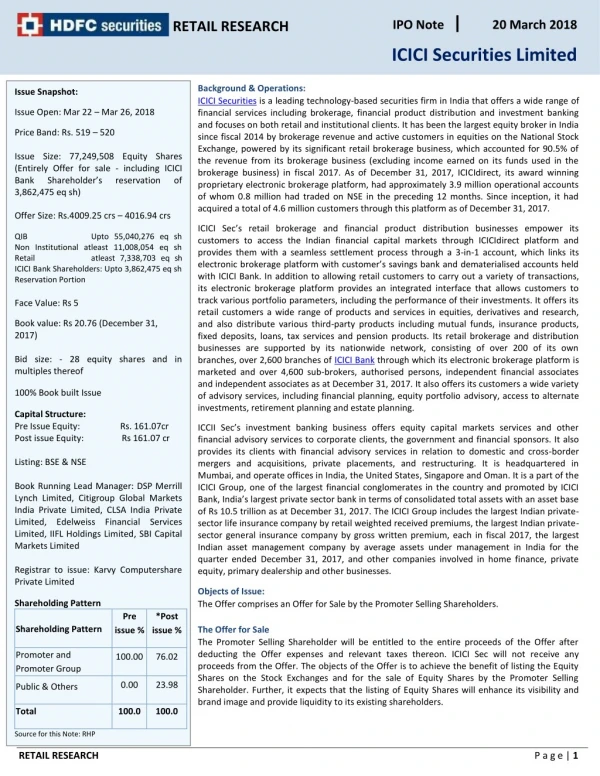

Download

1 / 23

E N D

Sale of Securities On April 1, 2006, the investment in Silmaril’s debt securities is sold for $103,000, which includes accrued interest of $2,500. On January 1, the debt securities had a carrying value of $105,240, therefore interest revenue of $2,105 ($105,240 x .08 x 3/12) would be recorded The required amortization for the three-months’ premium between January 1 and April 1 would be $395.

Sale of Debt Securities Entry to record accrued revenue and to amortize premium: Apr. 1 Interest Receivable 2,500 Investment in Held-to Maturity Securities 395 Interest Revenue 2,105 Entry to record sale: Apr. 1 Cash 103,000 Realized Loss on Sale of Securities 4,345 Interest Receivable 2,500 Investment in Held-to Maturity Securities 104,845

Sale of Equity Securities Jan. 1, 2003 Investment in Trading Securities 10,000 Cash 10,000 Dec 31, 2003 Market Adjustment – Trading 2,000 Unrealized gain - Trading 2,000 Dec 31, 2004 Unrealized loss – Trading 2,000 Market Adjustment – Trading 2,000 Dec 31, 2004 Cash 9,000 Realized loss – Trading 1,000 Investment in Trading Securities 10,000

Transferring SecuritiesBetween Categories Treatment of Change in Value Transferred From trading Any unrealized change in value not previously recognized will be recognized in net income in the current period. To trading Any unrealized change in value not previously recognized will be recognized in net income in the current period. Recognize any unrealized change in value in a stockholders’ equity account. From held to maturity to available for sale Continued

Transferring SecuritiesBetween Categories Treatment of Change in Value Transferred From available for sale to held to maturity Any unrealized change in value recorded in a stockholders’ equity account is to be amortized over the security’s remaining life using the effective-interest method. Statement of Financial Standards No. 115, par. 15d

Transfer from the trading to available-for-sale category Assume: Cost of trading security $3,000 Fair market value, end of 2006 3,600 Fair market value at transfer date (in 2007) 3,800 Continued

Transfer from the trading to available-for-sale category Investment in Available-for-Sale Securities 3,800 Market Adjustment--Trading Securities 600 Unrealized Gain on Transfer of Securities 200 Investment in Trading Securities 3,000

Transfer from the available-for-sale category to the trading security category • Assume: • Cost of available-for-sale security $12,000 • Fair market value, end of 2006 10,700 Continued

