Download

1 / 26

0 likes | 12 Views

Capital structure refers to the mix of long-term financing sources a company utilizes, such as equity, debt, and reserves. By determining the ideal proportion of internal and external funding, a company can impact its Weighted Average Cost of Capital (WACC) and firm value. The optimal capital structure aims to maximize shareholder wealth while minimizing capital costs, enhancing investment opportunities. Factors like simplicity, risk management, liquidity, flexibility, cost efficiency, and returns on equity capital play key roles in determining an ideal capital structure.

E N D

INTRODUCTION Capital Structure means a combination of all long-term sources of finance. It includes Equity Share Capital, Reserves and Surplus, Preference Share capital, Loan, Debentures and other such long-term sources of finance. A company has to decide the proportion in which it should have its own finance and outsider’s finance particularly debt finance. Based on the proportion of finance, WACC and Value of a firm are affected. CAPITAL STRUCTURE DECISION A COMPANY’S FINANCING DECISION OR CAPITAL STRUCTURE DECISION IS CONCERNED WITH THE SOURCES OF FUNDS FROM WHERE LONG TERM FINANCE IS RAISED AND THE PROPORTION IN WHICH THE TOTAL AMOUNT IS RAISED USING THESE SOURCES OF FUNDS. IT INVOLVES DETERMINING HOW THE SELECTED ASSETS/PROJECT WILL BE FINANCED. BROADLY, FINANCING DECISIONS INVOLVE THE FOLLOWING THREE ISSUES- I. THE AMOUNT OF TOTAL LONG TERM CAPITAL REQUIREMENT. THIS IS RELATED WITH CAPITAL BUDGETING DECISION OF THE COMPANY. II. SOURCES OF FUNDS FROM WHERE FUNDS ARE RAISED. III. COMPOSITION OF TOTAL FUNDS I.E. THE PROPORTION OF EACH SPECIFIC SOURCE IN TOTAL CAPITALIZATION.

OPTIMUM CAPITAL STRUCTURE The main objective of financial management is to maximize the market value of equity shares. It is only by maximizing the market value of ordinary shares that the wealth of the shareholder is maximized. Management should choose such a capital structure so that the objective of financial management can be fulfilled. Such a capital structure or a mixture of debt and owner capital is called optimum capital structure so that the value the firm is maximum. Optimum capital structure maximizes the wealth of the shareholders on the one hand and minimizes the capital cost of the firm on the other. Due to lower capital cost, the firm gets new investment opportunities. Thus we see that there is a close relationship between the capital structure and the value of the firm. A company’s capital structure affects the value of a firm by affecting the company’s potential earnings or cost of capital, or both.

QUALITIES OF OPTIMUM OR A SOUND CAPITAL STRUCTURE Simplicity Minimum Risk Adequate Liquidity Flexibility Minimum Cost of Capital Maximum Return Full Utilization Control

1. SIMPLICITY The ideal or optimal capital structure should have a quality of simplicity. Here, simplicity means initially raising funds should be through few types of securities, meaning thereby that only equity and preference shares should be issued and debentures be issued, later on. Thus, diversification insecurities should be introduced gradually, along with the development of the business. It will add to the confidence of the investors and raising funds will become easy. 2. MINIMUM RISK Various risks are attached to every business, like, business competitions, changes in demand of the goods, natural climates, increase in taxes, increase in interest rates, reduction in purchasing power, increase in business cost, etc. These risks have an effect on planning and building up of capital structure. Hence, the capital structure should be such that these risks may be minimum and the burden thereof may be successfully borne by the business if so required. To minimize the risks, the component of high category securities in the capital structure is necessary.

3. FLEXIBILITY Capital structure is not determined only for the immediate needs of the enterprises, but also for long- term needs. Hence, the capital structure should be such that the funds may be raised in the future also to meet the increasing needs of the business. It should also be possible to reduce capital and funds when less capital is required. 4. ADEQUATE LIQUIDITY The composition of capital structure and assets of the institution should be such that the institution may always maintain adequate liquidity. Hence, the company may issue such debentures, which may be repurchased in the market and maybe resold in the market, when needed. In addition, these days system of issue of debentures having conditions of the repurchase is on increase for maintaining and adequate liquidity.

