Download

1 / 8

140 likes | 735 Views

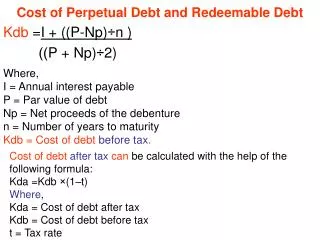

Cost of Perpetual Debt and Redeemable Debt. Where, I = Annual interest payable P = Par value of debt Np = Net proceeds of the debenture n = Number of years to maturity Kdb = Cost of debt before tax. Kdb = I + ((P-Np)÷n ) P + Np)÷2) )).

E N D

Cost of Perpetual Debt and Redeemable Debt Where, I = Annual interest payable P = Par value of debt Np = Net proceeds of the debenture n = Number of years to maturity Kdb = Cost of debt before tax. Kdb =I + ((P-Np)÷n ) P + Np)÷2))) Cost of debt after tax can be calculated with the help of the following formula: Kda =Kdb ×(1–t) Where, Kda = Cost of debt after tax Kdb = Cost of debt before tax t = Tax rate

Exercise A company issues $ 2000,000, 10% redeemable debentures at a discount of 5%. The costs of floatation amount to $ 50,000. The debentures are redeemable after 8 years. Calculate before tax and after tax. a tax rate of 55%. Solution Kdb =I + ((P-Np)÷n ) (P + Np)÷2) = 200000 + ((2000000- 1850000) ÷ 8) ((2000000 + 1850000 ) ÷2) =200000 +18750 = 11.36% 1925000 Kda =Kdb ×(1–t) Kda = 11.36% ×(1–55%) = 5.11%

Exercise • A company issues 9% redeemable debentures at a premium of 20%. , 500$ Par value of a debenture , The costs of floatation is 5% from the Par value. The debentures are redeemable after 12 years. Calculate before tax and after tax. a tax rate of 25%. • Solution • Np = 500 + 100 – ( 5%×500) = 575 Kdb =I + ((P-Np)÷n ) (P + Np)÷2) Kdb = 45 + (( 500 – 575 ) ÷ 12 ) = 38.75 7.2% (( 500 + 575 )÷ 2) 537.5 Kda =Kdb ×(1–t) Kda = 7.2% ×(1–25%) = 5.4%

Cost of Preference Share Capital There are two types of preference shares irredeemable and redeemable. Cost of irredeemable preference share capital is calculated with the help of the following formula: Kp = Dp ÷ Np Where, Kp = Cost of preference share Dp = Fixed preference dividend Np = Net proceeds of an equity share Cost of redeemable preference share is calculated with the help of the following formula: Kp = Dp + ((P- Np) ÷ n) ((P +Np) ÷ 2) Where, Kp = Cost of preference share Dp= Fixed preference share P = Par value of debt Np = Net proceeds of the preference share n = Number of maturity period.

Exercise (irredeemable preference share ) XYZ Ltd. issues 20,000, 8% preference shares of $ 100 each. Cost of issue is $ 2 per share. Calculate cost of preference share capital if these shares are issued (a) at par, (b) at a premium of 10% and (c) of a at a discount of 6%. Solution Kp = Dp ÷ Np (a)= Kp = ( 20000 × 100) × 8% = 160000 = 8.16% 2000000 – 40000 1960000 (b)= Kp = ( 20000 × 100) × 8% = 160000 =7.40% 2000000 +200000 – 40000 2160000 ( c) Kp = (20000 × 100) × 8% = 160000 =8.69% 2000000 -120000 – 40000 1840000

Exercise (redeemable preference share ) ABC Ltd. issues 20,000, 8% preference shares of $ 100 each. Redeemable after 8 years at a premium of 10%. The cost of issue is $ 2 per share. Calculate the cost of preference share capital. Solution Kp = Dp + ((P- Np) ÷ n) ((P +Np) ÷ 2) Np= 2000000 + 200000 – (2× 20000) = 2160000 Kp = 160000 + (( 2000000 – 2160000) ÷ 8)= ((2000000 +2160000 ) ÷ 2) = 160000 – 20000 = 6.73% 2080000

Cost of Retained Earnings Retained earnings is one of the sources of finance for investment proposal; it is different from other sources like debt, equity and preference shares. Cost of retained earnings is the same as the cost of an equivalent fully subscripted issue of additional shares, which is measured by the cost of equity capital. Cost of retained earnings can be calculated with the help of the following formula: Kr = Ke ( 1-t) (1-b) Where, Kr=Cost of retained earnings Ke=Cost of equity t=Tax rate b=Brokerage cost

Exercise A firm’s Ke (return available to shareholders) is 10%, the average tax rate of shareholders is 30% and it is expected that 2% is brokerage cost that shareholders will have to pay while investing their dividends in alternative securities. What is the cost of retained earnings? Solution Kr = Ke ( 1-t) (1-b) So, Kr = 10% (1–0.3) (1–0.02) = 10%×0.7×0.98 = 6.86%