Transfer from the available-for-sale category to the trading security category Investment in Trading Securities 10,300 Market Adjustment--Trading Securities 1,300 Unrealized Loss on Transfer of Securities 1,700 Unrealized Increase/Decrease in Value of Available-for- Sale Securities 1,300 Investment in Available-for- Sale Securities 12,000

Transfer from held-to-maturity to the available-for-sale category. Assume: Cost of held-to-maturity security 20,000 Fair market value, Dec. 31, 2006 20,700 Continued

Transfer from held-to-maturity to the available-for-sale category. Investment in Available-for- Sale Securities 20,400 Unrealized Increase/ Decrease in Value of Available-for-Sale Securities 400 Investment in Held-to- Maturity Securities 20,000

Transfer from available-for-sale to held-to-maturity. Assume: Cost of available-for-sale securities $5,000 Fair market value, end of 2006 6,500 Fair market value at transfer date 5,900 Continued

Transfer from available-for-sale to held-to-maturity. Investment in Held-to-Maturity Securities 5,900 Unrealized Increase/Decrease in Value of Available-for-Sale Securities 600 Investment in Available-for- Sale Securities 5,000 Market Adjustment— Available-for-Sale Securities 1,500

Investment securities and the cash flow statement The purchase and sale of available-for-sale, held-to-maturity, and equity method securities are reported in the Investing Activities section of the statement of cash flows. In contrast, the cash flows associated with the purchase and sale of trading securities are shown in the Operating Activities section. This difference stems from the fact that, by definition, a company that maintains a trading securities portfolio considers as part of its normal business operations the attempt to make money through the correct timing of purchases and sales of (trading) securities.

Cash Flows from Gains and Losses on Available-for-Sale Cash Company began with a $1,000 investment on January 1, 2005. Cash sales $1,700 Cash expenses (1,400) Purchases of investment securities (600) Sale of investment securities (costing $200) 170 Continued

Cash Flows from Gains and Losses on Available-for-Sale Sales $1,700 Expenses (1,400 ) Operating income $ 300 Realized loss on sale of securities (30 ) Net income $ 270 The market value of the remaining securities was $500 on December 31, 2005. Continued

Cash Flows from Gains and Losses on Available-for-Sale This $100 unrealized increase is reported as an increase in Accumulated Other Comprehensive Income. Cash Company will report a $100 unrealized increase in the value of it available-for-sale portfolio. However, if it were a Trading security, Cash Company would report the $100 unrealized increase in the income statement

Cash Flows from Gains and Losses on Available-for-Sale Operating activities: Net income $ 270 Plus realized loss on sale of securities 30 $ 300 Investing activities: Purchase of investment securities $(600) Sale of investment securities 170 (430) Financing activities: Initial investment by owner 1,000 Net increase in cash $ 870 The statement of cash flows for Caesh Company for 2005 appear as follows:

Classification and Disclosure • Trading securities • The change in net unrealized holding gain or loss that is included in the income statement. • Available-for-sale securities • Aggregate fair value, gross unrealized holding gains and gross unrealized holding losses, and amortized cost basis by major security type. • The proceeds from sales of available-for-sale securities and the gross realized gains and losses on those sales and the basis on which cost was determined in computing realized gains and losses.

Classification and Disclosure • Available-for-sale securities (continued): • The change in net unrealized holding gain or loss on available-for-sale securities that has been included in stockholders’ equity during the period. • Held-to-maturity securities: • Aggregate fair value, gross unrealized holding gains and gross unrealized holding losses, and amortized cost basis by major security type. • The company should disclose information about contractual maturities. Continued

Classification and Disclosure • Transfers of securities between categories: • Gross gains and losses included in earnings from transfers of securities from available-for-sale into the trading category. • For securities transferred from held-to-maturity, the company should disclose the amortized cost amount transferred, the related realized or unrealized gain or loss, and the reason for transferring the securities.

chapter14 The End