Download

1 / 7

70 likes | 192 Views

Breakeven Analysis. Quantitative Tool for Evaluating Alternatives. Breakeven Analysis. Organizations face Variables Costs (VC). Variable Costs (VC) change with the volume of production, e.g. cost of materials or labor. Organizations face Fixed Costs (FC).

E N D

Breakeven Analysis Quantitative Tool for Evaluating Alternatives

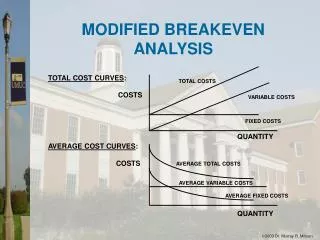

Breakeven Analysis • Organizations face Variables Costs (VC). • Variable Costs (VC) change with the volume of production, e.g. cost of materials or labor. • Organizations face Fixed Costs (FC). • Fixed Costs (FC) do not change with volume of production and would be incurred even if no products were manufactured or sold, e.g. Utilities, Advertising and Sales Expenses, Machinery. • Price (P) per Unit is the revenue obtained per unit. • Unit Contribution or Margin per Unit is the difference between price per unit and variable cost per unit, i.e. • Unit Contribution = P per unit – VC per unit • Breakeven volume is found by dividing the total fixed costs by the unit contribution • Breakeven Volume (Units) = Total Fixed Costs • Unit Contribution

Break Even Analysis • Breakeven occurs when Total Costs = Total Revenues • Total Costs = Fixed Costs + Variable Costs • If TC are greater than TR than loss is incurred. • If TR are greater than TC than profit is incurred. • Typically TR are less than TC at beginning stages of production • Raising prices will reduce BEP. • Lowering prices will increase BEP.