Download

1 / 17

170 likes | 405 Views

TABLE 6.1. WHAT MAKES A PROFESSION. TABLE 6.2. FEATURES, DUTIES, RIGHTS, AND VALUES OF THE ACCOUNTING PROFESSION. TABLE 6.3. MOTIVES INFLUENCING PEOPLE AT KOHLBERG’S SIX STAGES OF MORAL REASONING. TABLE 6.4. NATIONAL AND INTERNATIONAL ACCOUNTING ORGANIZATIONS OPERATING IN NORTH AMERICA.

E N D

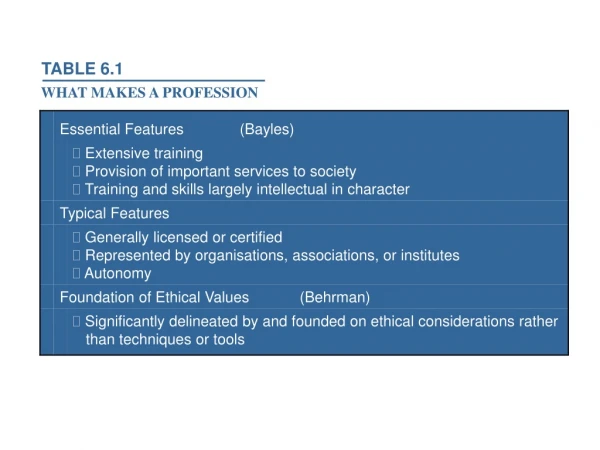

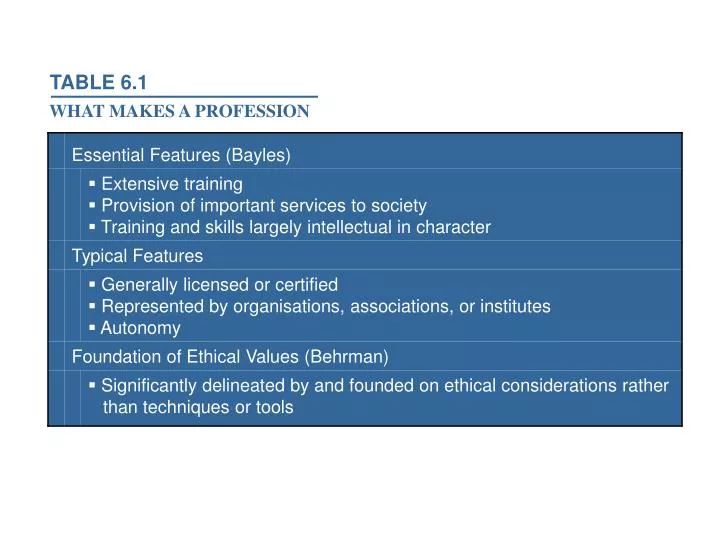

TABLE 6.1 WHAT MAKES A PROFESSION

TABLE 6.2 FEATURES, DUTIES, RIGHTS, AND VALUES OF THE ACCOUNTING PROFESSION

TABLE 6.3 MOTIVES INFLUENCING PEOPLE AT KOHLBERG’S SIX STAGES OF MORAL REASONING

TABLE 6.4 NATIONAL AND INTERNATIONAL ACCOUNTINGORGANIZATIONS OPERATING IN NORTH AMERICA

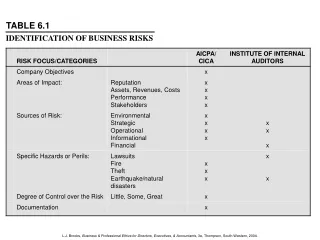

TABLE 6.5 CONTRIBUTIONS TO THE NORTH AMERICAN REGULATORY FRAMEWORK FOR PROFESSIONAL ACCOUNTANTS

TABLE 6.6 TYPICAL FRAMEWORK FOR A CODE OF CONDUCTFOR PROFESSIONAL ACCOUNTANTS

TABLE 6.7 FUNDAMENTAL PRINCIPLES IN CODES OF CONDUCTFOR PROFESSIONAL ACCOUNTANTS

TABLE 6.8 IFAC 2005 CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTSFUNDAMENTAL PRINCIPLES – SECTION 100.4

TABLE 6.9 POSSIBLE SANCTIONS FOR UNETHICAL BEHAVIOR UNDER PROFESSIONAL ACCOUNTING CODES OF CONDUCT AND REGULATORY AUTHORITIES

