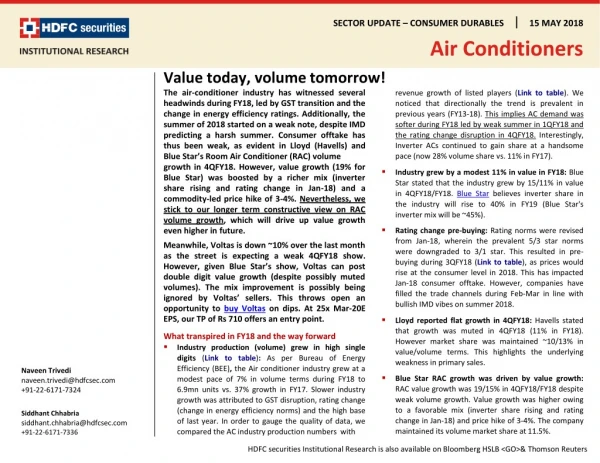

Download

1 / 11

120 likes | 243 Views

I. Household sector as an institutional sector in national accounts. Vu Quang Viet Consultant to UNSD. Definition of a household.

E N D

I. Household sector as an institutional sector in national accounts Vu Quang Viet Consultant to UNSD

Definition of a household • A household is defined as a group of persons who share the same living accommodation, who pool some, or all, of their income and wealth and who consume certain types of goods and services collectively, mainly housing and food. • Members of the same household do not necessarily have to belong to the same family so long as there is some sharing of resources and consumption. • Students who study away from home are still part of a household. • Excluded are: • Hired domestic staff who live on the same premises; • People who live permanently in institutions (religious orders, mental hospitals, prisons, retirement);

Household as producers of goods and services Households as wage earners Household as net income transfers receivers Household as consumer of goods and services Household sector in SNA Operating surplus Compensation of employees Property income Social benefits/cont Other current transfers

Actual final consumption vs. actual final consumption expenditure Final consumption expenditure consists of expenditure incurred by resident households on final goods and services. Actual final consumption consists of: Final expenditure of goods and services paid by households; Social transfers in kind received from the Government or NPISHs. Purchases of goods and services by gov. and NPISHs and distributed free to households ( including social security benefits reimbursed on specified goods and services, other social security benefits in kind except reimbursement; social assistance benefits in kind); Part of output of government that benefits directly individuals (=individual government final consumption). Social transfer in kind cannot be captured in Household consumption survey and has to estimated from government output and imputed by national accountants.

Final consumption expenditure in the use table Social transfers in kind Can be covered by household survey

Compensation of employees • Compensation of employees (D1) • Wages and salaries (D11) • Employers’ social contributions (D12) • Employers’ actual social contributions (D121) • Employers’ actual pension contributions (D1211) • Employers’ actual non-pension contributions(D1212) • Employers’ imputed social contributions (D122) • Employers’ imputed pension contributions (D1221) • Employers’ imputed non-pension contributions (D1222)

Employers’ social contributions • Employers’ social contributions are social contributions payable by employers to social security funds or other employment-related social insurance schemes to secure social benefits for their employees. • Social security schemes are operated by general government; • Other employer-related social insurance schemes may be operated by the employers themselves, by an insurance corporation or may be an autonomous pension scheme.

Employers’ imputed social contributions: definition • Some employers provide benefits themselves directly to their employees, former employees or dependants without involving an insurance enterprise or autonomous pension fund, and without creating a special fund or segregated reserve for the purpose. • Existing employees may be considered as being protected against various specified needs or circumstances, even though no reserves are built up to provide future entitlement.

Employers’ imputed social contributions: principle and practice • SNA Principle: Remuneration should be imputed for such employees equal in value to secure the de facto entitlements employees may obtain at present and in the future. • SNA Recommended Practice: Use the unfunded non-pension benefits payable by the enterprise during the same accounting period as an estimate of the imputed remuneration that would be needed to cover the imputed contributions. • More Practical Practice: Use the current unfunded pension and non-pension benefits payable unless employers are legally liable to their benefit policies, especially the government.