5. MINIMUM CAPITAL of COST Capital may be obtained by various sources and costs are to be incurred for every source, like underwriting commission, discounts, commission, advertisements, printing, interests or dividends, statements costs, expenses on transfer, etc. The capital structure should be such that the capital of the cost of capital collection is minimum. The costs of some sources are high and as low for some other sources. 6. MAXIMUM RETURN ON EQUITY CAPITAL We know that equity shareholders are the real owners of a company and only they bear the real risk on investments. So, the capital structure should be such that they may get the maximum returns (profits). But, it is possible only when the institution is able to have certain and adequate income, regularly. Although, accrual of this income must depend upon the efficiency of the managers. But, even then, income may be raised by procuring capital at low costs, by developing proper capital structure.

7. FULL UTILIZATION While making capitalization, the institution should keep it in view that the procured money is fully utilized, meaning thereby that the volume of capital should be so determined that the institution may neither have overcapitalization nor undercapitalization. Capitalization should be proper. When capitalization in the institution is proper, the capital sources of the institution do not remain idle and they are well utilized. 8. Maximum control generally, the right of control over the institution is in the hands of equity shareholders. But, this right may be transferred by giving voting rights to preference shareholders and debenture holders, in special circumstances. Hence, the capital structure of the institution should be such that the management and control of the company may remain secured in the hands of equity shareholders.

FACTORS AFFECTING CAPITAL STRUCTURE Size of business Form of business organization Stability of earnings Degree of competition Stage of life cycle Credit standing Corporate taxation State regulation State of capital market Attitude of management Trading on equity Cash flow ability of the company Cost of capital Flotation costs

1. SIZE OF BUSINESS:- Small business is face more difficulty in availing long term loans. if it is able to take a long term loan, it will be available at higher rate of interest and comfortable terms. the too restrictive terms of credit make the capital structure of small company in flexible and the management can not run the business independently without interference. therefor, small company’s depend of share capital and retained earnings to meet their long-term fund requirements. the cost of issuing share capital in small company’s is higher than in large company’s. in addition, the risk of losing control of the company’s increases with frequent issuance of equity shares to obtain long-term finance. the shares of a small company are not widely dispersed and a disgruntled section of shareholder’s can easily to take control of the company. for this reason, small companies sometimes do not allow their business to grow much and arrange their finances from retained earnings. large companies are able to take long-term loans on relatively easy terms and can issue ordinary shares and preference share to the public. the cost of issuance is also lower as compared to smaller companies due to the issue of higher amount of shares. therefor, while planning the capital structure, the company should make proper use of its size. 2. FORM OF BUSINESS ORGANIZATION:- In case of private company, sole business and partnership business, control principle is given more importance because in this the business is owned by lesser persons. This is not the case in public limited companies because other ownership is held by a large number of shareholders who are spread over a large distance.

3. STABILITY OF EARNINGS:- The stability of sales and earnings affects the amount of leverage. companies whose sales and earnings are stable in nature, such companies can use a higher amount of debt in their capital structure and can easily pay fixed financial charges. industries producing consumer goods tend to fluctuate more in sales and therefore use less credit. on the other hand, the sales and income of public utility institutions are stable and for this reason they use debt a lot to finance their assets. the potential increase in sales also affects the amount of leverage. the greater the potential for development, the greater the need for external funds. this is the reason why developing companies make more use of debt in their capital structure. companies whose sales are declining should not use excess debt or preference share capital in their capital structure as they may face difficulty in paying interest and preference dividends which may lead to winding up of the company. 4. DEGREE OF COMPETITION:- If the amount of competition in the industry is high, then the companies in such industry should use more common equity capital instead of debt. on the other hand, industries which do not have high competition, tend to have stagnant income and can use credit more.

