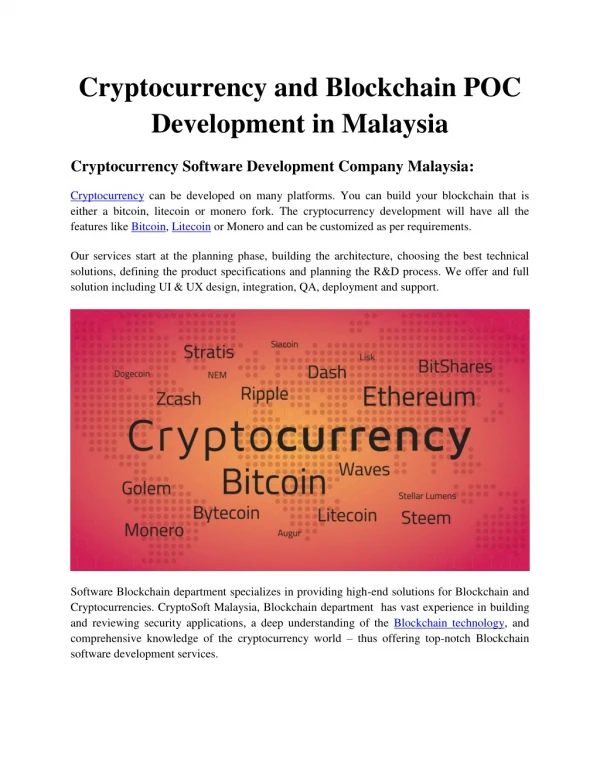

Download

1 / 13

190 likes | 928 Views

Economic and Accounting Development in Malaysia. Introduction. Patterns of accounting development can be traced to stages of economic growth (Singhvi, 1992) Role of state is crucial for accounting and economic development.

E N D

Introduction • Patterns of accounting development can be traced to stages of economic growth • (Singhvi, 1992) • Role of state is crucial for accounting and economic development. • Malaysia-colonial impact, ethic group occupation and post colonial era.

Economic and Accounting in Malaysia • RMK 1 - 1966-1970, RMK 9- 2006-2010. • RMK 10 - 2011-2015. • Economic planning-to enhance the business growth, eradicate poverty and balance the socio economy. • 1958-MACPA was incorporated, instituted in 1961. • 1965- Companies Act • 1967- MIA

New Economic Policy • NEP- export-oriented industries like free trade zone • 1960- Four stockbrokers at central Bank. • 1964- Malayan Stock Exchange • 1965- Stock Exchange of Malaysia and Singapore • 1973-Kuala Lumpur Stock Exchange • 1974-Corporate Financial Reporting in Malaysia is published. • 2000s- Bursa Malaysia

International Accounting Standard (IAS) • 1978- IAS 1 to 4 were adopted by MACPA. • 1979- IAS 5-10 were adopted • Until 1986- 13 IAS s were adopted • MACPA- close rapport with government and its agencies for mutual benefits and material interest.

Fourth Malaysian Plan (1981-1985) • Due to economic recession, Malaysian Economy is slow- GDP growth rate is 5.8% p.a. – high public sector and budget deficit. • Review the 4thMP-create privatization for capital market growth • 1981-Amanah Saham Nasional (PNB) • Amended 1984 Companies Act- include Accounts as Profit and Loss Account and Balance Sheet. • 1984- issued Malaysian Accounting Standards -MASs

Fifth Malaysian Plan (1986-1990) • Privatization- more for SMIs and reduce strains during recession. • 1986-Amendment to Companies Act 1965 • 1987-Malaysian Institute of Accountants – MIA – to increase number of accountants. • 1988-MACPA issue Malaysian Auditing Guideline- MAG • 1990-Malaysian Association of Accounting Technicians ( MAAT)-1990

Sixth Malaysian Plan (1991-1995) • National development policy-NDP • Emphasize on Economic growth, political stability, national unity • Aim to eradicate poverty and restructure society. • Industrial restructuring-high tech industry, capital and technology intensive. • Malaysian Institute of Taxation (MIT)-1991 • MACPA Guidelines for Accounting in Public Sector- Jan 1992

Capital Market • The capital market increase share of investment funds for public and private sectors • 1991 : RM 9.4 billions • 1992 : RM 13.8 billions- net funds raised • Private sector was dominant than public sector - 66% in 1991, 89% in 1992 • Audit committee was set up to ensure financial integrity of all listed companies. • 1993-Securities Commission was set up to foster the development of capital market, safeguard public interest & minority shareholders, and maintain integrity & efficiency.

State and Interest Groups • Malaysian economy has gradually changed: • 1957- rubber and tin exporter • 1960s – govt. focus on rural development and infrastructure • 1970s-state intervene in agricultural and rural development ( NEP target 30% equity for Bumiputra community) • 1980s-expansion of state enterprise sector and privatisation. • 1990s- manufacturing and high-tech industries

Accounting and Economic Development • 1960s-Economic growth provide the need to regulate accounting profession. • 1972-MACPA issue statement of disclosures • 1973-KLSE amd diversification of economy • 1976-Statement of statutory accounts • 1980s- Recession in early 1980s – raised issue on the quality of accounting and auditing standards. Various accounting standards are issued e.g. guideline and code of ethics.

Need funds for manufacturing (1956-65) Treasury function (1966-70) Bookkeeping emphasized (1971-75) Financial reporting and disclosures are emphasized- MAS 1-EPFS, MAS 2, Merger accounting (1976-85) Improved financial reporting (1986-90) Accountants responsible for financial activities & control Audit committees Accountants-bookkeeping role(1991-95) Accounting standards Development in Accounting

Conclusion • State needs to examine the domestic policies in shaping national development. • State needs to intervene the national economic rationality against the short term interest of private sector.