Download

1 / 32

320 likes | 459 Views

Finnair Group Interim Report 1 January – 31 March 2006. Industry bracing for tightening competition. Competition remained tough, especially in Nordic countries All airlines have strict efficiency programmes US airlines are shifting capacity to international traffic

E N D

Industry bracing for tightening competition • Competition remained tough, especially in Nordic countries • All airlines have strict efficiency programmes • US airlines are shifting capacity to international traffic • Record high volume of orders for new aircraft • Many airlines still in shaky financial shape

Finnair’s fuel bill grew 30 MEUR in first quarter • Fuel price remained high • Average price of tickets still at last year’s level • Good development in demand and turnover • Asian demand engine for growth • Introduction of new aircraft will temporarily weaken productivity during first part of year

Slow quarter as predicted Q1/2006 Q1/2005 Change % Turnover mill. € 480.3 443.4 8.3 EBITDAR 40.9 59.7 -31.5 EBIT excl. capital gains and fair values changes of derivatives -5.1 14.0 - Capital gains 0.0 0.0 ‘- Fair value changes of derivatives -0.1 4.7 - Operating profit/loss (EBIT) -5.2 18.7 - Profit after financial items -5.2 17.4 -

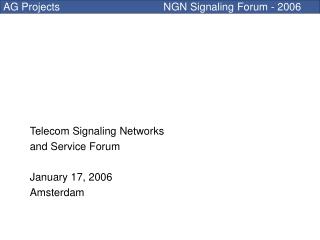

Group continues to have strong liquidityCash flow January-March

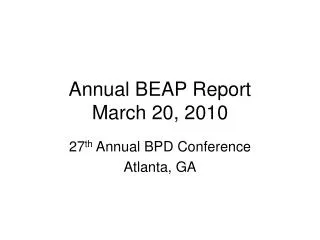

Unit costs +10.2%,without fuel +3.0%Change YoY 2002 2005 2006 2003 2004 %

Expensive fuel raises unit costs * excluding fair value changes of derivatives ATK = Available Tonne Kilometre

Asian success story continues • Demand grew by 21.8%, passenger numbers by 26.5% and load factors by 1.5% • Amount of cargo grew by 20.4% • New route to Nagoya (Japan) in June and Delhi (India) in November. Next year Kuala Lumpur (Malesia) which is 11th Asian destination. • 1-2 new Asian destinations per year, more frequencies to existing destinations • New Asian feeder routes to Edinburgh, Pisa, Kiev, Krakow, and Geneva, more flights to St Petersburg and Warsaw • Lie-flat bed seats installed in long-haul business class

Share of Asian traffic growing Scheduled traffic passenger and cargo revenues Q1/2006

Modern fleet • Finnair Scheduled Traffic will have one of most modern fleets in Europe by summer • Very popular new Embraer 170/190 aircraft increase flexibility, decrease costs and are eco-efficient • Remaining Boeing MD-80 aircraft retired at quickened pace, last flight on 3 July • Eighth wide-body aircraft, Finnair’s first Airbus 340 takes flight in July • New Airbus A340/350 aircraft replace current wide-body fleet by 2012

Fuel costs increasing • 2003: 10.2% of turnover • 2004: 12.5% of turnover • 2005: 15.6% of turnover • 2006: >20.0% of turnover at current price level and planned traffic growth • Finnair has hedged 55% of its fuel purchases for the next six months, thereafter for the following 18 months with a decreasing level.

120 million euro challenges • Fuel prices remain high • Fuel bill grew by 100 million euros last year, 120 million euros this year • Ticket prices still at low level • Focus on improving competitiveness without sacrificing service level • Internal services to work according to market rules • Streamline hierarchy, improve flexibility

Personnel cuts of 670… • New allocation of jobs • Statutory employer-employee negotiations beginning to cut 670 jobs in 2006-2007 • Planned efficiency measures to bring 80 MEUR annual cost benefits • Efficiency measures everywhere in organisation • Emphasis on Finnair Technical Services and support functions

…and increases of over 1000 • Strong growth in traffic between Asia and Europe has already ensured 3000 jobs • This year 350 persons will be recruited to flight operations • If competitive cost level is met, at best over 1000 will be recruited during next 5 years to operational functions

Strategic cornerstones • Growth from traffic between Europe and Asia as well as from near-by areas • Most desired airline by customers • Increased flexibility • Cost efficiency vs. competitors SUSTAINABLE, PROFITABLE GROWTH

Assesments for future development • Focus on traffic expansion between Asia and Europe will continue with additional aircraft • Load factors will improve with more flexible capacity • Strong booking situation • Continuing improvement of profitability • Fuel expenses will continue to be high • Price development continues poor due to tight competition • 2006 result clearly profitable

Slow fourth quarter as predictedChange in EBIT per quarter(Excluding capital gains and fair value changes of derivatives) MEUR 2002 2003 2004 2005 2006

Average yield and costs EUR c/RTK & EUR c/ATK 2005 2006 2002 2004 2003

Aircraft operating lease liabilities have grown in line with strategyFlexibility, costs, risk management On 31 March all leases were operating leases. If capitalised using the common method of multiplying annual aircraft lease payments by seven, the adjusted gearing on 31 March 2006 would have been 85,0%

Superiority of product • Direct to 50 international destinations • No time-consuming transfers at crowded airports • Best schedules • Morning-evening concept • Most punctual in Europe with least cancellations • Top class service in Europe • oneworld – alliance with best quality and coverage • New aircraft in European traffic

Operations systematically rationalised Personnel on average

Finnair Financial Targets”Sustainable value creation” EBIT margin at least 6% => 110-120 mill. € in the coming few years Operating profit (EBIT) EBITDAR margin at least 17% => over 300 mill. € in the coming few years EBITDAR Economic profit To create positive value over pretax WACC of 8.5% Adjusted Gearing Gearing adjusted for aircraft lease liabilities not to exceed 140 % Pay out ratio Minimum one third of the EPS Total Shareholder Return (TSR) On average 15% annual TSR => to double the value for shareholders in five years

www.finnair.com Finnair Group Investor Relations email: investor.relations@finnair.com tel: +358-9-818 4951 fax: +358-9-818 4092

![REVISED UH ADMINISTRATIVE PROCEDURES FOR PROCUREMENT (APM 8.200-8.295 [INTERIM])](https://cdn2.slideserve.com/5049032/revised-uh-administrative-procedures-for-procurement-apm-8-200-8-295-interim-dt.jpg)