5. STAGE OF LIFE CYCLE:- The stage of the life cycle of an industry is also an important factor affecting the capital structure. If the industry is in its infancy then it is more likely to fail. Therefore, in such a situation, more emphasis should be given on ordinary share capital. The firm can function properly if it does not issue securities on which it has to pay at a fixed rate. In such a situation the risk is high. When the company is going through a phase of rapid growth, the management should plan the capital structure in such a way that it can get finance on easy terms as and when required. If it reaches the stage of maturity, then it should be spent on the development programs of new goods and the finance should be done with ordinary share capital because there is uncertainty of growth in business income. If the level of business activity is likely to decrease in the long run, the capital structure should be planned in such a way that the excess funds can be returned. 6. CREDIT STANDING:- Companies whose creditworthiness is high in the minds of the investors and lenders, such companies can get finance on convenient terms from the means of their choice. If the company is not in good standing then the decision regarding obtaining finance becomes limited.

7. CORPORATE TAXATION:- Due to the existing provisions relating to tax, the use of loans in the capital structure of the company is cheaper than ordinary share capital or preference share capital because interest on loans is deducted from taxable income, whereas such exemption is not available for dividend. The tax level affects the capital cost. Therefore, in order to take advantage of trading on equity, the management uses more debt funds in the capital structure, thereby increasing the income available to ordinary shareholders. 8. STATE REGULATION:- Decisions regarding capital structure are also influenced by the provisions related to government control. In India, the debt-equity ratio was fixed for companies in the control of capital issues act. Similarly, the maximum rate of interest on debentures was also fixed. Guidelines have also been fixed for release of bonus shares. Since 1992, the capital issue was controlled by SEBI. The management should keep these provisions in mind while planning the capital structure.

9. STATE OF CAPITAL MARKET:- While taking decisions regarding capital structure, the trend of capital market should be kept in mind as it affects the cost of capital and availability of finance from different types of resources. Sometimes the company wants to issue equity shares, but due to high risk, the investors do not want to invest in that company, then in such a situation the company should not issue shares and should get necessary finance from other means. Therefore, the proper timing of issue of securities to the public is an important factor in influencing the capital structure of the company. The currency and tax policies of the government are also important in this matter. If the management realizes that debt funds will become costly in future, it should get the necessary finance from debt instruments at the earliest. Due to the possible reduction in the rate of interest, the management can take advantage of the lower rate of interest in future by getting finance from other sources at present. 10. ATTITUDE OF MANAGEMENT:- What is the attitude of the management towards the various elements affecting the capital structure, this element also affects the capital structure. Management's attitude towards control and risk should be analyzed. Some managers do not want to take too much risk, in which case ordinary equity capital should be used instead of debt funds. Managements who want to take more risk can use the credit more and more.

11. Trading on equity:- Financial leverage or trading on equity is the use of fixed-cost means of finance, such as debt and preference equity capital, to finance the assets of the company. Equity). If the return on assets received from debt funds is more than the cost of the loan, it will lead to an increase in the earnings per share. Earnings per share will also increase with the use of preference share capital but will increase more with the use of loans because interest can be deducted from taxable income. Financial leverage is an important element of capital structure planning because of its effect on earnings per share. The higher the earnings per share, the higher the value of the company's equity shares. To determine the effect of leverage, management should analyze the relationship between earnings per share (EPS) and earnings before interest and tax (EBIT) under alternative means of finance. If the level of income before interest and tax is increasing, then the income per share will increase due to more use of debt. Therefore, the management of the company should choose such option of means of finance on which the income per share is maximum. 12. Cash flow ability of the company:- Sometimes the company has high interest cover ratio but does not have enough cash to pay interest, preference dividend and debt. This may put the company in a state of financial insolvency. Therefore, the company must have enough cash during the year so that the fixed charges can be paid on time. The amount of fixed encumbrance will be higher if the company uses more debt and preference share capital in its capital structure. The higher the company's cash flow capacity, the greater will be its ability to utilize debt. Therefore, when the company management considers to use additional debt, it should analyze the cash generating capacity of the company to pay the fixed burden. Companies that see the potential for higher and more stable cash flows in the future can use more of debt in their capital structure. The ability of a company to generate cash flows and pay fixed charges can be ascertained by finding the ratio of net cash inflows to fixed charges. The higher this ratio, the higher will be the debt capacity of the company.

