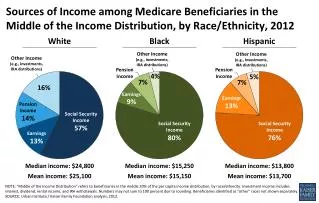

Income Security Programs

SOCIAL DEVELOPMENT CANADA. Income Security Programs. SOCIAL DEVELOPMENT CANADA. Income Security Programs. Old Age Security (OAS) Canada Pension Plan (CPP) International Social Security Agreements 1 800 277-9914 www.sdc-dsc.gc.ca/isp. Canada's Retirement Income System.

Income Security Programs

E N D

Presentation Transcript

SOCIAL DEVELOPMENT CANADA Income Security Programs

SOCIAL DEVELOPMENT CANADA Income Security Programs • Old Age Security (OAS) • Canada Pension Plan (CPP) • International SocialSecurity Agreements • 1 800 277-9914 • www.sdc-dsc.gc.ca/isp

Canada's Retirement Income System

The 3 levels of Canada’s Retirement Income System 3Private SavingsEmployer Pensions 2 Canada Pension Plan Québec Pension Plan 1 Old Age Security

Canada’s Retirement Income System • In general, 70% of pre-retirement income is required • OAS and CPP retirement pensions are designed to replace about 40% of thepre-retirement income

Canada’s Retirement Income System • On average, 70% of pre-retirement income is required to maintain pre- retirement lifestyle • The OAS pension and CPP Retirement pension are designed to replace about 40% of the average pre-retirement income • Maximum OAS and CPP retirement benefits in year 2006 is about $16,000

Old Age Security Sustainability • Financed from general tax revenues of the Government of Canada • OAS on solid ground - Actuarial studies • Canada’s Gross Domestic Product (GDP) and individual incomes to rise

Old Age Security Benefits • Old Age Security pension (OAS) • Guaranteed Income Supplement (GIS) • Allowance • Allowance for the Survivor

Old Age Security (OAS) Pension • Based on age, legal status, and years of residence in Canada • 2 types of pension - Full and Partial • Taxable • May be subject to OAS Repayment of Benefits

OAS Pension Must: • be 65 years ofage or more; • meet the legalstatus andresidencerequirements; • apply in writing

OAS PensionLegal Status Requirement Must be: • a Canadian citizen; or • a legal resident of Canada; on the day preceding the approval of your application or on the day before the day you stopped living in Canada.

OAS Residency Requirement People living inCanada • Must be a Canadian citizen or a legal resident at the time your application is approved • Must have resided in Canada for at least 10 years after the age of 18

OAS Residency Requirements People living outside of Canada • Must have been a Canadian citizen or a legal resident of Canada when you left Canada • Must have resided in Canada for at least 20 years after the age of 18

Full OAS Pension Must: • have resided in Canada for at least40 years after age 18 and before your application is approved; or • meet the 10 years residence rule; or • meet the “3 for 1” residence rule.

Full OAS Pension“3 for 1” Residence Rule Example: 18 55 65 64 Need 3 years ofresidence For each year ofabsence

Partial OAS Pension • You do not qualify for a full OAS pension • 1/40th of a full OAS pension for each full year of residence in Canada after age 18 • Minimum of 10 years residence required • Once approved, a partial OAS pension will not be increased following additional years of residence in Canada

Portability To have the OAS pension paid outside Canada, you must: • have 20 years of residence in Canada after age 18; or • meet the 20-yearresidence throughone of Canada’sInternationalAgreements withanother country.

OAS Repayment of Benefits • OAS pension higher-income pensioners • Net World Income from $62,144 to $100,914 (2006) • 15% for residents, varies for non-residents • Based on previous year’s income (continued…)

Guaranteed Income Supplement (GIS) • For low-income seniors • Added to the OAS pension • Based on income and marital status • Based on combined income, if the applicant has a spouse/partner • Not taxable

GIS Must: • be in receipt of an OAS pension; • reside in Canada; • apply in writing.

Allowance • For low-income seniors who meet the eligibility conditions • Based on combined income from the previous year • Not taxable • Must apply in writing

Allowance Must be: • between the ages of 60 and 64; • the spouse/common-law partner of a GIS recipient; • a Canadian citizenor a legal resident(same as OAS); • a resident of Canadafor at least 10 yearsafter age 18

Allowance for the Survivor • For low-income seniors who meet the eligibility conditions • Based on previous year’s income • Not taxable • Must apply in writing

Allowance for the Survivor Must be: • between the ages of 60and 64; • a survivor; • a Canadian citizen or legal resident (same as OAS); • a resident of Canada for at least 10 years after age 18.

