Download

1 / 38

390 likes | 576 Views

National Insurance. Presented by : Rachel Kuan 08B1902 Tiffany Chiam 08B1901 Michelle Chang 08B1928 Emily Wee 08B1709. DEFINITION. Those with earned income will contribute to the National Insurance fund from which benefits are paid.

E N D

National Insurance Presented by : Rachel Kuan 08B1902 Tiffany Chiam 08B1901 Michelle Chang 08B1928 Emily Wee 08B1709

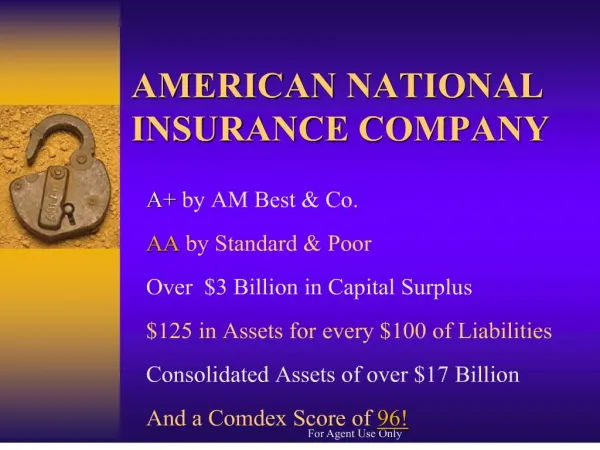

DEFINITION • Those with earned income will contribute to the National Insurance fund from which benefits are paid. • These benefits include retirement pensions, unemployment pay, widow’s benefit, invalidity benefit, and certain sickness and maternity benefits.

NATIONAL INSURANCE CONTRIBUTIONS EMPLOYED PERSON SELF-EMPLOYED PERSON PAID BY SELF-EMPLOYED PERSON PAID BY EMPLOYEE PAID BY EMPLOYER CLASS 4 CLASS 2 CLASS 1 PRIMARY CLASS 1A CLASS 1 SECONDARY CLASSES OF NATIONAL INSURANCE CONTRIBUTIONS

The amount of National Insurance Contribution(NIC) a person pays and the payment of contributions depend on the class of contribution.

Example Stephen works for Camberley Cars Ltd on a part-time basis earning a salary of ₤19,000 p.a. He is provided with a company car; petrol for both business and private mileage; and a place is provided for his daughter at the company’s workplace nursery while he is working for them. Stephen also runs a small bed and breakfast business from his home. In the year to 31 March 2010 his taxable trading profit from the business is ₤10,300. Explain which classes of NICs are payable by Stephen and Camberley Cars Ltd in respect of 2009/10. Answer : • Class 1 primary contributions based on his salary from Camberley Cars Ltd of ₤19,000 as his earnings are in excess of ₤5,715. • Flat rate Class 2 contributions in respect of his bed and breakfast business. • Class 4 contributions in respect of his bed and breakfast business based on his taxable trading profits as they are in excess of ₤5,715. Camberley Cars Ltd will pay : • Class 1 secondary contributions based on Stephen’s salary of ₤19,000 as his earnings are in excess of ₤5,715. • Class 1A contributions are based on the assessable employment benefit arising from the provision of a company car and private petrol to Stephen. Note : Class 1A contributions are not required in respect of the provision of a nursery place as it is an exempt benefit.

NICs payable in respect of employees The following NICs are payable in respect of employees: • Class 1 primary contributions • Class 1 secondary contributions • Class 1A contributions The definition of earnings for Class 1 NIC purposes ‘Earnings’ for the purpose of Class 1 NICs consists of any remuneration derived from the employment and paid in cash or assets which are readily convertible into cash. The calculation of Class 1 NICs is based on gross earnings with no allowable deductions.

Gross earnings includes : • Wages, salary, overtime pay, commission or bonus • Sick pay, including statutory sick pay • Tips and gratuities paid or allocated by employer • Payment of the cost of travel between home and work • Vouchers (exchangeable for cash or non-cash items, such as goods).

Gross earnings do not include : • Exempt employment benefits. • Most taxable non-cash benefitsexcept remuneration received in the form of financial instruments, readily convertible assets and non-cash vouchers • Tips received from customers • Mileage allowance received from the employer provided it does not exceed the HMRC approved allowance mileage rate of 40p per mile • Business expenses paid for or reimbursed by the employer, including reasonable travel and subsistence expenses. Note : Dividends are not subject to NICs, even if they are drawn by a director/shareholder in place of monthly salary.

example Janet and John are employed by Garden Gnomes Ltd. Their remuneration for 2009/10 is as follows : Calculate Janet and John’s ‘gross earnings’ for Class 1 NIC purposes.

