Download

1 / 24

240 likes | 264 Views

This preview of the classical model explores the history of economic ideas, from pre-classical thoughts to classical political economy and neoclassical economics. It discusses the assumptions and principles of the classical model and how it determines real variables at full employment.

E N D

3 THE CLASSICAL MODEL Mankiw’s Text CHAPTER

History of Economic Ideas (briefly) • Pre-classical Economic Ideas: • Scholastic thought (Thomas Aquinas) • Mercantilism (1500 -1750) • Physiocracy (1750-1780) • Classical Political Economy: • Adam Smith, David Ricardo, J.S. Mill, Karl Marx… • Neoclassical Economics: • W.S. Jevons, Carl Menger, and Leon Walras • Alfred Marshall

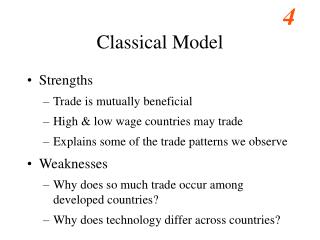

The Classical Model: A Preview • The classical model is a model of the economy that determines the real variables—real GDP, employment and unemployment, the real wage rate, consumption, saving, investment, and the real interest rate—at full employment. • The classical dichotomy, states: • At full employment, the forces that determine real variables are independent of those that determine nominal variables. • Most economists believe that the economy is rarely at full employment but that the classical model provides a benchmark against which to measure the actual state of the economy.

The Classical Model: A Preview • This model assumes that the economy automatically ensures that supply equals demand for every commodity. The economy is at full-employment. • Say’s Law: Supply creates its own demand. • Supply and demand are made equal by fast-acting prices that quickly close the gap between supply and demand whenever there is one. Prices are flexible in all markets. • Market-Clearing Model: Prices freely adjust to equilibrate supply and demand.

Outline of the classical model • A closed economy, market-clearing model • Aggregate Supply side • factor markets (supply, demand, price) • determination of output/income • Aggregate Demand side • determinants of C, I, and G • Equilibrium • goods market • loanable funds market

The Labor Market and Potential GDP • To understand how potential GDP is determined, we study: • The demand for labor • The supply of labor • Labor market equilibrium • Potential GDP

MPL 1 As more labor is added, MPL MPL 1 Slope of the production function equals MPL 1 MPL and the production function Y output MPL L labor

Units of output Real wage MPL, Labor demand Units of labor, L Quantity of labor demanded MPL and the demand for labor Each firm hires labor up to the point where MPL = W/P.

Labor supply Units of output equilibrium real wage MPL, Labor demand Units of labor, L The equilibrium real wage The real wage adjusts to equate labor demand with supply.

Units of output Supply of capital equilibrium R/P MPK, demand for capital Units of capital, K The equilibrium real rental rate The real rental rate adjusts to equate demand for capital with supply.

The Neoclassical Theory of Distribution • Our theory of the distribution of total income between labor and capital is called the neoclassical theory of distribution. • It states that each factor input is paid its marginal product. • The total real income of labor is MPL x L = W/P× L • The total real income of capital is MPK x K = R/P× K

nationalincome capitalincome laborincome How income is distributed: • total labor income = total capital income = If production function has constant returns to scale, then

Measuring Economic Inequality • The census bureau defines a household’s income as money income, which equals market income plus cash payments to households by the government. • Market income equals wages, interest, rent, and profit earned by the household in factor markets, before paying income taxes.

Measuring Economic Inequality • The mode income is the most common income and was about $12,500 in 2000. • The median income is the level of income that separates the population into two groups of equal size and was $42,148. • The mean income is the average income and was $57,054.

Measuring Economic Inequality • The poorest 20% of the population in 2001 received only 3.5% of the total income. • The middle 20% of the received 14.5% of total income. • The richest 20% received 50.1% of total income.

Who Are the Rich and the Poor? The median income in 2005 was $46,326. Education is the single biggest factor affecting household income distribution.

Who Are the Rich and the Poor? Size of household, marital status, and age of householder arealso important. Race and region are the least important.

Distribution of Nation’s Wealth U.S. households in the top 20 percent of the income distribution earn own well more than 80 percent of the nation's wealth

The Dynamic Classical Model • Changes in Productivity • Labor productivity is real GDP per hour of labor. • Three factors influence labor productivity. • Physical capital • Human capital • Technology

The Dynamic Classical Model • Human capital is the knowledge and skill that has been acquired from education and on-the-job training. • Learning-by-doing is the activity of on-the-job education that can greatly increase labor productivity.

The Dynamic Classical Model • The percentage increase in labor hours exceeded the percentage increase in the population because the increase in capital and technological advances increased labor productivity, which increased the real wage rate, which in turn increased the labor force participation rate.