Download

1 / 36

360 likes | 374 Views

Learn about education tax benefits, including the American Opportunity Tax Credit and Lifetime Learning Credit, and how to calculate eligible expenses. Help students and their families claim the federal tax benefits they deserve to pay for higher education.

E N D

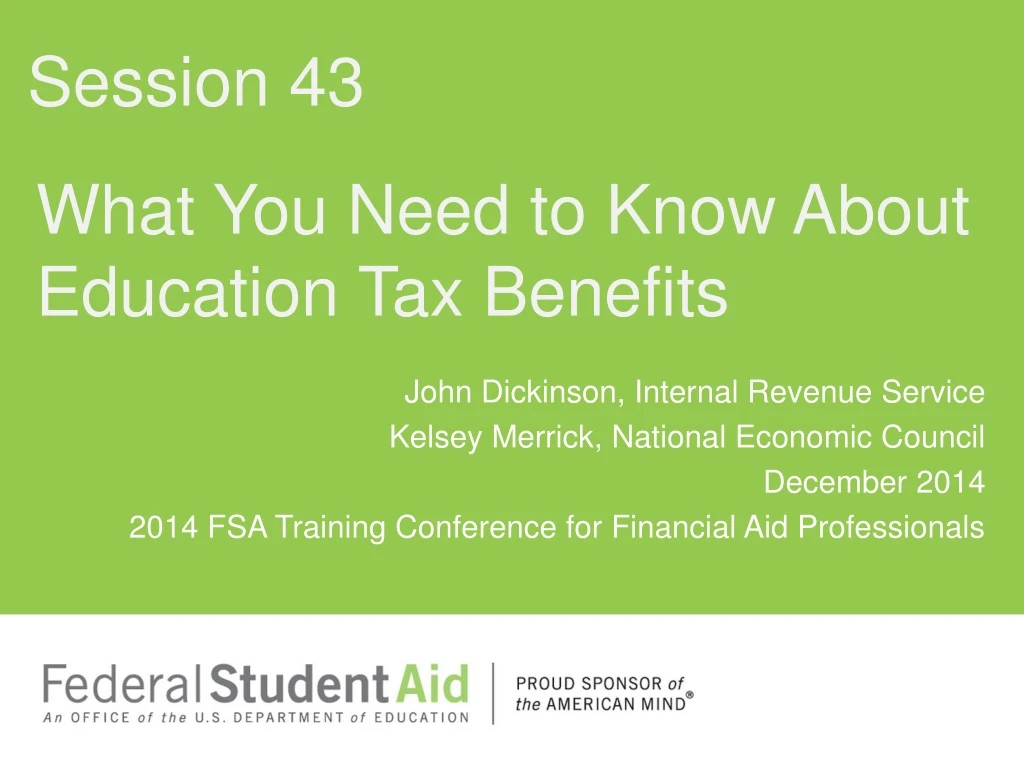

Session 43 What You Need to Know About Education Tax Benefits John Dickinson, Internal Revenue Service Kelsey Merrick, National Economic Council December 2014 2014 FSA Training Conference for Financial Aid Professionals

Overview • Education tax benefits are a major source of federal financial aid • Knowing about these credits benefits your students, their families and your school • Calculating eligible expenses for each provision varies by student and credit • Help all those who qualify receive the federal tax benefits they deserve and need to help pay for higher education • Claiming education credits can be complex, and some families leave money on the table

Education Tax Credits • American Opportunity Tax Credit • Lifetime Learning Credit

Who Benefits from Credits? Source: Office of Tax Policy, US Treasury for Tax Year 2011

Who Qualifies? The student must meet all three of the following: • Pay qualified expenses of higher education • Pay the education expenses for a qualified student • Must pay the expenses for themselves, their spouse, or for a dependent

Who Does Not Qualify? The student cannot claim the credit if any of the following are true: • Files married filing separately • Is listed as a dependent on another person’s return And….

Education Credits and Foreign Students • F1 Student Visa • Is a nonresident alien • Married to a nonresident alien

Basic Qualifying Education Expense Requirements • Must generally be paid during the tax year (Jan-Dec). • For tax year 2014, qualifying expenses must be for an academic period beginning in 2014 or the first three months of 2015 • Primarily, tuition and fees required as part of the student’s enrollment. For AOTC only, books are also a qualified expense. • Do not include: • Room and board • Transportation • Personal, living, or family expenses • Insurance • Medical expenses (including student health fees) • Sports, games, hobbies, and noncredit courses unless included in course of instruction • Payments refunded to the student if they withdraw from courses

Funds that Qualify Expenses paid by the following income sources can be qualifying expenses for education tax credits: • Payments for services, such as wages • A loan • A gift • An inheritance, or • A withdrawal from student’s personal savings • Taxable scholarships or fellowships

Expenses that Do Not Qualify • Insurance • Medical expenses (including student health fees) • Room and Board • Transportation • Personal, Living, or Family Expenses • Sports, games, hobbies, and noncredit courses unless included in course of instruction