Allowance and Allowance for the Survivor at age 65: • At age 65, the Allowance and Allowance for the Survivor stops,must apply for OAS Pension • May also qualify for the GIS

Maximum Net Income Allowed Jan to March 2006 GIS – Single $ 14,256 Table 1 GIS Married - Spouse/Partner is: • an OAS pensioner (65+)$ 18,720 Table 2 • a Non-pensioner (under 60)$ 34,368 Table 3 • an Allowance pensioner (60-64) $ 34,368 Table 4 Allowance $ 26,496 Table 4 Allowance for the Survivor $ 19,368 Table 5 (widow/widower 60-64) NOT INCLUDING OLD AGE SECURITY!

Portability • GIS, Allowance andAllowance for theSurvivor may only be paid outside of Canada for the month of your departure and for the following six months

Renewal • GIS, Allowance and Allowance for the Survivor must be renewed each year • They are renewed automatically if you file your income tax return prior toApril 30 (continued…)

Canada Pension Plan • Began in January 1966 • Employment-based contributions • Self-supporting • Payable outside Canada • Reviewed and revised regularly • Québec has a program with similar benefits

CPP Investment Board • Professionally manages the CPP fund,not needed to pay benefits • Broadly subject to the same investment rules as other pension funds • Reports its investments and returns regularly www.cppib.ca

Contributions for Year 2006 Maximum Contributory Earnings: $42,100 (YMPE) - $3,500 (YBE) = $38,600 Employee Rate: 4.95% Amount: $1,831.50 Employer Rate: 4.95% Amount: $1,831.50 Self-Employed Rate: 9.9% Amount: $3,663

Contribution Rates Schedule Year Employee Employer Self-Employed 2000 3.9% 3.9% 7.8% 2001 4.3% 4.3% 8.6% 2002 4.7% 4.7% 9.4% • 4.95% 4.95% 9.9% 2006 4.95% 4.95% 9.9% (Contribution Rate will now be maintained at this maximum rate of 9.9%)

Adjusted Earnings • Protects pension by taking growth of wages into account

Contributory Period Starts (later of): • January 1966; or • month after your 18th birthday.

Contributory Period Ends (first of): • month before your Retirement pension starts; or • month you reach age 70; or • month you die; or • when eligible for Disability benefits.

Contributory Period Example • Ends (first of): • retirement; or • age 70; or • death • Starts (later of): • January 1966; or • age 18 Age 60 Age 65 Age 70 Start (Flexible start date option)

Canada Pension Plan Statement of Contributions • Sent periodically • 1 877 454-4051

Drop-Out Provisions • Periods of CPP Disability • Periods during which children were raisedup to age 7 • Plus 65 years of age • 15% of the lowest earning years in your contributory period(calculated last on remaining years)

Drop-Out ProvisionsExample: Year 2005Age 65 1968 - 1974 1982-1983 1977 - 1978 1985 - 1990 Contributory Period40 Years23 years after drop-outs (approximate only as calculation actually uses months) 1. Periods of disability (1985 to 1990) 6 Years 2. Raising children (1968 to 1974) 7 Years 3. 15% (39 - 13 = 26 years x 15%) 4 Years

Child Rearing Drop-Out Must have: • a child born after December 31, 1958; • left or reduced work to care for the child while under the age of 7; • received the FamilyAllowances; or • been eligible for theChild Tax Benefit. Must apply in writing

Credit Splitting • “Credits” may be divided upon divorce, legal annulment or separation of spouses or common-law partners • “Credits” may create eligibility or increase/ decrease entitlement toCPP benefits • Applicant’s ex-spouse/ex-partner is notified ofthe request in writing

Canada Pension Plan Benefits • Retirement pension • Disability benefit • Disabled Contributor Child’s benefit • Survivor benefits • Death benefit • Survivor’s benefit • Surviving Child’s benefit

Retirement Pension May start receiving theRetirement pension: between age 60 and 65; at age 65; between age 65 and 70. • Must have made at least one valid contribution • Must apply in writing • Taxable

Flexible Retirement Pension Between 60 and 65: • Amount decreased by 0.5% for each month under age 65 • Maximum decrease of 30% • No re-adjustment of pension amount at age 65 (continued…)

Flexible Retirement Pension Between 60 and 65 • No retroactivity • Stop or earn up to a maximum amount for period of time • Stops contributing to CPP/QPP

Substantially Ceased WorkingCessation Test For Early Retirement • Earnings from employment must be below the maximum monthly CPP Retirement pension • Only for the month before the Retirement pension starts and for the month the pension starts being paid • Max. of $844.58 for each month (2006)

Flexible Retirement Pension Between 65 and 70 • Increased by 0.5% for each month over age 65 • Maximum increase of 30% • Retroactivity of maximum of 11 months prior to application (back to age 65 only) • Cannot contribute after age 70

Sharing Your Retirement Pension Sharing your Retirement pension withyour spouse or common-law partner.