Download

1 / 26

530 likes | 1.09k Views

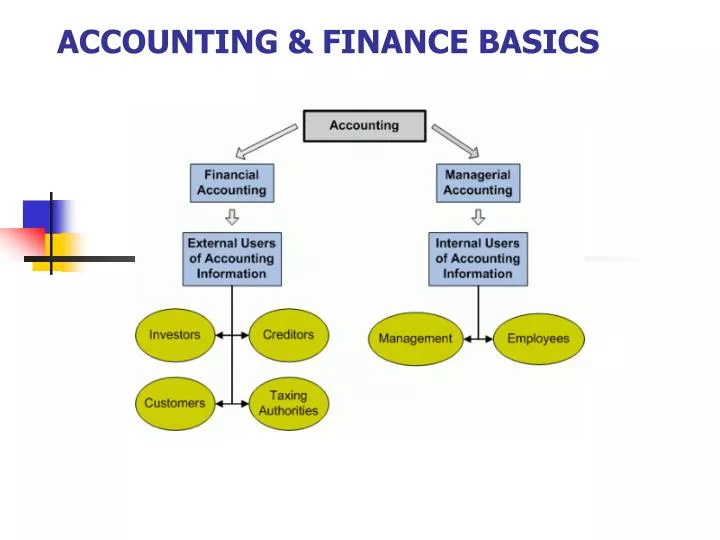

ACCOUNTING & FINANCE BASICS. WHO USES ACCOUNTING?. External users are parties outside the reporting entity (company) who are interested in the accounting information.

E N D

WHO USES ACCOUNTING? • External users are parties outside the reporting entity (company) who are interested in the accounting information. • Investors (owners) use accounting information to make buy, sell or keep decisions related to shares, bonds, etc. Creditors (suppliers, banks) utilize accounting information to make lending decisions. Taxing authorities (Internal Revenue Service) need accounting information to determine a company's tax liabilities. Customers may need accounting information to decide which products and from which company to buy. • Internal users are parties inside the reporting entity (company) who are interested in the accounting information. • A company's senior and middle management uses accounting information to run business. Employees utilize accounting information to determine a company's profitability and profit sharing. • Financial accounting provides information that is designed to satisfy the needs of external users. Such reporting is usually done in the form of financial statements. • Managerial accounting provides information that is useful in running a company by internal users. Such reporting is usually accomplished through custom designed reports.

FINANCIAL REPORTING • Businesses communicate accounting information to the public through a process known as financial reporting. • Financial reporting is a process through which companies communicate information to the public. • The central means of external financial reporting is a set of financial statements. The four general-purpose financial statements are the following: • Income Statement • Statement of Changes in Equity • Balance Sheet • Statement of Cash Flows

FINANCIAL STATEMENTS • An income statement presents revenues and expenses and resulting net income or loss for a period of time. An income statement is also called Statement of Operations, Earnings Statement, or Profit and Loss Statement (P/L). • A statement of changes in equity shows all changes in owner's equity for a period of time. This statement is also called Owners' Equity Statement. • A balance sheet presents assets, liabilities and owner's equity at a specific date. A balance sheet is also called Statement of Financial Position. • A cash flow statement summarizes information about cash outflows (payments) and inflows (receipts). This statement may also include certain information not related to actual cash flows.

ELEMENTS OF FINANCIAL STATEMENTS 1. • All financial statements consist of classes or categories known as elements. There are ten elements: assets, liabilities, equity, contributed capital, revenue, expenses, distributions, net income, gains, and losses Assets are economic recourses of a business used to accomplish its main goal, i.e., increase owners' wealth. To be formally recognized as an asset, the following two conditions must be met: • potential economic benefit must be assignable to a particular entity, and • event giving rise to the assignment must have already occurred. For example, if a company has purchased a piece of equipment and uses it in generating profits, it is considered as an asset. However, if the company just considers buying new equipment, it can't be deemed or recorded as an asset.

