Income Tax Complexity: A Work In Progress

10 likes | 243 Views

Income Tax Complexity: A Work In Progress Trayton Oakes, Department of Economics & Department of Political Science, College of Arts and Sciences and Honors College Kari Battaglia, M.A., Department of Economics, College of Arts and Sciences. Topic. Abstract & Literature Review. Methodology.

Income Tax Complexity: A Work In Progress

E N D

Presentation Transcript

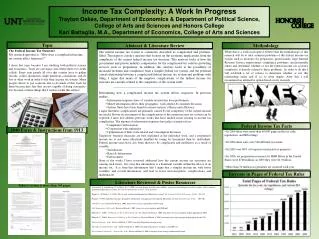

Income Tax Complexity: A Work In Progress Trayton Oakes, Department of Economics & Department of Political Science, College of Arts and Sciences and Honors College Kari Battaglia, M.A., Department of Economics, College of Arts and Sciences Topic Abstract & Literature Review Methodology The Federal Income Tax Structure My research question is, “How does a complicated income tax system affect taxpayers?” I chose this topic because I am studying both political science and economics. Taxes are one major area where these two fields collide. Every year people all over this country have to gather records, collect documents, make numerous calculations, and do lots of other work in order to file their income tax returns. Many people choose to pay someone else to do much of this work for them because they fear they are not capable of doing it properly. It is because of these things that I wish to tackle this subject. • The federal income tax system is commonly described as complicated and problem-filled. This paper is a policy analysis that focuses on the economic implications from the complexity of the current federal income tax structure. This analysis looks at how the government and private industry compensates for the complicated tax code by providing services such as preparation. In addition, this analysis looks at the possibility of increased revenues and compliance from a simpler federal tax system, and the potential causal relationship between a complicated federal income tax system and problems with filing. I argue that many of the negative complications of the federal income tax structure are causally related to the complexity of the system itself. • _____________________________________________________ • Determining how a complicated income tax system affects taxpayers. In previous studies: • Information taxpayers have of variable taxation has been problematic • Mixed information affects their geographic, work-related & consumer decisions • Serious flaws have been found in current systems’ efficacy and efficiency • I argue that these complications are primarily caused by the complexity of the current income tax model. Before an assessment of the complications of the current income tax system can be explored, I must first address previous works that have studied issues relating to income tax complexities. The amount of information taxpayers have plays a major role in: • Compliance with taxation • Cooperation with authorities • Optimization of their work-related and consumption decisions • Taxpayers’ business decisions are best explained at the individual level, and a progressive income tax is not more effectively handled by taxing by household than by individuals. Federal income taxes have also been shown to be complicated and ineffective as a result of variable: • Jurisdictions • Rates & Information • Enforcement • None of the works I have reviewed addressed how the current income tax structures are causing such issues. It is clear that information is a dominant variable within the effects of an income tax. It is from this information that I argue that a simpler income tax with fewer variables, and overall information, will lead to fewer misconceptions, complications, and inadequacies. While this is a work in progress I believe that the methodology of this research will be to take common problems of the federal income tax system such as necessity for preparatory professionals, large Internal Revenue Service employment, compliance problems, and potentially others and determine whether or not the federal income tax system’s complexity is directly related to these problems. In order to do this I will establish a set of criteria to determine whether or not this relationship exists and if so, to what degree. After this I will recommend an alternative option based on my research. Federal Income Tax Facts 1040 Form & Instructions from 1913 • In 2004 there were more than 60,000 pages in the tax code, regulations, and IRS rulings • In 2004 there were over 500 different tax forms. • In 2003 over 60% of taxpayers used paid tax preparers. • In 1996, tax preparation revenues for H&R Block in the United States were $700 million; in 2003 they were $1.9 billion. • More than 30 million tax penalties are assessed each year. Increase in Pages of Federal Tax Rules Literature Reviewed & Poster Resources Today’s version is more than 160 pages. Osmundsen, P., Schjelderup, G., & Hagen, K. P. (2000). Personal income taxation under mobility, exogenous and endogenous welfare weights, and asymmetric information [Electronic version]. Journal of Population Economics, 13(4), 623-637. Piggott, J., & Whalley, J. (1996). The tax unit and household production [Electronic version]. The Journal of Political Economy, 104(2), 398-418. Pischke, J. (1995). Individual income, incomplete information, and aggregate consumption [Electronic version]. Econometrica, 63(4), 805-840. 1040 Form. (n.d.). Retrieved March 8, 2009, from www.irs.ustreas.gov/pub/irs-utl/1913.pdf 1040 Instructions 2008. (n.d.). Retrieved March 8, 2009, from www.irs.gov/pub/irs-pdf/i1040.pdf Edwards, C. (2003). 10 Outrageous Facts About the Income Tax. Retrieved March 8, 2009, from http://www.cato.org/pub_display.php?pub_id=3063 Edwards, C. (2004). Democrats' Challenge on Tax Complexity. Retrieved March 8, 2009, from http://www.cato.org/pub_display.php?pub_id=2763 Charity Navigator. (n.d.). Retrieved March 8, 2009, from http://blog.charitynavigator.org/ Thoughts about Real Estate. (n.d.). Retrieved March 8, 2009, from http://mdrealestate.wordpress.com/2007/11/ Zen Consulting Group Inc. - Income Tax. (n.d.). Retrieved March 8, 2009, from http://www.zencgi.com/IncomeTax.html