Download

1 / 65

650 likes | 799 Views

Derivative Securities (Options): Puts & Calls. Lockheed Martin (LMT) Transactions. Lockheed Martin (LMT) Transactions. Lockheed Martin (LMT) Transactions. Lockheed Martin (LMT) Transactions. Rights Warrants Convertibles. Puts Calls. Types of Options. Common Stock Stock Indexes

E N D

Rights Warrants Convertibles Puts Calls Types of Options

Common Stock Stock Indexes Debt Instruments Foreign currencies Commodities Financial futures A Growing Market – puts and calls can be traded on:

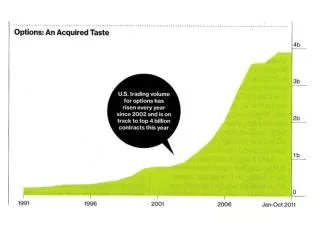

Why so much interest in options? • “…investors can buy a lot of priceaction with a limited amount of capital, while nearly always enjoying limited exposure to risk.”

Why Options? • A basic question asked by investors is: “Why buy stock options instead of shares in the underlying stock?” • To answer this question, we compare the possible outcomes from these two investment strategies: • Buy the underlying stock • Buy options on the underlying stock

Example: Buying the Underlying Stock versus Buying a Call Option • Suppose IBM is selling for $90 per share and call options with a strike price of $90 are $5 per share. • Investment for 100 shares: • IBM Shares: $9,000 • One listed call option contract: $500 • Suppose further that the option expires in three months. • Finally, let’s say that in three months, the price of IBM shares will either be: $100, $80, or $90.

Example: Buying the Underlying Stock versus Buying a Call Option, Cont. • Let’s calculate the dollar and percentage return given each of the prices for IBM stock:

Characteristics of Options • “Derivative” Securities - obtain their value from the underlying issue • Contract to buy or sell other securities

Characteristics of Options • Noownership interest in the underlying company (dividends; voting rights, etc.) • Provide leverage through a fixed purchase price - exaggerates any gain or loss

Option Exchanges • Chicago Board Options Exchange (CBOE) • Established in 1973 • cboe.org - professional traders • cboe.com - private investors

Option Exchange Features • Central marketplace vs. O-T-C • Secondary market • Option Clearing Corporation (OCC)

The Options Clearing Corporation • The Options Clearing Corporation (OCC) is a private agency that guarantees that the terms of an option contract will be fulfilled if the option is exercised. • The OCC issues and clears all option contracts trading on U.S. exchanges. • Note that the exchanges and the OCC are all subject to regulation by the Securities and Exchange Commission (SEC). Visit the OCC at: www.optionsclearing.com.

Option Exchange Features • Standardized Terms: • contract size • expiration dates • exercise (striking) price

Basic Option Terms(listed equity options) • Call Option: • contract to buy stock • 100 shares of stock • exercise price set by exchange • expires on fixed date – 3rd Friday of the expiration month

Basic Option Terms(listed equity options) • Put Option: • contract to sell stock • 100 shares of stock • exercise price set by exchange • expires on fixed date – 3rd Friday of the expiration month

Call - contract to: Buy 100 shares Fixed price Specified term Put - contract to: Sell 100 shares Fixed price Specified term Basic Option Terms

Option Jargon • “Striking Price” - price at which the contract is exercised or carried out • Example: • XYZ-AUG-30; “30” is the striking price, or exercise price of the option

Option Jargon • “Expiration Date” - maturity date; the third Friday of the expiration month • Example: • XYZ-AUG-30; option expires on the third Friday of August

Option Jargon • “Option Writer (Maker)” - seller of an option contract

Option Jargon • “Covered Writer” - already owns shares of the underlying stock; can deliver shares if exercised

Option Jargon • “Naked Writer” - does not own shares of the underlying stock; must buy shares if exercised

Option Jargon[Call Options] • “In the Money” - stock price greater than exercise price

Option Jargon[Call Options] • “Out of the Money” - stock price less than exercise price

Option Jargon[Call Options] • “At the Money” - stock price = exercise price

Option Pricing[Three Prices to Consider] • Underlying stock price per share • Exercise (striking) price of the option contract • Price (Premium) of the option contract

Call Option Pricing • Option premium reflects: • Intrinsic valueof the option, • plus the option’s time value • Premium = IV + TV • Time Value = Premium - IV

Call Option Pricing[ABC-MAY-80] • Intrinsic value (IV): • IV = Stock price - exercise price • IV = $81.75 - $80.00 = $1.75

Call Option Pricing[ABC-MAY-80] • Time value (TV): • TV = premium - intrinsic value • TV = $3.75 - $1.75 = $2.00

Put Option Pricing[ABC-JUL-80] • Intrinsic value (IV): • IV = Exercise price - stock price • IV = $80.00 - $79.00 = $1.00

Put Option Pricing[ABC-JUL-80] • Time value (TV): • TV = premium - intrinsic value • TV = $3.00 – 1.00 = $2.00

FIGURE 11.2 The Valuation Properties of Put and Call Options

Option Trading Strategies • Buying options for speculation • Hedging with puts and calls • Option writing and spreading

Buying Options for Speculation • Same motivation as buying stock • “Buy low, sell high” • Smaller investment - greater leverage • Limited loss

Hedging with Puts and Calls • Combination of two or more securities • Objectives: • To earn or protect a profit • Limit losses