40 percent of the common stock of Barclay Company on January 1, 20X1, for $200,000. Barclay has net assets with a book value of $400,000 and a fair value of $465,000.

Excess of cost over fair value of net identifiable assets $14,000 Total differential $40,000 Excess of fair value over book value of net identifiable assets $26,000 Equity Method--Cost Exceeds Book Value Cost of Investment $200,000 Fair value of net identifiable assets (40% x $465,000) $186,000 Book value of net identifiable assets (40% x $400,000) $160,000

40% x $80,000 Equity Method--Cost Exceeds Book Value Barclay reports net income of $80,000 in 20X1. Investment in Barclay Stock 32,000 Income from Investee 32,000 Record equity-method income.

40% x $20,000 Equity Method--Cost Exceeds Book Value Barclay reports net income of $80,000 in 20X1. Investment in Barclay Stock 32,000 Income from Investee 32,000 Record equity-method income. Barclay declares and pays a dividend of $20,000 in 20X1. Cash 8,000 Investment in Barclay Stock 8,000 Record dividend from Barclay.

Equity Method--Cost Exceeds Book Value The $40,000 excess paid by Ajax is assigned to Land, $6,000, Equipment, $20,000, and Goodwill, $14,000. Equipment is amortized, but land and goodwill are not. Equipment ($20,000 ÷ 5 years) $4,000 Income from Investee 4,000 Investment in Barclay Stock 4,000 Amortize differential.

Equity Method--Disposal of Assets If Barclay had purchased the land in 20X0 for $75,000 and sells the land in 20X2 for $125,000. Barclay recognizes a gain on the sale of $50,000, and Ajax’s share is $20,000 (40%). Ajax’s share of Barclay's reported gain $20,000 Portion of Ajax’s differential related to land (6,000) Gain to be recognized by Ajax $14,000 Income from Investee 6,000 Investment in Barclay Stock 6,000 Remove differential related to Barclay’s land sold.

Equity Method--Purchase Additional Shares ABC Company purchases 20 percent of XYZ’s common stock on January 2, 20X1, and another 10 percent on July 1, 20X1, and the stock purchases are at book value. Income, January 2 to June 30: $20,000 x .20 $ 4,000 Income, July 1 to December 31: $30,000 x .30 9,000 Income from Investment, 20X1 $13,000 Investment in XYZ Stock 13,000 Income from Investee 13,000

January15, 20X1 Cash 2,000 Investment in XYZ Stock 2,000 July 15, 20X1 Cash 3,000 Investment in XYZ Stock 3,000 Equity Method--Purchase Additional Shares XYZ declares and pays a $10,000 dividend on January 15 and again on July 15. January 15 dividend: $10,000 x .20 $2,000 July 15 dividend: $10,000 x .30 3,000 Reduction in Investment, 20X1 $5,000

Zenon Investment Income Reported by Aron Originally under Restated under Year Net Income Dividends Cost Equity 20X1 $15,000 $10,000 $1,500 $2,250 20X2 18,000 10,000 1,500 2,700 20X3 22,00010,0001,5003,300 $55,000 $30,000 $4,500 $8,250 Equity Method--Change to Equity Method Aron Corporation purchases 15 percent of Zenon Company’s common stock on January 2, 20X1 and another 10 percent on January 2, 20X4. Aron switches to the equity method on January 2, 20X4.

$8,250 - $4,500 Equity Method--Change to Equity Method The investment account and retained earnings of Aaron are restated as if the equity method had been applied from the date of the original acquisition. Investment in Zenon Common Stock 3,750 Retained Earnings 3,750 Restate investment account from cost to equity method.

