Download

1 / 58

590 likes | 723 Views

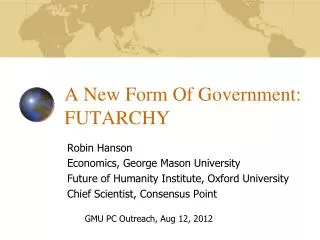

A New Form Of Government: FUTARCHY. Robin Hanson Economics, George Mason University Future of Humanity Institute, Oxford University Chief Scientist, Consensus Point. GMU PC Outreach, Aug 12, 2012. “Pays $1 if Obama wins”. Will price rise or fall?. sell. E[ price change | ?? ]. buy.

E N D

A New Form Of Government: FUTARCHY Robin Hanson Economics, George Mason University Future of Humanity Institute, Oxford University Chief Scientist, Consensus Point GMU PC Outreach, Aug 12, 2012

“Pays $1 if Obama wins” Will price rise or fall? sell E[ price change | ?? ] buy price sell Lots of ?? get tried, price includes all! buy Buy Low, Sell High

Current Event Prices 50-65% August US Unemployment 8.3% or more 58-59% Obama is re-elected in 2012 19-24% Greece defaults by 2013 11-16% Portugal defaults by 2013 6-9% Spain defaults by 2013 51-53% Syria’s al-Assad out by 2013 20-29% US or Israel strike Iran by 2013 12-50% Category 4 or bigger storm hits US in 2012 7-10% Cap & trade for US emissions by 2014 51-60% Nation using Euro drops it by 2014 61-85% Global ave temp higher in 2019 than 2009 InTrade.com

Beats Alternatives • Vs. Public Opinion • I.E.M. beat presidential election polls 709/964 (Berg et al ‘08) • Re NFL, beat ave., rank 7 vs. 39 of 1947 (Pennock et al ’04) • Vs. Public Experts • Racetrack odds beat weighed track experts (Figlewski ‘79) • If anything, track odds weigh experts too much! • OJ futures improve weather forecast (Roll ‘84) • Stocks beat Challenger panel (Maloney & Mulherin ‘03) • Gas demand markets beat experts (Spencer ‘04) • Econ stat markets beat experts 2/3 (Wolfers & Zitzewitz ‘04) • Vs. Private Experts • HP market beat official forecast 6/8 (Plott ‘00) • Eli Lily markets beat official 6/9 (Servan-Schreiber ’05) • Microsoft project markets beat managers (Proebsting ’05) • XPree beat corp error, 3.5 vs 6.6%

“Prediction Market Accuracy in the Long Run” Joyce Berg, Forrest Nelson and Thomas Rietz, Jan. 2008.

Iowa Electronic Markets vs. Polls “Accuracy and Forecast Standard Error of Prediction Markets” Joyce Berg, Forrest Nelson and Thomas Rietz, July 2003.

Iowa FluMarkets Clinical Infectious Diseases 2007:44 (15 January)

Back in 2003 … Policy Analysis Market • Every nation*quarter: • Political stability • Military activity • Economic growth • US $ aid • US military activity • & global, special • & all combinations

The Fuss: Analysts often use prices from various markets as indicators of potential events. The use of petroleum futures contract prices by analysts of the Middle East is a classic example. The Policy Analysis Market (PAM) refines this approach by trading futures contracts that deal with underlying fundamentals of relevance to the Middle East. Initially, PAM will focus on the economic, civil, and military futures of Egypt, Jordan, Iran, Iraq, Israel, Saudi Arabia, Syria, and Turkey and the impact of U.S. involvement with each. [Click here for a summary of PAM futures contracts] The contracts traded on PAM will be based on objective data and observable events. These contracts will be valuable because traders who are registered with PAM will use their money to acquire contracts. A PAM trader who believes that the price of a specific futures contract under-predicts the future status of the issue on which it is based can attempt to profit from his belief by buying the contract. The converse holds for a trader who believes the price is an over-prediction – she can be a seller of the contract. This price discovery process, with the prospect of profit and at pain of loss, is at the core of a market’s predictive power. The issues represented by PAM contracts may be interrelated; for example, the economic health of a country may affect civil stability in the country and the disposition of one country’s military may affect the disposition of another country’s military. The trading process at the heart of PAM allows traders to structure combinations of futures contracts. Such combinations represent predictions about interrelated issues that the trader has knowledge of and thus may be able to make money on through PAM. Trading these trader-structured derivatives results in a substantial refinement in predictive power. [Click here for an example of PAM futures and derivatives contracts] The PAM trading interface presents A Market in the Future of the Middle East. Trading on PAM is placed in the context of the region using a trading language designed for the fields of policy, security, and risk analysis. PAM will be active and accessible 24/7 and should prove as engaging as it is informative. Became:

Terror Betting Is “Unthinkable” • We deny our “Taboo Tradeoffs” (P. Tetlock) • E.g., money vs. risk of death • Outraged at those we see do (really, we all do) • More outraged if they think a long time first • If catch ourselves, seek moral cleansing • PAM painted as crossing a moral boundary • “None of us should intend to benefit when some of them hurt some of us.” • So politicians must not think long before rejecting

PAM Press Of 500+ articles, these gave more favorable PAM impression: Article: later in time, more words, mentioned insider, news (not Editorial) style, not anonymous Publication: finance or science specialty, many awards, many readers

100s of Firm Markets Now • Sales - HP, Google, Nokia, XPree, O’Reilly, Best Buy • Deadlines - Siemens, Microsoft, Misys • Pick Project - Qualcomm, GE, Lily, Pfizer, Motorola, Intercontinental Hotels • Unknown - Novartis, GSK, Motorola, ArcelorMittal, Corning, Dentsu, Masterfoods, Thomson, Yahoo, Abbott, Chrysler, Edmunds, InfoWorld, FritoLay, Erickson, IHG, NBC, HVG, RAND, SAIC, SCA, TNT, Cisco, General Mills, Swisscom

To Evaluate Institutions Institution A Institution B When They Use Similar Inputs Compare Quality Of Outputs

Collective Forecasting Forecasts On Requested Topics User Contributions User Scores Engagement

Advantages Incentives Self-Selection Correct Biases • Numerically precise • Consistent across many issues • Frequently updated • Hard to manipulate • Need not say who how expert when • Issue is not experts vs. amateurs • At least as accurate as alternatives

Requirements Use: • Questions really want answered now • Will eventually know answer (or parts) • Suspect not getting frank info via usual channels • Don’t mind participants knowing best estimates • People with access to key info • A few can be fine; their time is main cost • Little penalty for invite many don’t know • Incentives to entice participation • Money, attention, influence can legally offer • Valued when questions answered • Many fast questions, status quo estimates Validate:

Typical Prediction Market Scenario • Champion puts on mantle of “innovator” • Avoids most interesting, valuable topics • Forecasts more accurate, users satisfied • Typical Outcomes: • Someone embarrassed, project killed, or • Champion moves, project dies, or • Continues, off key topics, weak interest

Puzzling Disinterest • On prediction markets, most accept accuracy claims, yet still reject • Most thought wanted it find it works, but don’t want • Similar disinterest in prediction track records • Similar disinterest in randomized experiments • Forecasting orgs poorly funded, little noticed • Common issues: • Bad: visible track record of failure warnings • Bad: boss less seen as key info clearinghouse • Bad: hard to manipulate perceptions to motivate effort

Manager As Politician • Myth: manager as scientific decider • Reality: mainly build, maintain coalitions • Signal solid wide support, avoid cracks • Avoid clear records of failure warnings • Avoid signs that changed mind

A Catechism “X is not for Y” = “Y is not the main function of X.” Food isn’t for Nutrition Clothes aren’t for Comfort Marriage isn’t for Romance Talk isn’t to Gain Info Laughter isn’t about Jokes Charity isn’t about Helping Sports aren’t for Exercise Church isn’t about God Art isn’t about Insight Medicine isn’t for Health Consulting isn’t for Advice Investing isn’t for Returns School isn’t for Learning Research isn’t for Progress Leading isn’t about deciding Politics isn’t about policy

Collective Forecasting Questions Consensus What exactly is my influence? What exactly are my incentives? My Forecast My Score How exactly do I express my opinion? Truth

Editing Interface Is Transparent If my edit increases the consensus chance of true state, I win. If decreases, I lose. I directly change the consensus Consensus My Edits My Score Truth

Imagine Combo Dashboard Ave. Worth: $12,459 Coming soon from Consensus Point

Ask For Detail Ave.Worth: $12,459 Them B Ship Date 2009 2010 J F M A M J J A S O N D

Make An Edit Ave. Worth: $12,459 If We Have Autozoop, you gain $53 But if We Don’t Have It You lose $78. OK?

Make an Assumption Scenario: 15% Ave. Worth: $10,724

Add 2nd Assumption Scenario: 2.3% Ave. Worth: $10,982

Edit As Before Scenario: 2.3% Ave. Worth: $10,724 If we have Autozoop, you gain $53 But if we don’t have it You lose $78. OK?