Answer to example • Notes • The employer’s pension contributions are excluded as they are an exempt benefit. • The employee’s pension contributions are ignored as these are not deductible in calculating earnings for NIC purposes. • The car benefit is excluded as it is non-cash benefit which will be assessed to Class 1A NICs, not Class 1.

Eligible employees Class 1 contributions are payable where the individual: • Is employed in the UK, and • Is aged 16 or over, and • Has earnings in excess of the lower earnings threshold of ₤5,715 for 2009/10.

Class 1 primary contributions Class 1 primary contributions are payable by employees: • Aged 16 or over until • Attaining pensionable age (65 for a man, 60 for a woman.) The employer is responsible for calculating the amount of Class 1 primary NICs due and deducting the contributions from the employee’s wages. Note that Class 1 primary contributions: • Are not an allowable deduction for the purposes of calculating the individual employees personal income tax liability. • Do no represent a cost to the business of the employer, as they are ultimately paid by the employee. Therefore, they are not a deductible expense when calculating the employer’s taxable trading profits.

Calculating class 1 primary contributions Primary contributions are normally calculated by reference to an employee’s earnings period: • If paid weekly, the contributions are calculated on a weekly basis (The apportioned lower limit is ₤110 per week (₤5,715/52) and the upper limit is ₤844 a week (₤43,875/52) • If paid monthly, the contributions are calculated on a monthly basis (The apportioned lower limit is ₤476 per month(₤5,715/12) and the upper limit is ₤3,656 a month (₤43,875/12) The primary contributions payable are calculated as: • 11% on gross earnings between ₤5,715 and ₤43,875 • 1% on gross earnings in excess of ₤43,875

Class 1 secondary contribution It is payable by employers in respect of employees: Age 16 or over Until the employee ceases employment There is no upper age limit for employer contributions, the employer is liable in full even if the employee is above pensionable age. Secondary contributions are an additional cost of employment and are a deductible expenses when calculating the employer’s taxable trading profits.

Calculating class 1 secondary contributions • Calculated by reference to an employee’s earnings period. (calculations should be performed on an annual basis unless you are clearly told otherwise) • 12.8% of all gross earnings above £5,715. • Notes to be taken account: • No upper earnings limit • No change in rate of NIC payable for employer contributions.

Example: Millie is employed by Blue Forge Ltd and is paid an annual salary of £43,000. Millie is also provided with the following taxable benefits: £ Company car 5,000 Vouchers for the local gym 2,000 Calculate the employee’s and the employer’s Class 1 NIC liability due for 2009/10.

Answer: • Class 1 NICs are due on annual earning of £45,000 (salary £43,000+voucher £2,000) • The company car is a non cash benefit and is not subject to Class 1 NICs. • Employee’s Class 1 NICs £ (£43,875- £5,715)@11% 4,198 (£45,000-43,875)@1% 11 4,209 • Employer’s Class 1 NICs (£45,000- £5,715)x 12.8% 5,028

Company directors • Special rules apply to company directors to prevent the avoidance of NICs by paying low weekly or monthly salaries, and then taking a large bonus in a single week or month. • Therefore, when an employee is a company director, his Class 1 NICs are calculated as if he had an annual earnings period.

Payment of class 1 contributions Administration and payment of Class 1 NICs is carried out by the employers as follows: • The employer is responsible for calculating the amount of Class 1 primary and secondary contributions at each pay date. • Primary contributions are deducted from employee’s wages by the employer and paid to HMRC on the employee’s behalf. • The total primary and secondary contributions are payable to the employer by the HMRC, along with income tax deducted from the employees under PAYE. • The payment is normally due on the 19th of each month (i.e. due not later than 14 days after the end of each PAYE month).

Class 1a NICs • Employers are required to Class 1A contributions on ‘taxable benefits’ provided to employees earning at a rate of £8,500 pa and directors. • No Class 1A contributions are payable in respect of: • Exempt benefits • Benefits already treated as earnings and assessed to Class 1 NICs, such as remuneration received in the form of non cash vouchers. The contributions are calculated as : • 12.8% on the value of the taxable benefits. Class 1A contributions are an additional cost of employment and are a deductible expense when calculating the employer’s taxable trading profits.

Example: Simon is employed by Dutton Ltd at an annual salary of £52,000. He was provided with a company car throughout 2009/10 that had a list of price of £15,000. The car has CO² emissions of 193 g/km. Petrol for both business and private mileage is provided by his employer. Calculate the employee’s and the employer’s Class 1 and Class 1A NIC liabilities due for 2009/10.