13. COST OF CAPITAL:- The cost of a source of finance is the minimum return required by its suppliers. The expected return depends on the degree of risk borne by the investors. Ordinary shareholders bear maximum risk as the rate of dividend is not fixed for them and dividend is paid after paying interest and preference dividend. It is the statutory obligation of the company to pay interest on loans whether the company is profitable or not. Therefore, debt is a cheaper means of finance than ordinary share capital. The cost of the loan is further reduced as the interest is deducted from the income to calculate income tax. It should not be forgotten here that the company cannot continuously reduce the collective cost of capital by the use of debt, only to an extent that debt can be a cheaper means of finance. Debt beyond this limit can prove to be a costly instrument as the use of excessive debt increases the risk to the creditors and shareholders. The creditors are not ready to extend the loan to the company when the degree of risk increases and if they do, they ask for a higher rate of interest than before. Similarly, due to excessive use of debt, common shareholders also expect higher rate of dividend, which increases the cost of ordinary share capital. All this reduces the market value of the ordinary share. If the cost of share capital and retained earnings are compared, the cost of retained earnings will be less because one is not issuing expenses and secondly, retained earnings do not have to pay personal income tax to the shareholders which otherwise would have to be paid on dividends. 14. Flotation costs:- These costs are incurred at the time of issue of securities. These include the commission of underwriters, brokerage, stationery expenses and other expenses. Usually the cost of taking the loan is less than the cost of issue of shares. This may attract the company towards credit instruments. In case of retained earnings, issue expenses do not have to be incurred. But the issue cost is not an important factor in the decision on capital structure. If the amount of issue amount is increased, the percentage of issue cost can be reduced.

CAPITAL STRUCTURE THEORIES The principles of capital structure express the relationship between capital structure, cost of capital and the value of the firm. The capital structure of the firm should be such that the value of the firm ( wealth of the shareholders) is maximum. Such capital structure called optimum capital structure. There are various theories that explain the relationship between capital structure or financing mix (dept-equity ratio), cost of capital and valuation of the company. According to one ideology, capital structure affects a cost of capital and its value. According to another view, there is no relation between the capital structure of the company, its cost of capital and its value. There are four approaches to express the relationship between the capital structure and the value of the firm. These principles are the following : 1. Net Income Approach 2. Net Operating Income Approach 3. Modigliani-Miller Approach 4. Traditional Approach Will be described in the following pages:

NET INCOME APPROACH This principles was given by Durand. According to this theory, decisions regarding capita structure affect the value of the firm. Changes in the capital structure ( financial leverage or debt-equity ratio) lead to changes in the collective capital cost and the value of the firm. More use of debt in the structure will reduced the collective capital cost and increase the value and equity shares of the firm. On the other hand, a reduction in debit in the capital structure will increase the collective capital cost and decrease the firm’s value and market value of equity shares. In short, if the ratio of debt in the capital structure increases, the weighted average cost of capital decreases and hence the value of the firm increases. This theory is based on the following assumptions. (a) No tax (b) The cost of debt is less than the cost of equity capital. (c) The use of credit does not change the invester perception of risk. As per the net income approach, financial leverage is an important factor in the decision regarding the capital structure of the company. By judicious use of dept and equity, the company can achieve optimum capital structure. Such a capital structure is called optimum capital structure at which the cost of collective capital (ko) is minimum and the value of the firm is maximum. The market value of equity is highest on this capital structure.

NET OPERATING INCOME APPROACH This approach is also provided by durand. It is the opposite of the net income approach if there are no taxes. This approach says that the weighted average cost of capital remains constant. It believes in the fact that the market analyses a firm as a whole and discounts at a particular rate that has no relation to the debt-equity ratio. If tax information is given, it recommends that with an increase in debt financing WACC reduces and the value of the firm will start increasing. ASSUMPTIONS OF NET INCOME APPROACH The net income approach makes certain assumptions which are as follows. •The increase in debt will not affect the confidence levels of the investors. •There are only two sources of finance; debt and equity. There are no sources of finance like prefrence share capital and retained earning. •All companies have uniform dividend pay out ratio; it is 1. •There is no flotation cost, no transaction cost and corporate dividend tax. •Capital market is perfect, it means information about all companies are available to all investors and there are no chances of over pricing or under pricing of security. Further it means that all investors are rational. So, all investors want to maximize their return with minimization of risk. •All sources of finance are for infinity. There are no redeemable sources of fina