TABLE 6.10 THE MACDONALD COMMISSION: OVERVIEW OF PRINCIPAL RECOMMENDATIONS

TABLE 6.11 IFAC 2005 CODE OF ETHICS FOR PROFESSIONAL ACCOUNTANTSFRAMEWORK—CONTENTS • Page • PREFACE..................................................................................................................................... 2 • PART A: GENERAL APPLICATION OF THE CODE • 100 Introduction and Fundamental Principles ................................................................. 4 • 110 Integrity ...................................................................................................................... 9 • 120 Objectivity ................................................................................................................... 10 • 130 Professional Competence and Due Care.................................................................. 11 • 140 Confidentiality ............................................................................................................ 12 • 150 Professional Behavior ................................................................................................ 14 • PART B: PROFESSIONAL ACCOUNTANTS IN PUBLIC PRACTICE • 200 Introduction.................................................................................................................. 16 • 210 Professional Appointment........................................................................................... 21 • 220 Conflicts of Interest ..................................................................................................... 24 • 230 Second Opinions ......................................................................................................... 26 • 240 Fees and Other Types of Remuneration..................................................................... 27 • 250 Marketing Professional Services................................................................................. 29 • 260 Gifts and Hospitality .................................................................................................... 30 • 270 Custody of Clients Assets .......................................................................................... 31 • 280 Objectivity—All Services.............................................................................................. 32 • 290 Independence—Assurance Engagements .................................................................. 33 • PART C: PROFESSIONAL ACCOUNTANTS IN BUSINESS • 300 Introduction................................................................................................................... 79 • 310 Potential Conflicts........................................................................................................ 83 • 320 Preparation and Reporting of Information .................................................................. 85 • 330 Acting with Sufficient Expertise................................................................................... 86 • 340 Financial Interests ...................................................................................................... 87 • 350 Inducements ............................................................................................................... 89 • DEFINITIONS............................................................................................................................... 91 • EFFECTIVE DATE....................................................................................................................... 95

FIGURE 6.1 IFAC 2005 CODE OF ETHICS FRAMEWORK Duty to Society, Serve the Public Interest (S 100.1) • Compliance with Fundamental Principles • Integrity, Objectivity • Professional Competence & Due Care • Confidentiality, Professional Behavior (S 100.4) Threats to Compliance with Fundamental Principles Identify, Evaluate, Eliminate or Reduce Threats to Acceptable Levels by Applying Safeguards And Resolving any Conflicts in Application Threats (S 100.10)Safeguards(S 100.11 & 12) Self-Interest, Self-review Professional Codes, Training or Standards Advocacy, Familiarity, Intimidation Legislation, Regulation, In client, firm or business (S 100.5) (S 100.16) Source: IFAC Code of Ethics for Professional Accountants, June 2005 (Section number).

TABLE 6.12 THREATS TO NONCOMPLIANCE – INDEPENDENT JUDGEMENT

TABLE 6.13 SAFEGUARDS REDUCING THE RISK OF CONFLICT OF INTEREST SITUATIONS

FIGURE 6.2 IFAC CODE’S FRAMEWORK FOR INDEPENDENT JUDGMENT Protect the Public Interest Professional Service to Clients Independence of Mind and Appearance (S 290.8) Independent Judgment Integrity Objectivity Professional Skepticism Source: IFAC Code of Ethics for Professional Accountants, 2005, S 290.8 & Independence Definition

TABLE 6.14 CONFLICTS OF INTEREST FOR PROFESSIONAL ACCOUNTANTS: CATEGORIES, SPHERES OF ACTIVITY AFFECTED, AND EXAMPLES

FIGURE 4.1 IFAC 2001 CODE OF ETHICS VALUES FRAMEWORK Duty to Society, Serve the Public Interest Objectives Meet Expectations for Professionalism, Performance, Public Interest Basic Needs Credibility, Professionalism, Highest Quality Services, Confidence • Fundamental Principles • Integrity, Objectivity, Professional Competence, Due Care, • Skepticism, Confidentiality, Professional Behavior, Technical Standards Source: IFAC, November, 2001.