Form 1098-T is… • Filed annually by nearly all post-secondary education institutions for most students • Used by IRS to verify education spending for education related tax benefits • Form 1098-T may not list all the information a student/parents need for claiming an education credit

Education Benefits and 1098-T (2010-2011) 26% of returns claiming AOTC have no Form 1098T. 37% of returns1 with 1098T claim no benefit. 1 Returns in income range for tuition deduction

Form 1098-T and Claiming a Credit • Use Form 1098-T as a guide • Student/parents make the choice which dollar of expense is used for which benefit • For tax purposes schools do not determine the best way to allocate expenses across benefits – this is for the student to do

Scholarships and Education Credits • No double benefit: Tuition and related expenses paid for with scholarships or grants do not qualify for education credits in order to prevent double benefits for the same expenses. • Trade-off between qualified expenses for education credits and taxability of grants: Scholarships and grants allocated to tuition and related expenses are tax-free, but they may also reduce the value of education credits. (If allocated to living expenses, grants are counted as taxable income.) • Taxpayers can choose how to allocate their scholarships and grants for tax purposes, regardless of how the institution allocated the funds (as long as the choice is in accordance with the terms of the scholarship or grant).

Scholarships and Education Credits • Students at low-cost institutions are more likely to be affected by this trade-off: • Up to $4,000 in qualified expenses can be used to claim the AOTC and up to $10,000 in qualified expenses can be used to claim LLC. • Students with tuition and related expenses in excess of these amounts will have at least some qualified expenses to claim an education credit, regardless of whether they allocate their scholarships and grants to tuition and related expenses or to living expenses.

Pell Grants and AOTC • The AOTC made education credits available to many Pell Grant recipients for the first time. • Pell Grant recipients can face complicated decisions at tax time and, in total, forgo hundreds of millions of dollars in education credit each year. • Even if a student’s Pell Grant fully covers tuition and related expenses, the student may still have unmet need for living expenses. • These taxpayers must choose between claiming an education credit and making their Pell Grant taxable

Pell Grants and AOTC • Many students do not realize that they have this choice, and that they could increase their AOTC by treating a portion of their Pell Grants as taxable income. • Most Pell Grant recipients should claim at least $2,000 in tuition and related expenses for the AOTC even if that means allocating some or all of their Pell Grant to living expenses and therefore including that amount as taxable income. • Beyond this rule of thumb, the right choice depends on the student’s and their family’s circumstances.

Scholarship Used to Pay Scholarship Used to Pay Living Expenses Tuition, Fees, and Books 5,645 5,645 Total Pell Grants Pell Used to Pay Tuition, Required Fees and Books 0 4,000 Pell Used to Pay Living Expenses 5,645 1,645 Expenses Eligible for AOTC (up to $4,000) 4,000 0 Total Income Parent 20,000 20,000 Taxable Income 3,000 3,000 Tax Before Credits 300 300 AOTC 1,300 0 EITC 2,958 2,958 1 Tax Liability of Parent -3,958 -2,658 Total Income Student (has $2,000 earnings) 7,645 3,645 Taxable Income 1,445 0 Tax Liability of Student 145 0 Total Tax Liability of Family -3,813 -2,658 2 Net Loss from Failing to Optimize Benefits 1,155 1 Negative values indicate that the family is receiving a refund. 2 The net loss from failing to optimize benefits equals the value of the foregone AOTC minus the tax the student avoids by using the Pell for tuition and excluding it from income. Example 1 • This family minimizes tax by including $4,000 of Pell as taxable income for the dependent student in order for the parents to claim $4,000 in qualified expenses for the AOTC.

Example 2 • This independent student minimizes tax by including $2,000 of Pell as taxable income in order to claim $2,000 in qualified expenses for the AOTC.

Save the Date!! Tax Credits Webinar: Its not just college credits its education credits too! December 8th, 2014

There are tools to help • IRS.gov – Tax Benefits for Education: Information Center • IRS.gov - Education Credits – AOTC and LLC • Publication 970, Tax Benefits for Education. • Form 8863, Education Credit Instructions • Publication 929, Tax Rules for Children and Dependents • IRS videos can be found at www.youtube.com. • Department of Education website at: https://studentaid.ed.gov/types/tax-benefits • Pub. 5081, Education Credit Online Resource Tool • To help determine if you are eligible for education credits, use the IRS’ Interactive Tax Assistanttool available on IRS.gov.

Resources On Grant/Credit Interaction • Treasury Blog Post: Helping students and families access college tax benefits http://www.treasury.gov/connect/blog/Pages/Helping-students-and-families-access-college-tax-benefits.aspx • Treasury Fact Sheet: Interaction of Pell Grants and Tax Credits: Students May be Foregoing Tax Benefits by Mistake http://www.treasury.gov/connect/blog/Documents/Pell%20AOTC%204%20pager.pdf • IRS Tax Benefits for Education http://www.irs.gov/pub/irs-pdf/p970.pdf

Reach out to us at: eitc.program@irs.gov