Download

1 / 21

640 likes | 2.03k Views

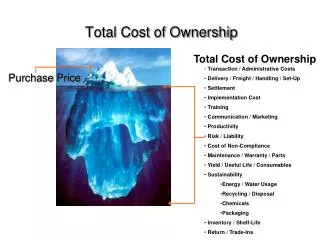

Total Cost of Ownership. Total cost of ownership is a philosophy for really understanding all supply chain related costs of doing business with a particular supplier for a particular good or service (Lisa Ellam, May 1999). TCO. 13-3. Key Concepts. Three Components of Total Cost Acquisition Costs

E N D

2. Chapter 13 Total Cost of Ownership

3. Total Cost of Ownership Total cost of ownership is a philosophy for really understanding all supply chain related costs of doing business with a particular supplier for a particular good or service (Lisa Ellam, May 1999)

4. Key Concepts

Three Components of Total Cost

Acquisition Costs

Ownerships Costs

Post-Ownership Costs

Purchase Price: But One Component of Cost

5. Key Concepts

TCO, Net Present Value Analysis (NPV), and Estimated Costs

The Importance of Total Cost of Ownership in Supply Management

Service Providers

Retail

Manufacturing

6. Three Components of Total Cost

Acquisition Costs

Ownerships Costs

Post-Ownership Costs

7. TCO Components Acquisition costs

Purchase price

Planning costs

Quality costs

Taxes

Financing costs

Ownership costs

Downtime costs

Risk costs

Cycle time costs

Conversion costs

Non-value added costs

Supply chain costs Post-ownership costs

Environmental costs

Warranty costs

Product liability costs

Customer dissatisfaction costs

8. Acquisition Costs Purchase Price

Planning Costs

Quality Costs

Taxes

Customs Duties and Tariffs

Regional Trade Agreements

Income-Base Shifting

Financing Costs

9. Ownership Costs

Downtime Costs

Risk Costs

Cycle Time Costs

Conversion Costs

Non-Value Added Costs

Supply Chain Costs

10. Ownership Costs Supply Chain Costs

Forecasting

Administration

Transportation

Inventory

Manufacturing

Customer service

Supplier selection/relationships

Global sourcing

11. Post - Ownership Costs

Environmental Costs

Warranty Costs

Product Liability Costs

Customer Dissatisfaction Costs

12. TCO, Net Present Value Analysis (NPV), and Estimated Costs NPV analysis is frequently incorporated into TCO analyses

NPV analyzes present values of the initial expenditure along with the likely future revenue and expenditure streams

The present value of a sum of future cash flows discounted by a required rate of return

NPV greater than zero suggests accepting the investment

NPV less than 0 suggests rejecting the investment

NPV = 0 is the point of indifference

13. Tangential Reprographics Example

14. TCO Formula

15. PVA Incorporated into a TCO Analysis

16. PVA Formulas PVAnnuity = CF [ 1/r � 1/r(1+r)t ]

CF = periodic cash inflow or outflow (must be the same each period)

r = discount rate per period (annual rate divided by the number of periods in one year)

t = total number of periods

PV = FV / (1 + r)t

FV = future value of single cash inflow or outflow

r = discount rate per period (annual rate divided by the number of periods in one year)

t = total number of periods

17. Importance of TCO in Supply Management

Service Providers

Retail

Manufacturing

Supply Chains/Supply Networks

18. Service and Retail Providers Understanding what drives the cost of overhead expenditures is crucial to any service business

Revenue must cover the direct costs, material and labor, and overhead in order to generate a profit

TCO analysis of recurring material costs are often overlooked and can yield great savings

TCO analysis of the labor base can reap lower per person costs, greater benefits, and improved morale

TCO analysis of equipment purchases may help reduce the expenditures for maintenance and parts over the lives of the investments

19. Manufacturing Manufacturers are concerned with all of the same TCO issues as service and retail firms, with some added issues

Issues that are particularly important in cost analysis for manufacturers are:

Direct materials

Manufacturing overhead

Emphasis should be placed on the variance between �should cost� and actual cost.

This should not be confused with price variance

20. Activity Based Costing A major problem in TCO analysis of manufacturers is accurate allocation of manufacturing overhead

Many manufacturers have used activity-based costing to help improve cost allocation

Activity-based costing (ABC) is a technique for accumulating cost for a given cost object that represents the total and true economic resources required or consumed by the object

21. Supply Chain/Supply Networks TCO analysis may include the study of:

Manufacturability

Infrastructure

Outsource decision

Analysis of suppliers beyond tier one

Structure of foreign and domestic tariffs/duties/taxes

Costs of delivery Foreign regulations

Foreign political/economic stability

Foreign exchange risk

Language/communication requirements

Volatility of end-customer demand

Inventory carrying costs

Inventory risk

Quality costs

22. Concluding Remarks TCO is an analytical tool and a philosophy

Accurate estimation of total costs requires a cross-functional approach

Supply management is a critical member of such a cross-functional approach

TCO is also applicable in one�s private life enabling better decision-making