Reserving for Incomplete Accident Years: Insights from Nancy P. Watkins and Associates

110 likes | 219 Views

This document outlines the evaluation of loss reserves specifically for incomplete accident years, focusing on methodologies used beyond the traditional December 31 evaluation date. It details various motivations for these assessments, including internal and external reporting needs, special business situations, and general approaches for accurately adjusting loss reserves. Different scenarios illustrate applicable methods such as loss development factors, loss ratio methods, and regrouping data techniques, providing a comprehensive framework for actuarial analyses in diverse contexts.

Reserving for Incomplete Accident Years: Insights from Nancy P. Watkins and Associates

E N D

Presentation Transcript

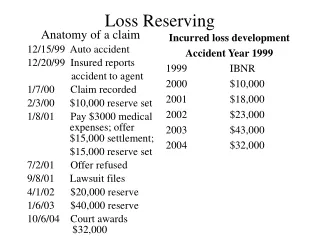

Reserving for Incomplete Accident Years Nancy P. Watkins Milliman & Robertson, Inc. CLRS - September 28-29, 1998

Reserving for Incomplete Accident Years • Refers to the evaluation of loss reserves as of a date other than December 31 • Does not refer to the projection of December 31 loss reserves based on data through a different evaluation point

Why Reserve for Incomplete Accident Years? • Internal reporting to management: • How are we doing year-to-date? • External reporting: • Shareholders • Regulators

Why Reserve for Incomplete Accident Years? • Special situations: • Rate review • Merger or acquisition • New company • New line of business • Line of business in runoff • Company fiscal year different from calendar year

General Approach to Incomplete Accident Years • Can start with previous year-end review (Scenario I) and make adjustments to accident year methods (Scenarios II, III) • Can apply same methods to regrouped data (Scenarios IV, V and VI)

General Approach to Incomplete Accident Years • “Methods” can refer to: • Losses or ALAE as underlying data • Paid or reported loss development • Paid or reported Bornhuetter-Ferguson • Claim counts and average severities • Many other methods as well

Examples of Methods: Scenario II • For complete years (1990-96), use same LDFs and ultimates as for previous year-end review (Scenario I) • For incomplete year (1997), use Loss Ratio Method, with selected ultimate loss ratio based on prior years • Subtract reported loss as of evaluation date to derive estimated IBNR

Examples of Methods: Scenario III • For complete years (1990-96), use interpolated LDFs based on LDFs from previous year-end review; apply to losses as of evaluation date • For incomplete year (1997), estimate a LDF based on some formula applied to 12-ultimate LDF; or • For incomplete year (1997), use Loss Ratio Method, with selected ultimate loss ratio based on prior years

Examples of Methods: Scenario IV • Regroup data into accident quarters evaluated at 3 months, 6 months, 9 months, etc. • Apply method to accident quarters in same way as to accident years

Examples of Methods: Scenario V • Regroup data into accident years evaluated at 9 months, 21 months, 33 months, etc. • Apply method to regrouped accident years in same way as to accident years at 12, 24, etc. except • Ultimate loss for incomplete accident year (1997) must be adjusted to exclude future exposures (4th quarter 1997)

Examples of Methods: Scenario VI • Regroup data into fiscal-accident years (10/1/x - 9/30/x+1) evaluated at 12 months, 24 months, 36 months, etc. • Apply method to regrouped fiscal-accident years in same way as to accident years • Ultimate loss for incomplete accident year (1997) does not need to be adjusted to exclude future exposures (4th quarter 1997)