Determinants

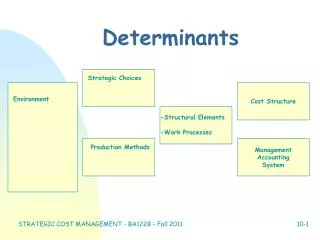

Determinants. Strategic Choices. Cost Structure. Environment. -Structural Elements -Work Processes. Management Accounting System. Production Methods. Types of Production Methods. Craft Mass Production Lean Production (Flexible Mfg. System). Structure Differences. Mass

Determinants

E N D

Presentation Transcript

Determinants Strategic Choices Cost Structure Environment -Structural Elements -Work Processes Management Accounting System Production Methods STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Types of Production Methods • Craft • Mass Production • Lean Production (Flexible Mfg. System) STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Structure Differences • Mass • Inflexible single purpose • High set-up time • Low labor skill level • Lean • Multi-use equipment • Low set-up time • Skilled labor force STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Work Process Differences • Mass • Supervisory control • Precise control over supplier • Standardized products • Independent, sequential prod. develop. • Lean • Empowered workers • Cooperative relationship w/suppliers • Customer focused organization • Concurrent, integrated design STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Cost Structure • Mass • Driven by volume • Allocation of fixed costs • Lean • Driven by process or activity STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Mgt. Actg. System in Lean Production • Driver focused • Value chain focused • Limited need for inventory reporting • Indirect cost orientation • Information system is critical for success STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Lean Prod--Attributes • Technical • Better decision relevance • Driver focused • External orientation • Cross functional & value chain focus • Better process understanding STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

MALP--Attributes, cont. • Behavioral • Team responsibility • Multiple motivation • Accountant as team player • Quality commitment • Global optimization • Risk of burnout STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

MALP--Attributes, cont. • Cultural • Team responsibility • Cooperation vs. competition • Focus on overall common good • Change in locus of power STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

MALP • Strategic Implications of Mgt. Actg. Systems • Quality choices can be affected • Cost is fundamental • Provides information on timeliness of production STRATEGIC COST MANAGEMENT- BA122B – Fall 2011

Accounting System Implications • Standard cost system does not work • Consider accumulating costs by value streams or activity groups • Expect to spend more money up front during the transition to lean operations • Use what information you already have STRATEGIC COST MANAGEMENT- BA122B – Fall 2011