Download

1 / 22

220 likes | 415 Views

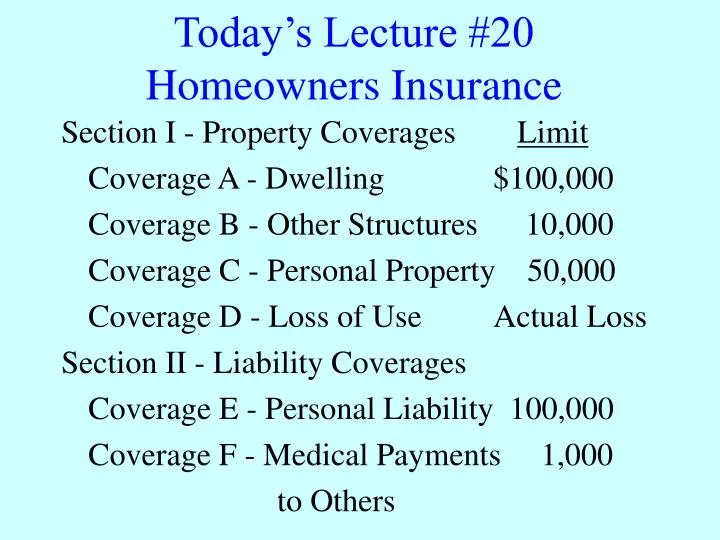

Today’s Lecture #20 Homeowners Insurance. Section I - Property Coverages Limit Coverage A - Dwelling $100,000 Coverage B - Other Structures 10,000 Coverage C - Personal Property 50,000 Coverage D - Loss of Use Actual Loss Section II - Liability Coverages

E N D

Today’s Lecture #20Homeowners Insurance Section I - Property Coverages Limit Coverage A - Dwelling $100,000 Coverage B - Other Structures 10,000 Coverage C - Personal Property 50,000 Coverage D - Loss of Use Actual Loss Section II - Liability Coverages Coverage E - Personal Liability 100,000 Coverage F - Medical Payments 1,000 to Others

Deductible Policy Deductible for Section I $250 This deductible applies only once to each loss. Apply deductible first, then policy limits.

Example If $60,000 of your personal property is stolen, calculate the loss as follows: Loss 60,000 Deductible 250 Loss less deductible 59,750 Policy limit 50,000 Covered loss 50,000

Definitions Insured means you and residents of your household who are: 1. Your relatives 2. Other persons under the age of 21 and in the care of any person named above

Insuring Clause Coverages A and B - Open perils - Covers all risks subject to limitations and exclusions Coverage C - Named perils

Section I Loss Settlement(Page 676) Actual cash value, not to exceed cost of repair or replacement: Personal Property Awnings, carpeting, household appliances, outdoor antennas and outdoor equipment, whether or not attached to buildings Structures that are not buildings

Section I Loss Settlement(Page 676) Replacement Cost subject to 80% coinsurance clause: Buildings under coverages A and B

Homeowners Example - 1 A fire causes damage to your house and your furniture. The amount of damages are: Replacement Cost ACV House 20,000 15,000 Furniture 6,000 3,000 How much will your Homeowners Policy pay? Assume the replacement cost of the entire house is less than $125,000.

Answers A) 18,000 B) 21,000 C) 23,000 D) 26,000 E) None of the above

Examples of Coverage A and B Exclusions • Freezing of plumbing while dwelling is unoccupied unless you have used reasonable care to maintain heat • Vandalism and malicious mischief to dwelling vacant more than 30 days • Smog, rust or other corrosion, mold, wet or dry rot • Birds, vermin, rodents or insects • Animals owned or kept by an insured

Homeowners Example - 2 You travel to China for six weeks. When you return you find that your home has been vandalized by spray paint on the walls. It costs $20,000 to repair the damage. How much will your policy pay? A) 0 B) $19,750 C) $20,000 D) None of the above

Coverage C - Personal Property 16 Named Perils (Pages 673-674) plus Collapse (Page 671) Examples of Covered Perils Fire Windstorm or hail Vehicles Vandalism and malicious mischief

Coverage C Covered PerilsContinued Theft, unless Committed by an insuredIf in dwelling under construction From area rented to others Property at other residence if not currently living there, except for a student as long as the student has been there any time within the 45 days prior to the loss

Homeowners Example - 3 While your son is home for Thanksgiving break, someone steals his laptop computer from his dorm room. The computer costs $2000 to replace. It had an Actual Cash Value of $750. How much will your policy pay? A) 0 B) $500 C) $750 D) $1750 E) None of the above

Special Limits on Personal Property (Page 668) 10% ($5000) on property usually located at an insured’s residence, other than residence premises $200 on money, gold, silver, etc. $1000 on securities, tickets, stamps $1000 on watercraft $1000 on loss by theft of jewelry, watches, furs, precious and semi-precious stones $2000 on loss by theft of firearms

Special Limits - Continued $2500 on silverware $2500 on property used in business while on residence premises $250 on property used in business while away from the residence premises

Homeowners Example - 4 Your fishing boat is destroyed in a fire. The boat costs $5000 to replace. It had an Actual Cash Value of $2000. How much will your policy pay? A) 0 B) $750 C) $1000 D) $1750 E) None of the above

Examples of Property Not Covered Under Section C(Page 669) • Animals, birds, fish • Motor vehicles • Aircraft

Homeowners Example - 5 Someone steals your prize rare breed rabbit. It costs $1500 to replace your rabbit. The rabbit had an Actual Cash Value of $500. How much will your policy pay? A) 0 B) $250 C) $500 D) $1250 E) None of the above

Coverage D - Loss of Use If a covered loss renders the residence premises unfit to live in, policy covers Additional living expenses or Fair rental value This is paid for the shortest time necessary to repair of replace damage or until permanent relocation.

Examples of Additional Coverages(Pages 670-672) Debris removal (could increase limit of liability by 5%) Trees, Shrubs, Plants and Lawns - Covered only for: Fire or lightning Explosion Riot or civil commotion Aircraft Vehicles not owned or operated by resident Vandalism or malicious mischief Theft 5% limit in total, no more than $500 per item Credit Card, Fund Transfer Card, Forgery and Counterfeit Money $500 Limit - No Deductible

Additional Section I Exclusions(Pages 674-675) Ordinance or law Earth movement Water Damage Power failure Neglect War Nuclear hazard Intentional loss