Download

1 / 25

250 likes | 606 Views

Commercial Mortgages, CMBS, ABS, CDO. Commercial Mortgages & MBS – Ch14 ABS -- Ch15 Collateralized debt obligations – Ch16. Commercial Mortgages. A commercial mortgage loan is originated to finance a commercial purchase or to refinance a prior mortgage obligation.

E N D

Commercial Mortgages, CMBS, ABS, CDO • Commercial Mortgages & MBS – Ch14 • ABS -- Ch15 • Collateralized debt obligations – Ch16 Ch14-15

Commercial Mortgages • A commercial mortgage loan is originated to finance a commercial purchase or to refinance a prior mortgage obligation. • Commercial mortgage loans are for income-generating properties, including • Multifamily properties (apartment buildings) • Office building • Industrial properties • Shopping centers • Hotel • Health care facilities Ch14-15

Characteristics of C. Mortgages • Commercial mortgage loans are non-recourse loans – lenders can only look to the income-producing property backing the loan for interest and principal repayments. Ch14-15

Performance Indictors • Debt-to-service coverage ratio (DSC) • The ratio of property’s net operating income (NOI) divided by the debt service • NOI = rental income – cash operating expenses • Critical value is 1 • Loan-to-value ratio • Value is the present value of the expected cash flow, different from market value or appraised value for residential mortgage • Valuation requires projecting an asset’s cash flow (NOI) and discounting at an appropriate interest rate (capitalization rate) Ch14-15

Call Protection • Prepayment lockout (2-10 years) • Defeasance • The borrower provides sufficient funds for the servicer in a portfolio of treasury securities that replicates the cash flows that • Prepayment Penalty Points (5-4-3-2-1) • Yield Maintenance Charge • A yield to make the lender indifferent as to the timing of prepayments. The charge is based on the difference between the mortgage coupon and the prevailing Treasury rate. Ch14-15

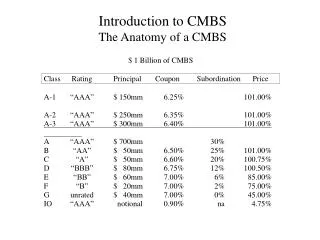

CMBS • A commercial mortgage-backed security is a security backed by one or more commercial mortgage loans. It can be issued by agency or none agency backed. • Ginnie Mae-issued securities are backed by FHA, called project loans • The purpose is to provide funding for commercial mortgages • Single borrower/multi-property deals and multi-borrower deals Ch14-15

CMBS vs RMBS • Much lower prepayment risk for CMBS • Lower probability of default for CMBS – the loan can be transferred by the servicer to a special servicer when the borrower is in default, imminent default, or in violation of covenant, who has the responsibility to modify the loan terms in case of an imminent default to reduce the likelihood of default. • Servicer: collecting monthly loan payments, keeping records related payments, maintaining property escrow for taxes and insurance … • Special servicer: duties arise when a loan becomes more than 60 days past due • See page 324 • Investors of CMBS typically are knowledgeable real estate investors and they have reviewed the proposed pool of mortgages when the structure is being created. Ch14-15

Asset-backed Securities Definition: A security created by pooling loans other than residential prime mortgage loans and commercial mortgage loans is referred to as an asset-backed security. Categorizing ABS: Existing asset securitizations or future flow securitizations Consumer ABS and commercial ABS Ch14-15

Creation of an ABS • 1. Granting a loan • Underwriting standards • Originator of a loan • 2. Securitization process • Special purpose vehicle (SPV): the ABS issuer • Legal implication: rating of ABS will be independent of the originator (page 356) • Conduit: the party who buys the loans and sell them to SPV. • 3. Credit enhancements • External – bond insurance (page 358) • Internal Ch14-15

Two-step Securitizations • Intermediate SPV (known as the depositor) • A wholly owned subsidiary of the originator • Purchase assets from the originator • Sell the assets to second SPV • Second SPV (known as the issuer) • Issue the ABS Ch14-15

Roles of SPV • The potential for reducing funding costs (page 334) • To diversify funding sources • To accelerate earnings for financial reporting purposes • For regulated entities, potential relief from capital requirements. Ch14-15

Credit Enhancement of ABS • External credit enhancement • Guaranty from third party like bond insurance • Internal credit enhancement • Cash flow waterfall (or simply waterfall) • -- cash flow to senior bondholders first, then to lower priority classes. Ch14-15

Collateral Type and Securitization Structure • Amortizing assets • Nonamortizing assets -- page 336 • Amortization schedule • Amortization period – page 336 Ch14-15

Credit Risks with ABS • Asset risk • Credit quality • Concentration risk • Structure risk -- make sure if the collateral’s cash flows match the payments that must be made to satisfy the issuer’s obligations. • Third-party providers • -- Page 338-339 Ch14-15

Credit Card Receivable-Backed Securities • This is an example of ABS -- Page 340. • Credit card issuers have receivables • financing charges collected, fees and principals. • IBs use the future cash flows from credit card receivables as collaterals to issue ABS or CDOs Ch14-15

Other types of ABS • Auto loan-backed securities • Prepayment is a concern • Rate reduction bonds • Backed by a special charge (tariff) included in the utility bills of utility customers. Ch14-15

Dodd-Frank Wall Street Reform and Consumer Protection Act • Securitizers retain a portion of the transaction’s credit risk • Reporting standards and disclosure for a securitization transaction • The representation and warranties required to be provided in securitization transactions and the mechanisms for enforcing them • Due diligence requirement with respect to loans underlying securitization transactions Ch14-15

Collateralized Debt Obligations • A security backed by a diversified pool of one or more of the following types of debt obligations • U.S. domestic investment-grade and high-yield corporate bonds • U.S. domestic bank loans • Emerging market bonds • Special situation loans and distressed debt • Foreign bank loans • Asset-backed securities • Residential and commercial mortgage-back securities Ch14-15

Structure of A CDO • Collateral managers • Collateral • Collateral assets • The funds to purchase collateral assets come from the issuance of debt obligations. • Structure of debt obligations • Senior tranches • Mezzanine tranches • Subordinate/equity tranches Ch14-15

Categories of CDOs • Arbitrage transactions • when the motivation of the sponsor is to earn the spread between the yield offered on the collateral and the payments made to the various tranches • Balance sheet transactions • when the motivation is to remove debt instruments (primarily loans) from its balance sheet, typically financial institutions such as banks seeking to reduce their capital requirement specified by bank regulators Ch14-15

Cash vs Synthetic Structures • Synthetic CDO structures involve the use of credit derivatives. Ch14-15

Arbitrage Transactions Create an arbitrage CDO is whether a structure can offer a competitive return for the subordinate/equity tranche as below:

Assumptions • The collateral of the CDO: • bonds that all mature in 10 years • The coupon rate for every bond is a fixed rate • The fixed rate at the time of purchase of cash bond is the 10 year treasury plus 400 basis points • To finance the senior tranche, • collateral manager enters into an interest-rate swap with another party with a notional principal of $80 million in which it agrees to do the following: • Pay a fixed rate each year equal to the 10-year Treasury rate plus 100 basis points • Receive LIBOR Ch14-15

Cash flows • Assuming the 10-year rate at the time the CDO is issued is 7%. • Interest received from collatoral: • Interest to senior tranche: • Interest to mezzanine tranche: • Interest to swap counterpart: • Interest received from swap counter part • As a result, • Total interest received: • Total interest paid: • Net interest Ch14-15

Synthetic CDOs • In a synthetic CDO, the collateral absorbs the economic risk associated with specified assets but does not have legal ownership of those assets • Requires the use of CDS Ch14-15