According to this approach, the firm is collectively valued by the market and does not divide the firms valued into equity value and debt value separately. The collective cost of capital (ko) remains constant at all levels of financial leverage. Equity value is the residual value, which is determined by subtracting the value of debt (b) from the total value (v) of the firm. Thus, Total Value of Equity (S) = V-B when the company increase the ratio of dept to capital structure, it increases the financial risk for equity shareholders. As a result of increased financial risk, equity shareholders expect a higher rate of return from the company to compensate for the higher risk. This means that it increases the cost of equity capital (k). Thus the benefit of using cheap credit is eliminated by the increase in the implicit cost of equity, resulting in the same collective cost of capital. According the theory of net operating income, the optimum capital structure is nothing because the firms net worth and the market value of the shares are not affected by the amount of financial.

TRADITIONAL APPROACH This approach does not define hard and fast facts. It says that the cost of capital is a function of the capital structure. The special thing about this approach is that it believes in an optimal capital structure. Optimal capital structure implies that at a particular ratio of debt and equity, the cost of capital is minimum and the value of the firm is maximum. The net income (NI) theory and the net operating income (NO1) theory are the two extremes of the relationship between the capital structure and the value of the firm. Whereas the net income theory states that the capital structure affects the collective capital cost and the total value of the firm, the net operating income theory suggests that the capital structure is completely irrelevant. The MM theory supports the net operating income approach. But due to the assumptions of MM theory, it does not appear to be fully applicable in actual practice. Conventional theory approaches the compromise or middle between net income theory and net operating income theory. In part it has the merits of both theories. Therefore, it is a middle principle. The traditional approach is similar to the net income theory when it states that leverage affects the collective capital cost and the total value of the firm, but it does not accept the view of the net income theory that the value of the firm changes over all amounts of financial leverage. Will necessarily increase. This is similar to the net operating income approach in that after a certain amount of leverage the collective capital cost increases, resulting in a decrease in the total value of the firm, but it differs from the net operating income theory because it does not adopt the idea. Assumes that the collective capital cost remains constant at all levels of leverage.

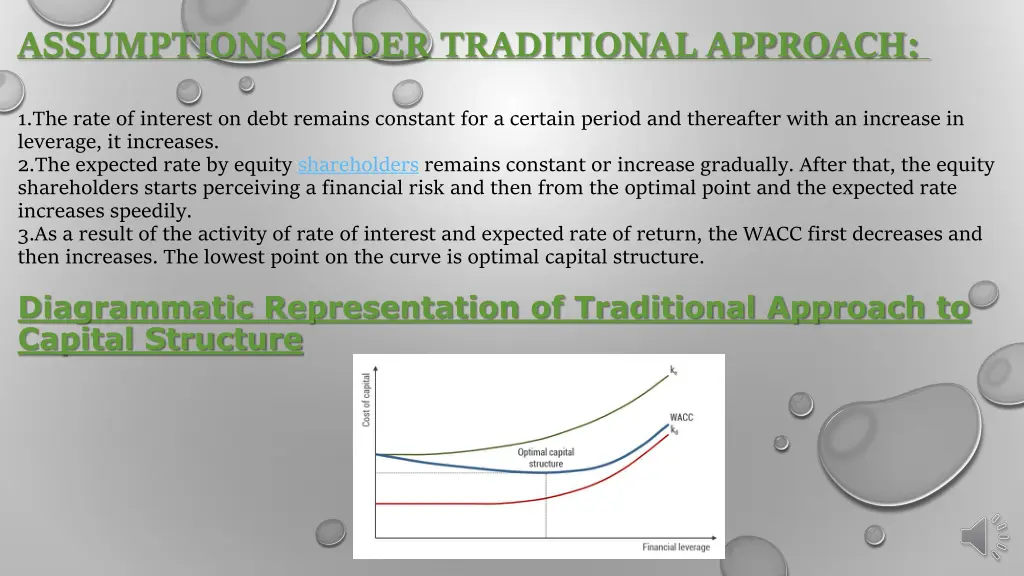

ASSUMPTIONS UNDER TRADITIONAL APPROACH: 1.The rate of interest on debt remains constant for a certain period and thereafter with an increase in leverage, it increases. 2.The expected rate by equity shareholders remains constant or increase gradually. After that, the equity shareholders starts perceiving a financial risk and then from the optimal point and the expected rate increases speedily. 3.As a result of the activity of rate of interest and expected rate of return, the WACC first decreases and then increases. The lowest point on the curve is optimal capital structure. Diagrammatic Representation of Traditional Approach to Capital Structure

