Download

1 / 30

300 likes | 511 Views

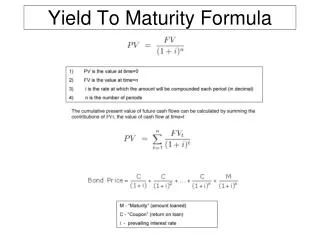

UNDERSTANDING THE INTEREST RATES. Yield to Maturity. Frederick University 2014. Yield to Maturity. The yield to maturity is the interest rate that makes the discounted value of the future payments from a debt instrument equal to its current value (market price) today.

E N D

UNDERSTANDING THE INTEREST RATES. Yield to Maturity Frederick University 2014

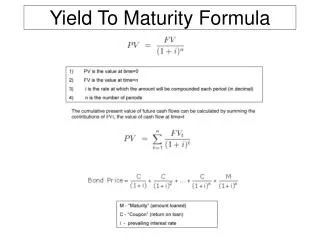

Yield to Maturity The yield to maturity is the interest rate that makes the discounted value of the future payments from a debt instrument equal to its current value (market price) today. It is the yield bondholders receive if they hold a bond to its maturity.

Bonds: 4 types • Discount bonds - zero coupon bonds (government bonds) • fixed payment loans (mortgages, car loans) • coupon bonds (government bonds, corporate bonds) • consols

Zero coupon bonds Discount bonds • Purchased price less than face value • P < F • No interest payments • Face value on maturity

example • 90 day bond, • P = € 9850, F = € 10,000 • YTM solves

F - P 360 idb = x F d yield on a discount basis • how the bond yields are actually quoted • approximates the YTM

example • 90 day bond, • P = € 9850, F = € 10,000 • discount yield =

The discount yield vs. the yield to maturity • idb < YTM why? • F in denominator • 360 day year

fixed payment loan • loan is repaid with equal (monthly) payments • Each payment is a combination of principal and interest

fixed payment loan • € 15,000 car loan, 5 years • monthly payments = € 300 • € 15,000 is price today • cash flow is 60 pmts. of € 300 • what is i?

i is annual rate • but payments are monthly, & compound monthly • i = i/12

how to solve for i? • Trial and error • Financial tables • Financial calculator • Spreadsheets

Coupon bond • a 2-year coupon bond • a face value F = €10,000, • a coupon rate i = 6%, • a price P =€9750. • bond price = PV(future bond payments) • The coupon payments are [face value x coupon rate]/2 = = €10,000 x 0.06 x 0.5 = €300.

payments are every 6 months for 2 years, • there are a total of 2 x 2 = 4 payment periods. • the yield to maturity, i, is expressed on an annual basis, so i/2 represents the 6 month discount rate • 9750 = 300/(1 + i/2) + 300/(1 + i/2)2 + 300/(1 + i/2)3 + 300/(1 + + i/2)4 + 10000/ ( 1 + i/2)4 • or: • 9750 = 300/(1 + i/2) + 300/(1 + i/2)2 + 300/(1 + i/2)3 + 10 300/(1 + i/2)4 • i =7.37%

3 important points • The yield to maturity equals the coupon rate ONLY when the bond price equals the face value of the bond. • When the bond price is less than the face value (the bond sells at a discount), the yield to maturity is greater than the coupon rate. When the bond price is greater than the face value (the bond sells at a premium), the yield to maturity is less than the coupon rate. • The yield to maturity is inversely related to the bond price. Bond prices and market interest rates move in opposite directions.

Consols (or perpetuities) Consols (or perpetuities) promise interest payments forever, but never repay principal.

Bond Yields • Yield to maturity (YTM) • Current yield • Holding period return

Yield to Maturity (YTM) • a measure of interest rate • interest rate where P = PV of cash flows

Current yield • approximation of YTM for coupon bonds annual coupon payment ic = bond price

Current yield vs. YTM Better approximation when: • Maturity is shorter • P is closer to F

example • 2 year bonds, F = € 10,000 • P = € 9750, coupon rate = 6% • current yield 600 ic = = 6.15% 9750

current yield = 6.15% • true YTM = 7.37% • lousy approximation • only 2 years to maturity • selling 2.5% below F

Holding period return • Holding period return – the return for holding a bond between periods t and t+1 • sell bond before maturity • return depends on • holding period • interest payments • resale price

Holding period return • C/Pt is the current yield ic • (Pt+1 – Pt)/Pt is the capital gain = g • RET = ic+ g

example • 2 year bonds, F = € 10,000 • P = € 9750, coupon rate = 6% • sell right after 1 year for € 9900 • € 300 at 6 mos. • € 300 at 1 yr. • € 9900 at 1 yr.

i/2 = 3.83% i = 7.66%

why i/2? • interest compounds annually not semiannually