Download

1 / 20

200 likes | 403 Views

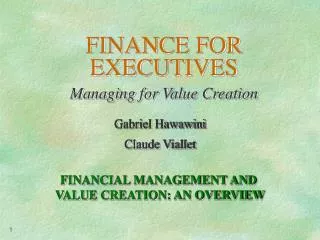

FINANCE FOR EXECUTIVES Managing for Value Creation. Gabriel Hawawini Claude Viallet. ASSESSING LIQUIDITY AND OPERATIONAL EFFICIENCY. EXHIBIT 3.1a: OS Distributors’ Balance Sheets. Figures in millions of dollars. DEC. 31, 1995. DEC. 31, 1996. DEC. 31, 1997. ASSETS. ·. $104.0. $119.0.

E N D

FINANCE FOR EXECUTIVES Managing for Value Creation Gabriel Hawawini Claude Viallet ASSESSING LIQUIDITY ANDOPERATIONAL EFFICIENCY

EXHIBIT 3.1a: OS Distributors’ Balance Sheets.Figures in millions of dollars DEC. 31, 1995 DEC. 31, 1996 DEC. 31, 1997 ASSETS · $104.0 $119.0 $137.0 CURRENT ASSETS Cash1 $6.0 $12.0 $8.0 Accounts receivable 44.0 48.0 56.0 Inventories 52.0 57.0 72.0 Prepaid expenses2 2.0 2.0 1.0 · 56.0 51.0 53.0 NONCURRENT ASSETS Financial assets & intangibles 0.0 0.0 0.0 Property, plant, & equip. (net) 56.0 51.0 53.0 Gross value3 $90.0 $90.0 $93.0 Accumulated depreciation (34.0) (39.0) (40.0) TOTAL ASSETS $160.0 $170.0 $190.0

EXHIBIT 3.1b: OS Distributors’ Balance Sheets.Figures in millions of dollars DEC. 31, 1995 DEC. 31, 1996 DEC. 31, 1997 LIABILITIES AND OWNERS’ EQUITY · $54.0 $66.0 $75.0 CURRENT LIABILITIES Short-term debt $15.0 $22.0 $23.0 Owed to banks $7.0 $14.0 $15.0 Current portion of long-term debt 8.0 8.0 8.0 Accounts payable 37.0 40.0 48.0 Accrued expenses4 2.0 4.0 4.0 · 42.0 34.0 38.0 NONCURRENT LIABILITIES Long -term debt5 42.0 34.0 38.0 · 64.0 70.0 77.0 Owners’ equity6 64.0 70.0 77.0 TOTAL LIABILITIES AND $160.0 $170.0 $190.0 OWNERS’ EQUITY

EXHIBIT 3.2a: The Managerial Balance Sheet Versus the Standard Balance Sheet. THE MANAGERIAL BALANCE SHEET INVESTED CAPITAL OR NET ASSETS CAPITAL EMPLOYED Short-term debt Long-term financing Long-term debt plus Owners’ equity Cash Working capital requirement (WCR) Operating assets less Operating liabilities Net fixed assets

EXHIBIT 3.2b: The Managerial Balance Sheet Versus the Standard Balance Sheet. THE STANDARD BALANCE SHEET LIABILITIES AND OWNER’S EQUITY TOTAL ASSETS Cash Short-term debt Operating assets Operating liabilities Accounts receivable plus Inventories plus Prepaid expenses Accounts payable plus Accrued expenses Long-term financing Long-term debt plus Owners’ equity Net fixed assets

EXHIBIT 3.3: The Firm’s Operating Cycle and Its Impact on the Firm’s Balance Sheet. D = Change in the balance sheet account

EXHIBIT 3.4: The Firm’s Operating Cycle, Showing Cash-to-Cash Period.

EXHIBIT 3.5: Extracts from Carrefour’s Balance Sheets and Income Statements. Figures in millions of dollars YEAR RECEIVABLES INVENTORIES PAYABLES WCR1 CASH2 SALES 1994 $68 $1,939 $5,296 –$3,289 $3,123 $27,260 1995 84 2,172 5,484 –3,228 3,281 28,922 Source: Company’s Annual Report. 1WCR = Working capital requirement = Receivables + Inventories – Payables 2Includes cash lent to other companies.

