Download

1 / 28

280 likes | 297 Views

This report evaluates the current and future patterns in electricity supply and demand in Latin America and the Caribbean region. It provides information on historical and projected installed capacity and generation, as well as the sources of information used. Additionally, it discusses how the region will pay for the investments required to meet the demand for electricity.

E N D

INTER-AMERICAN DEVELOPMENT BANK LAC ENERGY & ENVIRONMENT CANADA SEPTEMBER 2015

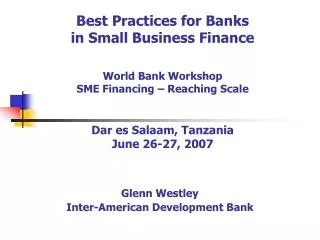

LACEnergyMatrix MillionBarrels of Oilequivalentperday,MBOe/d World LAC NorthAmerica Europe Source: EnergyInnovationCenterat theIDB

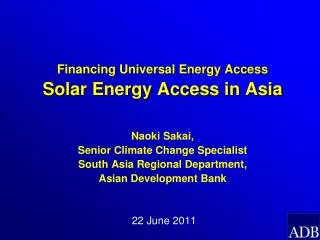

OilPriceOutlook %GDP NetOil Exporters (2014) Source:http://www.worldbank.org Source: WorldBank Source: IMFWorldEconomic Outlook

Affordability: Estimated Electricityprices(US$ cents/kWh- 2011) Source:OLADEElectric Tariffsin LAC2011,IEAElectricityInformation2012

Reliability:Estimated LACElectricityLosseslatest5yearaverage(%) Source:Jimenez,SerebriskyandMercado2014, IEA2012

Estimating Forecasting LAC-7 • Evaluated regional and country current & future patterns in Electricity installed capacity & generation • Sources of information Historical installed capacity and refinery capacity from Energy Information Administration (EIA) Official data for future installed capacity, Projected installed capacity according to official expansion plans. 22 23 24 25 26 27

Electricity Supply& Demand 3,000 Actual Data Forecasts(official) LAC Generation from hydro is 39% of total generation, while fossil fuels represent 55% of total generation and other sources account for 6% 2,500 By 2025, fossil fuel generation will be 59%, followed by hydrogeneration at 33%, and other sources will be 8% of total generation for Latin America. How will we pay for the investments required? Generation(TWh) 2,000 1,500 ProjectedDemand 1,000 500 0 2025 2024 2023 2022 2021 2020 2019 2018 2017 2016 2015 2014 2013 2012 2011 2010 2009 2008 2007 2006 2005 2004 2003 2002 2001 2000 1999 1998 1997 1996 1995 1994 1993 1992 1991 1990 1989 1988 1987 1986 1985 1984 1983 1982 1981 1980 Others (Biomass, Nuclear, Wind, Solar, Geothermal) Hydr Fossil Fuels (Gas, Diesel, Others (Biomass, Nuclear, Wind, Solar, o Coal) Geothermal) Fossil Fuels (Gas, Diesel, Coal) Hydro Sources:1986-2013–IEA; 2013-2030–INE/ENE

LACEnergyMatrix2012Thousands of BarrelsofOilequivalentperday,kBOe/d 68% www.iadb.org/energydatabase

How IDB works with the private sector • Strengthening medium & large scale sustainable investments. • Supporting growth of small & medium enterprises. • Expanding access to finance, markets, basic services & green growth. • Financing innovative business models that serve the base of the pyramid

IDB’s financial products and services • Senior and subordinated loans • Syndicated loans • Partial credit guarantees • Equity and quasi equity • Capacity building & knowledge creation • Partnerships

Who are IDB’s private sector clients Financial Intermediaries Companies • Micro, small and medium enterprises • Large corporates and state-owned enterprises • Special purpose vehicles • International and local banks • Investment funds • Microfinance institutions Non-profit and other organizations

NSG Portfolio -- December 2014 Infrastructure 36% Financial Markets 33% Industries & Services 29% Social Infrastructure 2%

Water supply • Water and waste treatment • Energy efficiency • Renewable generation (Wind, Solar, Geothermal) • Service improvements to energy transmission • Focus on low access • Toll Roads • Airports • Ports • Increase capacity & access • International safety standards Key NSG Lending Priorities Water & Sanitation Energy Transportation Sustainability

Project Type: Eurus Wind Farm Project in Mexico EURUS First large scale wind farm in Mexico Location: Mexico Approval: 2009 Cost: US$600 million IDB Loan: US$45 million plus US$30 million CTF Sponsor: Acciona And largest operating wind project in the Latin America.

Project Type: Hydroelectric Project in Costa Rica REVENTAZON Innovative financial structure Location: Costa Rica Approval: 2010 Cost: US$1.44 billion IDB Loan: US$200 million Loan + Guarantee Sponsor: ICE B loan funded by institutional investors. Project will represent 10% of CR energy’s installed capacity

Project Type: First operational large wind farm in Uruguay PALMATIR Catalyzing non conventional renewable energy Location: Uruguay Approval: 2012 Cost: US$153 million IDB Loan: US$42 million Sponsor: Abengoa Bankability enhancements helped mobilize investments in UR renewable energy (US$2.3 bn). Tracking CO2 emissions through supply chain

Project Type: Corporate Loan EGP EGP Mexico Supporting EGP’s investments in a 74MW wind farm in Oaxaca, Mexico Location: Mexico Approval: 2012 Cost: US$169 million IDB Loan: US$76 million Enel’s Bii Nee Stipa project will contribute to Mexico’s goal of reducing 50 % of its greenhouse gas emissions by 2020

Project Type: Photovoltaic Solar Power in Atacama Desert POZO ALMONTE Giving solar power a boost Location: Atacama, Chile Approval: 2013 Cost: US$82.7 million IDB Loan: US$21 million + C2F 21 million Sponsor: SolarPack First large-scale solar power plants in Chile. Contributing to reducing CO2 emissions by 56,000 tons per annum

B Loan Program Participation Agreement Loan Agreement Borrower Participants IDB B Loan A + B Loans • One loan agreement – IDB is lender of record and administers entire loan • IDB and B Lenders as Senior Lenders • Participation structure allows participants to benefit from IDB’s privileges and immunities

Canadian Climate Fund - C2F “Mountain of Defeat” - High and uncertain costs for early commercial projects

IDB’s value proposition • Sector and financial expertise with regional knowledge • Long term financing with tailored repayment schedules • Competitive financial products and terms • Ability to mobilize additional sources of financing or support: B loans, co-loans, China Funds, C2F • Exemption from withholding taxes and de facto preferred creditor status • Environmental and social leadership • Shared value, innovation, outreach and dissemination

Five things you need to know about the IDB and Sustainability • We are delivering on our sustainability commitments: Thirty-three percent of IDB lending in 2014 targeted environmental sustainability, climate change initiatives and renewable energy, totaling US$4.4 billion. • We are adding value to our projects through the implementation of safeguards, to minimize environmental and social harm and to maximize positive environmental and social outcomes of our work: 88% of projects with high environmental and social risks rated satisfactory in safeguard mitigation measures. • We are implementing a new strategy and vision for sustainable infrastructure, one that sees a shift from infrastructure being a fixed asset to infrastructure that is planned, built, and maintained as a service for people. • We innovate through special initiatives that support the sustainability agenda: we place an emphasis on urban sustainability through the Emerging and Sustainable Cities Initiative, and we continue to leverage support from the Climate Investment Funds, the GEF and various donor agencies. • We are improving gender and diversity mainstreaming: incorporating gender related results and sex-disaggregated indicators into more of our projects, to ensure that the benefits are felt by all.