Download

1 / 27

270 likes | 414 Views

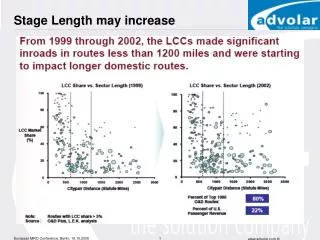

Stage Length may increase. LCC Market Share in Europe LCCs and the Future of the Business Model Drivers of the Business Model LCCs and MROs Conclusion. Agenda. LCCs Develop Different Market Strategies. Pure Low Cost Carriers Year round traffic Independent travelers

E N D

LCC Market Share in Europe LCCs and the Future of the Business Model Drivers of the Business Model LCCs and MROs Conclusion Agenda

LCCs Develop Different Market Strategies • Pure Low Cost Carriers • Year round traffic • Independent travelers • Balanced directional flows • Grow the market • Avoid charter markets (for the time being!) • Hybrid Models • Mix of business and leisure • “A la carte” services • Compete in some charter markets -Hot meals, -Lounges, -Paper tickets -Business -Branding -Low Fre- quency -Branded meals -Main Airports -Frequency -Branding -Low-Fares -Frequency

Migration of business models Charter Airlines Full Service Airlines LCCs

Migration of business models Charter Airlines Full Service Airlines Hybrids Hybrids LCCs

Positioning of LCCs Quality-conscious business passengers Price-conscious business passengers Non-business passengers Regional airlines LCCs Short-haul routes Charter Long-haul routes Network carrier Source: Mercer Management Consultants 2003

LCCs will continue to grow. Market share of 35% in 2010 seems not unrealistic. LCCs will move into leisure destinations (sector length max 2-3 f‘hrs) where traditional charter carriers have a significant „seat only“ business. LCCs will increase frequency on leisure routes but will reduce the number of departure airports. LCCs will adopt quality elements or product features from Full Service/Charter Airlines provided costs and complexity will not increase or they are providing another revenue stream (FFPs, IFE, seat reservation etc.) LCCs will enter into arrangements with tour operators provided their business model will not be affected. Migration and Segmentation

LCC Market Share in Europe LCCs and the Future of the Business Model Drivers of the Business Model LCCs and MROs Conclusion Agenda

Operation • Short Turn around Time • High reliabilty • Excellent T/S and MEL-Management • High Utilization – Low Saisonality • Equalized maintenance program • Maintenance program calendar time driven • Letter Checks outside standard maintenance periods • Low f‘hr/cycle ratio • Engine maintenance cycle driven • High load factor • Cabin wear and tear • No Hot Meal service, No IFE • Spares provisioning • Basing Concept

Aircraft Basing Concepts • National / flag carrier usually have one or two national bases only

Ryanair • LCCs have a pan European basing concept

Ryanair and Easyjet • LCCs have a pan European basing concept

Fleet • Homogenous Fleet • Overall maintenance costs (spares holding, engineering etc.) • No Stand-By Aircraft • High reliability • Ownership: Mostly Leased Aircraft • Mod policy • Spares Pool Exchange

Image Transfer • LCCs have a latent image problem: Low Cost = Low Safety • Contracting with a „Blue Chip“ in the MRO industrie reflects positively on the LCC

LCC Market Share in Europe LCCs and the Future of the Business Model Drivers of the Business Model LCCs and MROs Conclusion Agenda

The Low Cost Idea Can be Adoptedby the MRO Industry Low-cost means... ...not simply reducing the price for doing what always has been done, ...but primarily changing well-known processes. The simplicity of the new processes is key. The low-cost idea has to start in people´s mind!

Song‘s Credo We are not an airline, we are a culture. A culture founded by optimists - and built by believers. We are not an airline. We are listeners, innovators and technology creators. We are not an airline. We are magicians, musicians, acrobats and sprinters focused on a single goal: to give style, service and choice back to the people who fly. That´s why we „cast“ our stars - to make sure each and every one is attentive and gracious. Why we offer everyone 24 channels of real time, satellite TV and CD quality MP3 audio. Why we hand picked a socially-conscious chef - to prepare fresh meals and cater to diverse tastes. Why Kate Spade designed a collection for our stars, why we created exlusive programming for families, and offer cosmopolitans in the air. All in all, it´s why we offer more. And now it´s time to dig deeper. You see, we realize our difference doesn´t lie solely in the choices we offer, but also in how we offer them. ...

LCC Requirements • New thinking when offering services to LCCs. LCC culture is open minded. Leadership is not necessarily having airline background! „New frontiers“ are a challenge not a risk! • For LCCs there is little incentive to take on board anything other than line maintenance work. What LCCs really do well is flying passengers from A to B, develop products and grow markets, manage yield and revenue • LCCs want „air time“, suppliers want ground time. There´s a conflict of interest, less incentive for suppliers to „improve“ themselves Source: „Service Challenge“, Airline Business, October 2004

„Equalized“ maintenance concepts to assure shorter ground time and higher availability of the aircraft Suppliers should maximize the benefits from the „Data Pool“ they have built up during hundreds of checks e.g. knowledge of most frequently used material (pre-kitting), repair schemes etc. Cost reductions will have to come from smarter maintenance planning Doing the right work at the right time and not over-maintaining LCC Requirements

Small Engineering organisations require more support than traditional airlines: SB-evaluation, Documentation, Tech Records etc. LCCs are not interested in maintaining huge spare inventories. „Spares by the hour“ converts fixed costs into variable costs. Pre-kitted material for all checks, major component changes for all a/c models are available from specialized suppliers LCCs are not looking at how to increase fares if costs are going up. LCCs are turning every stone to reduce costs further. MROs negotiating a long term contract with a LCC should not offer complex Escalation Clauses but a Productivity Improvement Program. Benefits to be shared with the airline. Rates should be split into Euro (labour) and US Dollar (material) LCC Requirements

LCC Market Share in Europe LCCs and the Future of the Business Model Drivers of the Business Model LCCs and MROs Conclusion Agenda

LCCs in Europe and will continue to grow 35% market share in 2010 LCCs will continue to outsource maintenance services Maintenance volume will be affected by young fleet New Generation aircraft require less m‘hrs/bay day! MROs are invited to re-engineer processes in order to be more cost effective. They are not expected to deliver the standard poduct cheaper! MROs have to deliver pan european (pipe line management!) and dependable services. Productivity gains to be shared with the customer. Conclusion