EXHIBIT 3.6: OS Distributor’s Managerial Balance Sheets. All data from the balance sheets in Exhibit 3.1; figures in millions of dollars DEC. 31, 1995 DEC. 31, 1996 DEC. 31, 1997 INVESTED CAPITAL OR NET ASSETS • Cash • Working capital requirement (WCR)1 • Net fixed assets $12.0 10% 63.0 50% 51.0 40% $126.0 100% $ 8.0 6% 77.0 56% 53.0 38% $138.0 100% $ 6.0 5% 59.0 49% 56.0 46% $121.0 100% TOTAL INVESTED CAPITAL OR NET ASSETS CAPITAL EMPLOYED • Short-term debt • Long-term financing Long-term debt Owners’ equity $ 15.0 12% 106.0 88% $42.0 64.0 $121.0 100% $ 22.0 17% 104.0 83% $34.0 70.0 $126.0 100% $ 23.0 17% 115.0 83% $38.0 77.0 $138.0 100% TOTAL CAPITAL EMPLOYED 1 WCR = (Accounts receivable + Inventories + Prepaid expenses) – (Accounts payable + Accrued expenses). These amounts are given in Exhibit 3.1.

EXHIBIT 3.7: The Behavior of Working Capital Requirement overTime for a Firm with Seasonal Sales. WCR is assumed to be set at 25 percent of sales

EXHIBIT 3.8a: OS Distributor’s Net Investment in Its Operating Cycle and Its Financing. All data from the balance sheets in Exhibit 3.1; figures in millions of dollars DECEMBER 31, 1995 NET INVESTMENT IN THE OPERATING CYCLE OR WORKING CAPITAL REQUIREMENTS (WCR) WCR = [Accounts receivable + Inventories + Prepaid expenses] [$44 + $52 + $2] – [$37 + $2] = $59 – [Accounts payable + Accrued expenses] THE FINANCING OF THE OPERATING CYCLE Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets $50 $42 + $64 – $56 = Net short-term financing (NSF) = Short-term debt – Cash $9 $15 – $6 = NLF/WCR = percentage of working capital requirement financed long term 84.7% $ 50/$59 = NSF/WCR = percen tage of working capital 15.3% $ 9/$59 = requirement financed short term 100.0% WORKING CAPITAL REQUIREMENT AND ITS FINANCING 15.3% 84.7% WCR NSF $9 $59 NLF $50

EXHIBIT 3.8b: OS Distributor’s Net Investment in Its Operating Cycle and Its Financing. All data from the balance sheets in Exhibit 3.1; figures in millions of dollars DECEMBER 31, 1996 NET INVESTMENT IN THE OPERATING CYCLE OR WORKING CAPITAL REQUIREMENTS (WCR) WCR = [Accounts receivable + Inventories + Prepaid expenses] [$48 + $57 + $2] – [$40 + $4] = $63 – [Accounts payable + Accrued expenses] THE FINANCING OF THE OPERATING CYCLE Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets $53 $34 + $70 – $51 = Net short-term financing (NSF) = Short-term debt – Cash $10 $22 – $12 = NLF/WCR = percentage of working capital requirement financed long term 84.1% $53/$63 = NSF/WCR = percen tage of working capital 15.9% $10/$63 = requirement financed short term 100.0% WORKING CAPITAL REQUIREMENT AND ITS FINANCING WCR NSF $10 $63 NLF $53 15.9% 84.1%

EXHIBIT 3.8c: OS Distributor’s Net Investment in Its Operating Cycle and Its Financing. All data from the balance sheets in Exhibit 3.1; figures in millions of dollars DECEMBER 31, 1997 NET INVESTMENT IN THE OPERATING CYCLE OR WORKING CAPITAL REQUIREMENTS (WCR) WCR = [Accounts receivable + Inventories + Prepaid expenses] [$56 + $72 + $1] – [$48 + $4] = $77 – [Accounts payable + Accrued expenses] THE FINANCING OF THE OPERATING CYCLE Net long-term financing (NLF) = Long-term debt + Owners’ equity – Net fixed assets $62 $38 + $77 – $53 = Net short-term financing (NSF) = Short-term debt – Cash $5 $23 – $8 = NLF/WCR = percentage of working capital requirement financed long term 80.5% $62/$77 = NSF/WCR = percen tage of working capital 19.5% $15/$77 = requirement financed short term 100.0% WORKING CAPITAL REQUIREMENT AND ITS FINANCING WCR NSF $15 $77 NLF $62 19.5% 80.5%