MODIGLIANI AND MILLER APPROACH This approach was devised by modigliani and miller during the 1950s. The fundamentals of the modigliani and miller approach resemble that of the net operating income approach. Modigliani and miller advocate capital structure irrelevancy theory, which suggests that the valuation of a firm is irrelevant to the capital structure of a company. Whether a firm is high on leverage or has a lower debt component in the financing mix has no bearing on the value of a firm. The modigliani and miller approach further state that the operating income affects the market value of the firm, apart from the risk involved in the investment. The theory stated that the value of the firm is not dependent on the choice of capital structure or financing decisions of the firm.

ASSUMPTIONS OF MODIGLIANI AND MILLER APPROACH 1. There are no taxes. 2. Transaction cost for buying and selling securities, as well as the bankruptcy cost, is nil. 3. There is a symmetry of information. This means that an investor will have access to the same information that a corporation would and investors will thus behave rationally. 4. The cost of borrowing is the same for investors and companies. 5. There is no floatation cost, such as an underwriting commission, payment to merchant bankers, advertisement expenses, etc. 6. There is no corporate dividend tax. The modigliani and miller approach indicates that the value of a leveraged firm (a firm that has a mix of debt and equity) is the same as the value of an unleveraged firm (a firm that is wholly financed by equity). If the operating profits and future prospects are the same. That is, if an investor purchases shares of a leveraged firm, it would cost him the same as buying the shares of an unleveraged firm.

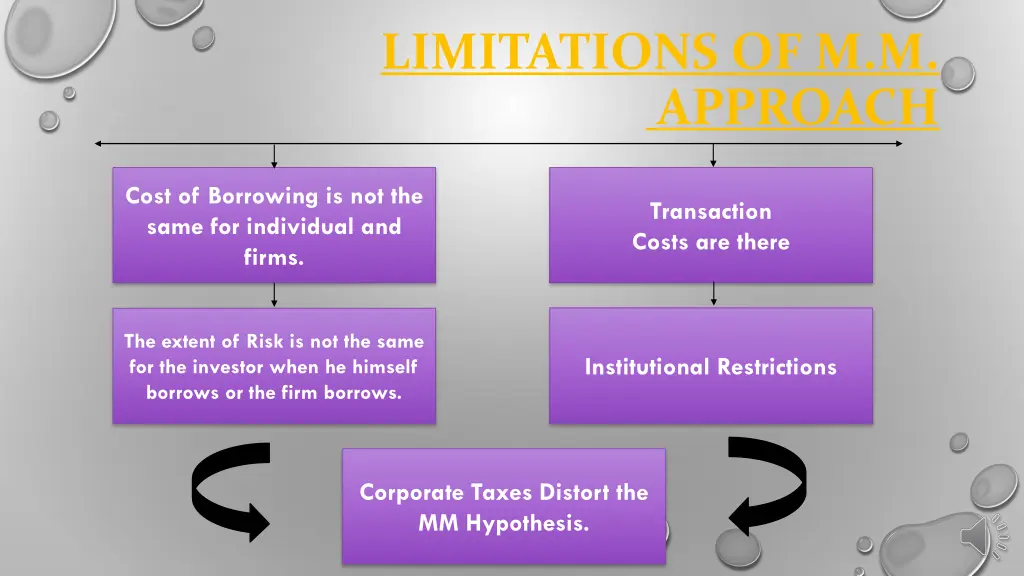

LIMITATIONS OF M.M. APPROACH Cost of Borrowing is not the same for individual and firms. Transaction Costs are there The extent of Risk is not the same for the investor when he himself borrows or the firm borrows. Institutional Restrictions Corporate Taxes Distort the MM Hypothesis.