Download

1 / 25

250 likes | 272 Views

Learn the definition of debit and credit, understand the rules of debits and credits, and practice analyzing and recording business transactions.

E N D

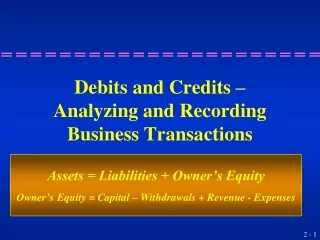

Debits and Credits –Analyzing and RecordingBusiness Transactions Assets = Liabilities + Owner’s Equity Owner’sEquity = Capital – Withdrawals + Revenue - Expenses

Debits and Credits What is the definition of debit? • The left side of any T account. • A number entered on the left side of any account is said to be debited to an account. What is the definition of credit? • The right side of any T account. • A number entered on the right side of any account is said to be credited to an account.

Debits and Credits Account Name (Title) Left side/Dr. (debit) Account Name (Title) Right side/Cr. (credit)

Rules of Debit & Credit A normal balance of an account is the increase side.* *Dr. (Debit) Increase side Normal Balance assets expenses withdrawals Account Categories

Rules of Debit & Credit A normal balance of an account is the increase side.* *Cr. (Credit) Increase side Normal Balance liabilities capital revenue Account Categories

Owner invests $50,000 cash in the business Debit Cash and credit Capital which increases one asset account and increases the capital account Cash 50,000 Capital 50,000

Deposited $3,600 received for the current day’s delivery services. Debit Cash and credit Delivery Fees which increases both an asset account and a temporary revenue account. Cash 3,600 Delivery Fees 3,600

Purchased $1,500 of Office Equpiment on credit Debit Office Equipment and Credit Accounts Payable which increases an asset account and increases a liability account. Office Eqpt 1,500 Accounts Payable 1,500

Delivery services are performed and $1,100 cash is received. Debit Cash and credit Delivery Fees which increases both an asset account and a temporary revenue account. Cash 1,100 Delivery Fees 1,100

Bought office supplies for $750 for the office with a check. Debit Office Supplies and Credit Cash which increases one assets account and decreases another asset account. Office Supplies 750 Cash 750

Billed a customer $575 for delivery services for $575 performed on account. Debit Accounts Receivable and credit Delivery Fees which increases both an asset account and a temporary revenue account. Accts Rec 575 Delivery Fees 575

Performed delivery services for a customer and received $400 cash. Debit Cash and credit Delivery Fees which increases both an asset account and a temporary revenue account. Cash 400 Delivery Fees 400

Received a $155 telephone bill and wrote a check to pay it. Debit Telephone Expense and credit Cash which increases one temporary expense account and decreases an asset account. Telephone Exp 155 Cash 155

Received $125 from a customer for delivery services performed last month on account. Debit Cash and credit Accounts Receivable which increases one asset account and decreases another asset account. Cash 125 Accts Rec 125

Wrote a check to pay the $900 monthly rent Debit Rent Expense and credit Cash which increases one temporary expense account and decreases an asset account. Rent Exp 900 Cash 900

Paid an additional $500 for the office equipment previously purchased on credit. Debit Accounts Payable and Credit Cash which decreases a liability account and decreases an asset account. Accts Payable 500 Cash 500

Owner invests $3,000 of his personal computer equipment into the business. Debit Computer Equpment and credit Capital which increases an asset account and increases the capital account. Computer Eqpt 3,000 Capital 3,000

Received $1,800 from a customer on account. Debit Cash and credit Accounts Receivable which increases one asset account and decreases another asset account. Cash 1,800 Accts Rec 1,800

The owner withdrew $75 of office supplies from the business for personal use. Debit Withdrawals and credit Office Supplies which increases one temporary capital account and decreases an asset account. Withdrawals 75 Office Supplies 75

Adverting expenses are incurred for $800 to be paid later. Debit Advertising Expense and credit Accounts Payable which increases one temporary expense account and increases a liability account. Advertising Exp 800 Accts Payable 800

Delivery services are performed on account in the amount of $2,500 Debit Accounts Receivable and credit Delivery Fees which increases both an asset account and a temporary revenue account. Accts Rec 2,500 Delivery Fees 2,500

The owner withdrew $500 for personal use. Debit Withdrawals and credit Cash which increases one temporary capital account and decreases an asset account. Withdrawals 500 Cash 500

Purchased a delivery truck for $16,000 on account Debit Delivery Equipment and Credit Accounts Payable which increases an asset account and increases a liability account. Delivery Eqpt 16,000 Accounts Payable 16,000

Paid $200 on account for the office equpiment previously purchased on account. Debit Accounts Payable and Credit Cash which decreases a liability account and decreases an asset account. Accts Payable 200 Cash 200

Solve for the missing part of the equation – Review Problem 5-8 Assets = Liabilities + Owner’s Equity Owner’sEquity = Capital – Withdrawals + Revenue - Expenses