Combo Market Maker Best of 5 Mechs 3 subjects, 7 prices, 5 minutes 6 subjects, 256 prices, 5 minutes

KL(prices,group) 1- KL(uniform,group) MSR Info vs. Time – 255 prices 1 % Info Agg. = 0 0 5 10 15 Minutes -1

Edit-Based Combo System Needs • User u chooses assumptions A, target event T • Find & show to user u (who has assets Su): • Current consensus p(T|A) • Now long/short? Via: Ep[Su|A&T]-Ep [Su|A¬T] • Limits [min,max] of new p’(T|A), to ensure Su ≥ 0 • User u aborts or picks a p’(T|A) in [min,max] • Update p to reflect p(T|A) -> p’(T|A) • Update assets Su to reflect bet for p’ over p • Periodically show how Ep[Su] varies with u If raise p win lose

Bayes/Markov Nets P(Clique | Rest of Net) = P(Clique | Its Separators) BL Clique • Probabilities In Product Form: px = c pc(xc) / s ps (xs) • Lets compute in space linear in # cliques, exp. in size • If Tree, Junction Tree algorithm lets compute linear in # cliques • We’ve shown that in LMSR, assets, expected assets also! • If edit p(T|A) -> p’(T|A), need T,A in same clique • DAGGRE.org is IARPA project at GMU • Now fielding this for 100s of users, questions • Come join! LE T Separator BE E SBL BLE AT TLE XE DBE

$1 if Lifespan Up & Single Payer P(L | S) Compare! P(L | not S) $1 if Not Single Payer $1 if Lifespan Up & Not Single Payer P(not S) Single Payer Decision Markets P(S) $1 if Single Payer $1

Policy Applications E[ Lifespan | Single Payer Health? ] E[ Lifespan | Stricter Air Quality Regs? ] E[ f(inflation,unemploy) | Fed raise rates? ] E[ Student test scores | School voucher? ] E[ red team in | new building security? ] E[ US terror deaths | halve DHS budget? ] E[ Unemployment | Demo. Pres. ’12? ] E[ firm stock price | dump CEO? ]

2008 US President Example From InTrade.com

Legal permission Outcome Measured Aggregate-enough Linear-enough Conditional-enough Decision Distinct options Important enough Enough influence Public credibility Traders Enough informed Decision-insiders Enough incentives Anonymity Prices Intermediate-enough Can show enough Decision Market Requirements

Three Premises and a Conclusion • It is not too hard to tell rich happy nations from poor miserable ones long after the fact. • Governments largely fail by not aggregating available information. • Speculative markets are our best known institution for aggregating information. • Try to vote on values, but bet on beliefs.

Plain Democracy Passed Bills => Laws

Vote On Values But Bet On Beliefs E[ National Welfare | Alternative ] >? E[ National Welfare | Status Quo ]

Futarchy’s One Rule When a market estimates currently-defined National Welfare to be higher given some proposed alternative policy, that policy is law. • Unless market on future-defined NW vetoes it • Start with existing policies, fee to propose change • Like contract, proposal says how handle conflicts • High standards at base, recurse to relax standards • Treaties could agree to include other nation’s NW. http://hanson.gmu.edu/futarchy.html

Ideologically Neutral? “Capitalists will sell us the rope to hang them” • Expect savvy selfish capitalists to bet beliefs, even if hurts class interest • Is market, but can endorse regulation

Issues In Defining National Welfare Claim: GDP futarchy beats current democracy. (Few-% time-discounted average of log GDP) • Risk aversion, time discounting • Leisure, environment, art, lifespan • Inequality, population, foreigners • Counting moral outrages

Issues In Defining Official Prices • Valid “banks” issue contingent assets • Valid “cash” contingent assets pay off in • Valid “marketplace” guarantees offer • “Enough” difference: size, duration, breadth • Valid judges of whether alternative tried

Intuitive, Common Rich get more “votes” Buy policy via market Market bubbles More lies, secrecy Do harm to win bets Forgo popular illusions Regarding Natl. Welfare Policy in NW defn. Max NW meas. errors Slow catch NW bugs Corrupt NW measure More when more care Concerns about Futarchy

Same As Democracy Guarantee rights Time-inconsistency Induce policy cycling Expressive voting Too many policies Military needs secrecy Losers fight transition Economics, Technical Markets too thin Most policy too small When “clear” diff. What if destroy Earth Infinity never comes Risk premia distortion Decision selection bias More Concerns

Vote On Values But Bet On Beliefs E[ National Welfare | Alternative ] >? E[ National Welfare | Status Quo ]

Info Leaks • Prices may inform rivals, alarm public • Traders now don’t know prices at order • Deal via: Limit orders, market orders, … • Can extend this to show less about price • Hide prices for a time delay after trade? • Orders can say how respond to price history • Trusted traders see actual prices?