Single Payment Ideas

Single Payment Ideas. A single payment really means an individual receives funds once and gives up funds once. There are two payments, but there is a closing of a loop in that money comes in and then goes out (or vice versa.) Between the two points in time interest is considered.

Single Payment Ideas

E N D

Presentation Transcript

Single Payment Ideas A single payment really means an individual receives funds once and gives up funds once. There are two payments, but there is a closing of a loop in that money comes in and then goes out (or vice versa.) Between the two points in time interest is considered.

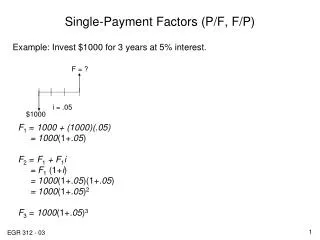

Single Payment Future Amount If you have $1 today and can earn an interest rate of 10% by the end of the first year then you will have $1.10. The$1.10 is calculated as the amount you start the period with plus the product of what you start the period with times the rate of interest that period – the 1.10 = 1 + 1(.1). If F is the amount at the end of the period, P is the amount at the beginning of the period and i is the rate of interest during the period, then in general we have F = P + Pi = P(1 + i).

Growth in general If you start out with P and wait one period at rate i we just saw you have F = P(1 + i). Now, if you again earn i, by the end of the second period you would have F = P(1 + i) + P(1 + i )i (start period with + start period with times i) = P(1 + i)(1 + i) = P(1 + i)2. In general, at the end of n periods, you have F = P(1 + i)n.

The formula F = P(1 + i)n, can be called the single payment future value (sometimes called the single payment compound amount) formula. Notice if we know or have specific numerical values for -the present amount P, -the constant interest rate each period i, and -the number of periods n, then we can solve for the future amount. Example: Say your grandmother gives you $10 and wants you to pay her back in 2 years and she will charge you 8% interest each year. How much do you pay her back at the end of two years? Let’s look at a time line on the next slide.

10 – you received $10 0 1 2 3 … n ? – How much do you pay back? F = 10(1 + .08)2 = 10(1.1664) = 11.66

The Future Value Factor We saw on the last page that the amount to be paid back was F = 10(1 + .08)2 = 10(1.1664) = 11.66. Remember in general we know F = P(1 + i)n. (1 + i)n is called the interest factor by which we multiple the present amount to get the future amount. The interest factor is part of the formula and includes the interest rate.

I want to show you how Microsoft Excel can be used to get single payment future value interest factors. On the next slide I have put into the first column time with values from 0 to 10. In the second column I have the future value interest factors for time 0 to time 10. If you clicked the mouse in cell B3 you see the value 1.1. But if you look up in the Excel spreadsheet area formula bar you see the formula =(1 + .1)^A2. I typed it in. The (1 + .1) looks familiar. The ^ is how you raise to a power in Excel. A2 refers to the cell A2. Where we see the value is 1. So (1 + .1)^A2 = 1.1 The reason I put A2 into the formula is because when I am done typing it I can drag the cell down to the 10th time period and the A2 will change to A3, A4 and so on as I drag down. This way, repetitive equations can be entered quickly.

Single Payment Present Value The present value concept uses the growth process we just studied, but the focal point is the present. As an example, what amount do you need today if you want $1.10 at the end of the period and you can earn 10% during the period. You need P = F / (1 + i) = 1.10 / (1 + .1) = $1.00 In general if you want to have F n periods from now and you can earn i each period , then today you need P = F / (1 + i)n. Note, the present value of an amount today would mean n = 0 and so P = F because anything raised to the power zero equals 1.

The single payment prevent value factor In the formula P = F / (1 + i)n the interest factor is 1 / (1 + i)n. We could use Excel to get the factor. In the third column of the Excel slide I had before I typed the equation =1/(1 + .1)^A3 in column C3. Then I was able to drag down the rest of the way. Let’s do an example. Say on your 21st birthday you want to have $100 so you can go out on the town and buy you and your friends some stuff, you know, pizza and soda and the like. The bank is currently paying 4% a year in interest each year. How much do you have to put into the bank on your 18th birthday so that you have the $100 on your 21st birthday?

100 0 1 2 3 … n 18 19 20 21 P = 100/(1 + .04)^3 = 100(.8890) = 88.90

Discount Rate or Internal Rate of Return The present value P of a future amount F n periods from now at interest rate i is P = F / (1 + i)n. The interest rate i in this context is often called the discount rate. It is the rate at which we “discount” future values to place them in terms of today’s value. Do not confuse this with the discount rate in the context of monetary policy. The Federal Reserve charges banks the “discount rate” when those banks borrow from the Fed.

Example Say you buy a stock for $50 and 3 years later the stock sells for $87.50. How much did you earn on the stock on an annual basis? Remember the general formula F = P(1 + i)n connects F, P, i, and n. If we fill in what we know we get 87.50 = 50(1 + i)3. So (1 + i)3 = 87.50/50, or 1+ i = (87.50/50)1/3, or i = (87.50/50)1/3 - 1 = 1.2051 – 1 = .2051 or 20.51% The internal rate of return on the stock over the 3 years was 20.51%.

The rule of 70 The rule of 70, sometimes called the handy rule of 70, is an approximation rule to answer the question of how long it will take a dollar amount to double. Remember the formula F = P(1 + i)n ? If F = 2 and P = 1 the formula becomes 2 = (1 + i)n. Taking the natural log of both sides gives, after some arrangement ln 2 = n ln (1 + i), Or n = ln 2/ln (1 + i). Now, using this formula will tell you exactly how long it will take some dollar amount to double. I bet you like this formula, right? A few people do not like it so an approximation was found that works fairly well when interest rates are around 5 to 12%.

The approx rule is Years to double (n) = 70/interest rate. Note, in the approximation rule 12%, for example, is 12, while in the exact formula on the previous slide we use 12% as .12. So, at 12% approx rule says a dollar amount will double in 70/12 = 5.83 periods. The exact formula would have n = ln 2 / ln(1 + .12) = 6.12 periods.

Summary Here we have seen the financial arrangements known by the umbrella phrase of single payment formulas. Whenever we compare dollars across time we incorporate interest.