EXHIBIT 3.9a: Some Benchmark Ratios of Working Capital Requirement to Sales for a Sample of U.S. Sectors1. WORKING CAPITAL REQUIREMENT SECTOR AS PERCENTAGE OF SALES 1996 Highest 1992–96 Lowest 1992–96 Electronic components 24% 25% 22% Aircraft 22% 22% 19% Measurement instruments 21% 22% 21% Steel works 20% 20% 18% Motor vehicles 20% 20% 19% Machinery & equipment 19% 21% 18% Textiles 17% 20% 17% Chemicals 17% 17% 14% Wood products & buildings 16% 16% 14% Apparel products 15% 17% 15% Department stores 15% 19% 13% Plastic products 14% 15% 14% Computing equipment 14% 17% 14% Retail: Nongrocery stores 12% 15% 12% Paper 11% 12% 10% AVERAGE: ALL SCORES 10% 11% 10% 1 Source: Calculated by the authors using Compustat data.

EXHIBIT 3.9b: Some Benchmark Ratios of Working Capital Requirement to Sales for a Sample of U.S. Sectors1. WORKING CAPITAL REQUIREMENT SECTOR AS PERCENTAGE OF SALES 1996 Highest 1992–96 Lowest 1992–96 Drugs 10% 13% 10% Wholesale: Durables 10% 10% 7% Soaps & perfumes 8% 8% 7% Food 7% 7% 5% Wholesale: Nondurables 5% 6% 5% Telephone 3% 3% –2% Oil & natural gas 2% 3% 2% Publishing 2% 2% 1% Beverages 1% 1% 0% Electric services 0% 2% 0% Grocery stores 0% 1% 0% Natural gas: Distribution –1% 2% –1% Services2 –1% –1% –5% Air transportation3 –13% –11% –13% 2The services sector covers a variety of industries, including advertising, cleaning, data processing, research and development, and management consultancy. 3The air transportation sector covers scheduled and nonscheduled air transportation as well as air courier services and airports and terminal services.

EXHIBIT 3.10: OS Distributor’s Management of Its Operating Cycle. All data from the balance sheets in Exhibit 3.1 and the income statements in Exhibit 2.2; figures in millions of dollars DEC. 31, 1995 DEC. 31, 1997 OBJECTIVE To evaluate the overall efficiency with which the firm’s operating cycle is managed Working capital requirement (WCR)1 Sales Cost of goods sold (COGS) Inventories Accounts receivable Average daily sales2 Accounts payable Average daily purchases2,3 $77 $420 $59 $390 = 16% = 15% To evaluate the efficiency with which inventories are managed $400 $72 $328 $52 = 5.6 times = 6.3 times To evaluate the efficiency with which accounts receivable are managed $44 $390/365 $56 $480/365 = 41 days = 43 days To evaluate the efficiency with which accounts payable are managed $37 $332/365 $48 $415/365 = 41 days = 42 days 1 WCR is found in Exhibit 3.6. 2 We assume the year has 365 days. 3 Purchases are equal to COGS plus the change in inventories (see equation 3.11). In 1994, inventories were $48, thus purchases (1995) = $328 + ($52 – $48) = $332. Purchases (1996) = $353 + ($57 – $52) = $358; and purchases (1997) = $400 + ($72 – $57) = $415.

EXHIBIT 3.12: OS Distributor’s Net Working Capital (NWC) and Current and Quick Ratios. All data from the balance sheets in Exhibit 3.1; figures in millions of dollars DEC. 31, 1995 DEC. 31, 1996 DEC. 31, 1997 • NWC = [Current assets – Current liabilities]1 • NWC = [Long-term financing2 – Net fixed assets]3 • Current ratio = Current assets Current liabilities • Quick ratio = Cash + Accts receivable Current liabilities $119 – $66 = $53 $104 – $54 = $50 $137 – $75 = $62 ($42 – $64) – $56 = $50 ($38 + $77) – $53 = $62 ($34 + $70) – $51 = $53 $119 $66 $137 $75 $104 $54 = 1.80 = 1.83 = 1.93 $12 + $48 $66 $8 + $56 $75 $6 + $44 $54 = 0.91 = 0.85 = 0.93 1 This is the traditional definition of net working capital. 2 Long-term financing = Long-term debt + Owners’ equity. 3 According to this definition, net working capital is the same as net long-term financing (see equation 3.4).

EXHIBIT A3.1: Financing Investments Using a Matched Strategy.

EXHIBIT A3.2: Financing Investments Using a Conservative Strategy.

EXHIBIT A3.3: Financing Investments Using an Aggressive Strategy.