BASIC ACCOUNTING EQUATION • A company's assets belong to the resource providers who are said to have claims on the assets. • In other words, each asset has its own source provided by an owner or creditor. So, there can't be any claim without an appropriate asset and vice versa. Based on the previous statement, we can define the basic accounting equation: Assets = Claims • Claims are divided into two categories: • Creditors' claims that are called liabilities • Owners' claims that are called equity Assets = Claims (Liabilities + Equity)

NET ASSESTS = RESIDUAL EQUITY • Liabilities are debts and obligations of a company. • Equity is what the company "owes" to owners. • The amount of total assets minus total liabilities equals equity. Because equity equals the difference between assets and liabilities, it is also called net assets. • If a company goes bankrupt, liabilities are paid off first to creditors, while equity is the last to be distributed. Therefore, owners' equity is also called residual equity. Let us look at an example of the basic accounting equation. Suppose Our Company has assets of $800, liabilities of $300, and equity of $500. These amounts will be shown in the basic accounting equation as follows: Illustration 1: Example of basic accounting equation: Assets=Claims (Liabilities + Equity) $800 = ( $300 + $500 ).

BOOKKEEPING: DOUBLE ENTRY • 1) Friends Company is created when the owners pool $5,000 into the business. The effect of the contributions on the accounting equation is as follows: • Illustration 2: Effect of cash contribution: Claims Assets = Liabilities + Equity +$5,000 = + +$5,000 • Note that the amount of this single transaction is recorded twice. The first time it is recorded as an asset and the second time it is recorded as the asset source (equity). Here is a rule: Any transaction is recorded at least twice. This rule is known as double-entry bookkeeping.

EFFECT OF BORROWING • Double-entry bookkeeping rule states that any transaction is recorded at least twice. • Because this transaction provided assets to the enterprise, it is called an asset source transaction. An asset source transaction is one of the four types of accounting transactions. • Asset source transactions result in an increase in an asset account and in one of the claim accounts (liability or equity accounts). • 2) Next, assume that Friends Company acquires additional $2,000 of assets by borrowing cash from creditors. This is also an asset source transaction. In the table below the beginning balances are derived from the ending balances of the previous transaction: • Illustration 3: Effect of borrowing Claims Assets = Liabilities + Equity • Beginning balance $5,000 = + $5,000 • Effect of borrowing +$2,000 = +$2,000 • Ending balance $7,000 = $2,000 + $5,000

EQUITY: CONTRIBUTED CAPITAL & RETAINED EARNINGS • Equity is usually viewed as a source of assets, and that's why it becomes necessary to subdivide the owner's' interest into two components. First, owner's claims are established when a business acquires assets from owners. These claims result from the contributions of capital resources by the owners, and therefore they are frequently called contributed capital. • Contributed capital is a component of equity resulting from contributions of capital resources from owners. • The second source of assets associated with equity occurs when a business obtains assets through its earnings activities and is called retained earnings. • Retained earnings form a component of equity resulting from earnings activities. • Taking into account above definitions, the basic accounting equation can be presented like this: Assets= Liabilities + Equity (Contributed Capital +Retained Earnings)

EFFECT OF REVENUE • An increase in assets resulting from rendition of goods or services to customers is called revenue. • Earning revenue can also be an asset source transaction. To illustrate the effect of a revenue transaction, assume that Friends Company received $3,000 cash for services it provided to customers (note that both assets and retained earnings increase - asset source transaction): Illustration 4: Effect of revenue recognition Equity Assets =Liabilities + Contributed Capital+Retained Earnings • Beginning balance $7,000 = $2,000 + $5,000 + $0 • Effect of revenue +3,000 = + + +3,000 • Ending balance $10,000 = $2,000 + $5,000 + $3,000

ASSET USE • As noted, assets acquired in operating activities are called revenues. Assets used in the process of generating revenues are called expenses. • Expenses decrease retained earnings. Assume Friends Company used $1,000 in assets to earn $3,000 in revenues. This is an example asset use transaction. • Asset use transactions result in a decrease in an asset account and in one of the claim accounts (liability or equity accounts). • The affect of this asset use transaction (assets and claims decrease) on the basic accounting equation is as follows:

EXPENSE: REDUCES ASSETS & CLAIMS Take a note of how decreases or negative amounts are shown in accounting records. Instead of prefixing a minus sign ("-"), a number is taken into parenthesis. This is a common way of showing a decrease in the accounting realm.

DISTRIBUTION • If a business chooses to transfer part of its assets (retained earnings in particular) to the owners, the transfer is called distribution. Assume Friends Company transfers $500 of assets to its owners. This is an asset use transaction: • Distribution and expenses both result in decreases in retained earnings and thus, in equity.

