Macro v Micro

Economics deals with the allocation and distribution of scarce (finite) resources. Finite resources refers not simply to goods, but time. Macro v Micro.

Macro v Micro

E N D

Presentation Transcript

Economics deals with the allocation and distribution of scarce (finite) resources. Finite resources refers not simply to goods, but time.

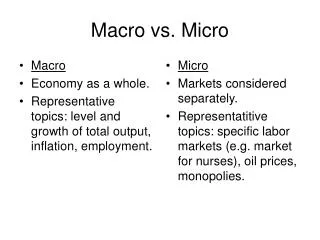

Macro v Micro • Micro -Individual/consumers and how they choose what to consume and how much of it and Businesses and how they as firms and industry decide what to produce and how much • Macro- Economy as a whole, How much is produced, what is produced, what is the price level of goods, how much money can flow into the economy without producing inflation/deflation, what level of employment is optimal to insure full production without producing inflation/deflation.

Economic Analysis • Models/paradigms/Assumptions- economic analysis requires economists to try to resolve questions about real world behavior by simplifying the world so that cause and effect can be measured consistent with the scientific method.

To do that, economists make certain presumptions about human behavior (more is better than less) individual interest guides us. In order to isolate a dependent and independent variable (social science) it’s necessary to hold the rest of the variables static (unchanged).

Assumptions typically made in economics include, rational behavior and perfect information. When we look at the effect of a price change on the quantity demanded by consumers, we hold static, a host of variables such as taste, income, substitutes/complements etc..

Yes…but… • What is the value of economic analysis if so many variables that can’t be held constant, are? • Are the basic assumptions accurate • Perfect information? • Rational Behavior • Alan Greenspan thought so----but----

Value of Models • Models allow economists to predict outcomes. However the assumptions limit the applicability of those predictions. • But you must acknowledge the limits!

Marginal v. Absolute • The temperature today is 82 degrees and its hot outside • The temperature today is 65 degrees and its comfortable • The temperature today is 98 degrees and its comfortable • How can they all be true? Assume

Economists are primarily concerned with how a change in one variable will lead to subsequent events (cause and effect). To ascertain whether cause and effect occurred it’s necessary to measure the change. Economists are not interested in absolutes

Causation v. Correlation • What’s the difference?? • Roll a die- likelihood of a six? • After 5 rolls? • Causation v. Correlation • Causation- a -> b • Litmis paper is turned red by an acid • Correlation; (b) generally follows (a) • When an original NFL team wins the Super Bowl the stock market goes up • Every country that has invaded Afghanistan has lost • Correlation may also mean Causation

Repeated tests of the experiment may help to differentiate btw correlation and causation • The degree of causation is often relevant- • Economists are less interested in absolute than change • Are interested in incremental change---Marginal analysis– How much more…How much less

How many people play piano or knit scarves is not particularly relevant without more info. Whether more people are playing piano or knitting scarves and what is the cause of that may be relevant. If the change is substantial it may be more relevant or show a stronger correlation • Marginal Analysis- how strongly is one variable associated with another. The stronger the correlation (1:1) the more predictive.

Opportunity Cost • Because of finite resources/time/goods etc… • People must constantly make decisions choosing one idea/thing/action over another. We call the cost of a decision Opportunity Cost. To the degree we can measure that cost it makes it more applicable for analysis. To simplify we give some things numbers (quantitative analysis)- ie whether something is leisure or not the authors created a scale 1 to 10, Money is one way to measure a trade off.

Measuring • ordinal v. cardinal- Ordinal- placing things in order rank…Cardinal giving them a quantitative measure • Marginal change- how do you measure- change • Graphically slope- relationship indep v. dependent variable

Utility • The degree of satisfaction/use a product or a course of action gives you. • Difficult to quantify • Yet economists do….Why because it’s the only way to test an idea