Answers: • Class 1 NICs Employee’s Class 1 NICs £ (£43,875- £5,715) x 11% 4,198 (£52,000- £43,875) x 1% 81 4,279 Employer’s Class 1 NICs (£52,000- £5,715) x 12.8% 5,924

Example… Continue… • Class 1A NICs Simon’s taxable benefits for Class 1A are as follows: Company motor car £ 15% + [(190-135)/5]= 26% x £15,000 3,900 Private fuel provided by company (26% x £16,900) 4,394 Taxable benefits for Class 1A 8,294 Employer’s Class 1A NICs (£8,294@12.8%) 1,062

NICs payable in respect of self-employed individuals NICs which are payable by self-employed individuals. • Class 2 contributions • Class 4 contributions

Class 2 contributions Payable by individuals: • Aged 16 or over until • Attaining pensionable age (65 man, 60 woman) Amount payable: • Class 2 contribution are a flat rate payment of £2.40 per week. • Maximum total Class 2 NICs payable for 2009/10 is therefore £125 (£2.40 x 52 weeks). Note that Class 2 Contributions: • Not an allowable deduction for the purposes of calculating the individual’s income tax liability. • Not a deductible expense when calculating the business’ taxable trading profits. Class 2 Contribution are collected by HMRC on a monthly basis by direct debit or by quarterly billing in arrears.

Class 4 contributions In addition to Class 2 NICs, a self-employed individual may also be liable to Class 4 NICs. Class 4 contributions are payable by self-employed individuals who: • At the start of the tax year, are aged 16 or over. They continue to pay until: • The end of the tax year in which they attain pensionable age (65 for a man, 60 for a woman). Note that Class 4 contributions: • Are not an allowable deduction for the purposes of calculating the individual’s income tax liability. • Are not a deductible expense when calculating the business’ taxable trading profits.

The definition of class 4 profits ‘Profits’ for the purposes of Class 4 NICs consists of: • The taxable trading profits of the individual that are assessed for income tax after deducting trading losses (if any) Note that ‘profits’ for Class 4 NICs are before deducting the individual’s personal allowance that is available for income tax purposes. If the individual has more than one business, the aggregate of all profits from all self-employed occupations are used to calculate the Class 4 NIC liability. Calculating Class 4 NICs The contributions payable are calculated as: • 8% on profits between ₤5,715 and ₤43,875 • 1% on profits in excess of ₤43,875

example James has been trading as a self-employed painter and decorator since 1998. His taxable trading profits for 2009/10 are ₤56,000 and he has trading losses brought forward of ₤10,000. His wife, Poppy, is a part-time mobile hairdresser. Her taxable trading profits for 2009/10 are ₤6,560. Calculate the Class 4 NICs payable by James and Poppy for 2009/10.

Payment of Class 4 contributions Class 4 contributions are paid to HMRC at the same time as the individual’s income tax due under self assessment, as follows:

Total NICs payable by a self-employed individual A self-employed individual pays both Class 2 and Class 4 NICs in respect of his trading profits. In addition, if the self-employed individual employs staff, he will be required to account for: • Class 2 and Class 4 NICs in respect of his trading profits. • Class 1 primary, Class 1 secondary and Class 1A NICs in respect of earnings and benefits provided to employees.

Example Diane has been a self-employed computer consultant for many years. Her taxable trading profits for 2009/10 are £50,000. Diane employs a full time personal assistant at a salary of £15,800 p.a. She also provides the assistant diesel-engine company car, which has a list price of £13,500 and CO² emission of 161g/km. Diane pays for the assistant’s private and business fuel. Calculate the total NICs that Diane must account for to HMRC in respect of 2009/10.

Answer: 1. Flat rate class 2 contribution in respect of the business. Class 2 NICs (£2.40 x 52 weeks) £ 125 2. Class 4 contributions in respect of the business based on taxable trading profits as they are in excess of £5,715. Class 4 NICs £ (£43,875- £5,715) x 8% 3,053 (£50,000- £43,875) x 1% 61 3,114 3. Class 1 secondary contributions as Diane is an employer, based on her personal assistant’s salary of £15,800. Employer’s Class 1 NICs (£15,800- £5,715) x 12.8% £1,291

Example… Continue… 4. Class 1A Contributions based on the benefit arising from the provision of a company car to the personal assistant. Company motor car £ 18% + [(160-135)/5] = 23% x £13,500 3,105 Private fuel provided (23% x £16,900) 3,887 Taxable benefits for Class 1A 6,992 Employer’s Class 1A NICs (£6,992 @ 12.8%) 895 5. Class 1 Primary contributions are levied on the personal assistant. However, it is Diane’s responsibility to deduct the NICs from the assistant’s salary and pay them to HMRC along with the Class 1 secondary contribution on the 19th of each month. Employees’s Class 1 NICs (£15,800- £5,715) x 11% 1,109

Example… Continue… Summary: £ Class 2 125 Class 4 3,114 Class 1 secondary 1,291 Class 1A 895 Diane’s total liability 5,425 Class 1 primary 1,109 Total amount Diane must account for to HMRC 6,534

~ The End ~ Thank You =)