Cost and Equity Methods Compared Recorded amount of investment at date of acquisition. Cost Method Original cost

Cost and Equity Methods Compared Recorded amount of investment at date of acquisition. Equity Method Original cost

Cost and Equity Methods Compared Usual carrying amount of investment subsequent to acquisition Cost Method Original cost

Cost and Equity Methods Compared Usual carrying amount of investment subsequent to acquisition Equity Method Original cost increased (decreased) by investor’s share of investee's income (loss) and decreased by investor’s share of investee’s dividends and by amortization or write-off of the differential.

Cost and Equity Methods Compared Differential Cost Method Not amortized or written-off

Cost and Equity Methods Compared Differential Equity Method Amortized or written down if related to limited-life assets of investee or assets disposed of.

Cost and Equity Methods Compared Income recognized by investor Cost Method Investor’s share of investee’s dividends declared from earnings since acquisition

Cost and Equity Methods Compared Income recognized by investor Equity Method Investor’s share of investee’s earnings since acquisition, whether distributed or not, reduced by any amortization or write-off of the differential.

Cost and Equity Methods Compared Investee dividends from earnings since acquisition by investor Cost Method Income

Cost and Equity Methods Compared Investee dividends from earnings since acquisition by investor Equity Method Reduction of investment

Cost and Equity Methods Compared Investee dividends in excess of earnings since acquisition by investor Cost Method Reduction of investment

Cost and Equity Methods Compared Investee dividends in excess of earnings since acquisition by investor Equity Method Reduction of investment

APB 18--What is Significant Influence? An investor owning less than 20 percent can still have significant influence. APB 18 stated a number of factors that could indicate such influence. 1. Representation on board of directors. 2. Participation in policy-making. 3. Material intercompany transactions. 4. Interchange of managerial personnel. 5. Technological dependency. 6. Size of investment in relation to concentration of other shareholdings.

FASB InterpretationNo. 35 Evidence that an investor is unable to exercise significant influence over an investee: 1.Opposition by the investee. 2. The investor and investee sign an agreement in which the investor surrenders significant rights as a shareholder. 3. Majority ownership of the investee is concentrated among a small group of shareholders who operate the investee without regard to the views of the investor. 4. The investor, desiring more information than is available to the investee’s other shareholders, tries to obtain that information, and fails. 5. The investor tries and fails to obtain representation on the investee’s board of directors.

PSAK 13 Investasi Investasi : investasi lancar dan inestasi jangka panjang Harga perolehan ditentukan dengan nilai wajar aktiva yang diserahkan Investasi jangka panjang dicatat sebesar harga perolehan, jika ada penurunan yang bersifat tidak sementara dicatat mengurangi investasi

PSAK 15 : Investasi pada perusahaan asosiasi Pengaruh signifikan 20% Dicatat dengan menggunakan metode ekuitas jika ada pengaruh signifikan Walaupun lebih dari 20% tetap metode cost jika : pembatasan yang ketat sehingga mengurangi kemampuan mengalihkan dana pada investor Pengungkapan daftar dan penjelasan dari perusahaan asosiasi (nama, tempat, kedudukan, jumlah kepemilikan) metode yang digunakan untuk mempertanggungjawabkan investasi tersebut

KUIS PT. Kenanga membeli 30% kepemilikan PT. Anggrek pada 1 April 2003 dengan menerbitkan saham sebanyak 1000.000 dengan nilai par 100 dan harga pasar 320. Saat pembelian ekuitas PT. Anggrek terdiri dari common stock 500.000.000, additional paid in capital 100.000.000 dan retained earning 300.000.000. Berikut asset yang memiliki perbedaan nilai buku dan nilai wajar nilai buku nilai wajar Tanah 100.000.000 200.000.000 Bangunan (10) 200.000.000 240.000.000 Peralatan (4) 130.000.000 100.000.000 Hutang jk panjang (5) 100.000.000 120.000.000 Selama tahun 2003 laba PT. Anggrek 120.000.000, deviden 10 juta (Februari) dan 40 juta (September). Buat jurnal selama tahun 2003 dan hitung nilai investasi 31/12/03

Chapter Two Chapter Two The End