Download

1 / 19

200 likes | 379 Views

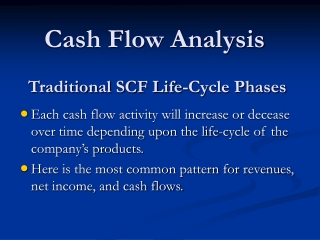

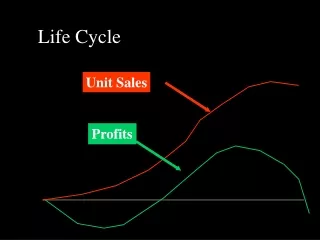

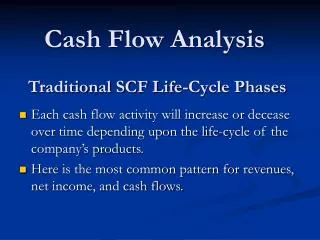

Traditional SCF Life-Cycle Phases. Cash Flow Analysis. Each cash flow activity will increase or decease over time depending upon the life-cycle of the company’s products. Here is the most common pattern for revenues, net income, and cash flows. Analyzing Cash Flow Information.

E N D

Traditional SCF Life-Cycle Phases Cash Flow Analysis • Each cash flow activity will increase or decease over time depending upon the life-cycle of the company’s products. • Here is the most common pattern for revenues, net income, and cash flows.

Analyzing Cash Flow Information Cash flow analysis can be used to address a variety of questions regarding a firm's cash flow dynamics: • How strong is the firm's internal cash flow generation? • Is the cash flow from operations positive or negative? • If it is negative, why? • Is it because the company is growing? • Is it because its operations are unprofitable? • Or is it having difficulty managing its working capital properly? • Does the company have the ability to meet its short-term financial obligations, such as interest payments, from its operating cash flow? • Can it continue to meet these obligations without reducing its operating flexibility?

Analyzing Cash Flow Information • How much cash did the company invest in growth? • Are these investments consistent with its business strategy? • Did the company use internal cash flow to finance growth, or did it rely on external financing? • Did the company pay dividends from internal free cash flow, or did it have to rely on external financing? • If the company had to fund its dividends from external sources, is the company's dividend policy sustainable? • What type of external financing does the company rely on? • Equity, short-term debt, or long-term debt? • Is the financing consistent with the company's overall business risk? • Does the company have excess cash flow after making capital investments? • Is it a long-term trend? • What plans does management have to deploy the free cash flow?

Recasting the SCF • Although it is possible to answer these questions using the GAAP SCF format, recasting the SCF makes answering these questions easier. • In addition, using a standard format makes comparison between companies easier. • Here is the model that we will use in this class.

Operating Cash Flow • Operating Cash Flow is broken up into two components, OCF before working capital investments and OCF before investments in long term assets. • Over the long run OCF must be positive, but firms in the early stages of development, growing rapidly, or investing heavily in research and development, marketing and advertising, and other future growth opportunities will have negative OCF.

Free Cash Flow • If cash flow after investing in long term assets is not positive then the firm did not generate enough cash from operations to pursue long-term growth opportunities and must rely on external financing. • These firms have less flexibility than firms that can generate the necessary funds internally. • Cash flow after long term investments is cash flow available to both debt and equity holders.

Free Cash Flow • Payments to debt holders include interest and principal payments. • Firms with negative free cash flow after investments in long term assets must borrow additional funds to meet their interest and principal payments. • They can also reduce their investments in working capital, long term investments, or issue additional equity.

Free Cash Flow • Cash flow after payments to creditors is free cash flow available to owners. • Payments to equity holders include dividends and stock repurchases. • If firms pay dividends despite negative cash flows available to equity holders then they are borrowing to pay dividends. This is not sustainable in the long term.

Summary • Examine cash flow from operations before investment in working capital to verify the company is able to generate a cash surplus from its operations. • Examine cash flow from operations before investment in long term assets to how the firms working capital is being managed and to see if the company can invest in long-term assets for future growth.

Summary • Examine free cash flow to debt and equity holders to asses a firm’s ability to meet its principal and interest payments. • Examine free cash flow to equity holders to asses a firm’s ability to sustain its dividend policy. • All cash flow analysis must be done taking into consideration the company’s business, its growth strategy, and its financial policies.

Analyzing Quality of Income • The Quality of Income Ratio is calculated as Cash Flow from Operations Net Income OR Cash Flow from Operations Net Income + Depreciation • This ratio should be > 1 for a healthy firm.

Analyzing Quality of Income • If there are significant differences between net income and operating cash flow ask the following questions: • What are the sources of the difference? • Is it due to accounting policy? • Is it due to one-time events or on-going activities? • Is the relationship changing over time? • If so, why? (see above for possible reasons). • Is it because of changes in business conditions or accounting policies and estimates?

Analyzing Quality of Income • What is the time lag between recognition of revenues and expenses and the receipt or payment of cash? • What uncertainties are there regarding cash collection or cash payments (e.g. bad debts, contingent liabilities, etc.) • Are the changes in working capital accounts normal? • If not, is there an adequate explanation for the changes?