PERMANENT ACCOUNTS • At the end of a period, all accounts are prepared for the next period. It is important to distinguish between permanent and temporary accounts. Balance sheet accounts (i.e., assets, liabilities, and equity) have a continuing nature; thus, they are not closed after each period and that's why they are called permanent accounts. • Permanent accounts are balance sheet accounts. They are not closed each period. Their balances are carried forward into the next period. Permanent accounts are also called real accounts. • In contrast, revenue, expense, and distribution accounts are used to collect information about a single accounting period. At the end of a period, amounts in revenue, expense, and distribution accounts are transferred to Retained Earnings. Accordingly, the revenue, expense, and distribution accounts must have zero balances at the end of one accounting period (after closing the books) and at the beginning of the following period.

TEMPORARY ACCOUNTS & CLOSING • Temporary accounts are closed at the end of each period. These are mostly income statement accounts, except for a distribution account that is equity statement account. Temporary accounts are also called nominal accounts. • The process of transferring the balances from the temporary accounts to the permanent account, Retained Earnings, is referred to as closing the accounts or closing the books. • Based on the five transactions described, we can now prepare the financial statements for the period. Recall that there are four general-purpose financial statements: • Income Statement • Statement of Changes in Equity • Balance Sheet • Statement of Cash Flows

INCOME STATEMENT ORIENTATION • The income statement measures the change in net assets or the difference between assets increases and assets decreases. The asset increases from the operating activities were labeled revenues. The asset decreases were called expenses. The difference between revenues and expenses is called net income (if revenue is greater than expenses) or a net loss (if vice versa). • Net income is the excess of asset increases (revenues) and asset decreases (expenses) for a period. Note that distributions do not fall under expenses caption and thus are not used in calculating the net income. • Net loss is the opposite of net income. Net loss results from the excess of asset decreases (expenses) over asset increases (revenues) for a period.

STATEMENT OF CHANGES IN EQUITY ORIENTATION • The statement of changes in equity explains the effects of transactions on owner's equity during an accounting period. The statement includes the beginning and ending balances of contributed capital and reflects any new capital acquisitions made during the accounting period. The statement also shows the portion of net earnings retained in the business.

BALANCE SHEET ORIENTATION • The balance sheet lists assets and corresponding claims (liabilities and equity). Any asset has a source, so assets balance with claims. That is why total assets equal total claims (liabilities and equity).

STATEMENT OF CASH FLOWS ORIENTATION • The statement of cash flows explains how the company obtained and used cash during a period. Sources of cash are called cash inflows, and uses of cash are known as cash outflows. • Cash inflows are sources of cash; for example, payments from customers, capital acquisitions, etc. • Cash outflows are uses of cash; for example, payments to vendors, paying off bank loans, etc.

HORIZONTAL ACCOUNTING MODEL • Let us demonstrate the usefulness of the horizontal model and apply it to the five transactions we covered before. Note that if a transaction does not affect the model, a related cell will show "n/a" in it. In the statement of cash flows, FA means cash flows from financing, IA means cash flows from investing, and OA means case flows from operating activities. • Obtained capital acquisition: $5,000 • Borrowed cash: $2,000 • Received cash revenue: $3,000 • Paid expenses with cash: $1,000 • Distributed cash to owners: $500 Using horizontal model helps a lot in understanding the effects produced by each event, so it is advisable to use it as often as possible while learning principles of financial accounting.

ACCOUNTING EVENTS & EFFECTS • With respect to Events No. 1 and 2, it is clear that only the balance sheet and statement of cash flows are affected. There is no effect on the income statement. Furthermore, you can see that Event No. 1 increases assets and equity and that the cash inflow is defined as a financing activity. Event No. 2 has a similar effect, except that liabilities increase instead of equity. Event No. 3 affects three financial statements. Assets and equity increase on the balance sheet. The recognition of revenue causes net income to increase, and the cash inflow is shown as an operating activity on the statement of cash flows. Event No. 4 is the opposite of Event No. 3. Assets, equity and net income decrease. Cash flow statement shows this decrease as an operating activity. Finally, Even No. 5 acts to decrease cash and equity. The cash distribution is not shown anywhere in the income statement. That's because distribution is not an expense and thus, is not included in the determination of net earnings. Cash distribution is categorized as a financing activity in the cash flow statement.