Download

1 / 16

170 likes | 433 Views

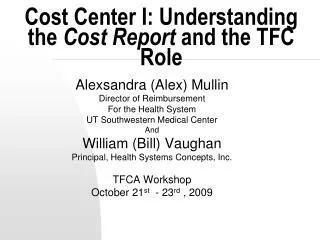

Cost Center I: Understanding the Cost Report and the TFC Role. Alexsandra (Alex) Mullin Director of Reimbursement For the Health System UT Southwestern Medical Center And William (Bill) Vaughan Principal, Health Systems Concepts, Inc. TFCA Workshop October 21 st - 23 rd , 2009.

E N D

Cost Center I: Understanding the Cost Report and the TFC Role Alexsandra (Alex) Mullin Director of Reimbursement For the Health System UT Southwestern Medical Center And William (Bill) Vaughan Principal, Health Systems Concepts, Inc. TFCA Workshop October 21st - 23rd , 2009

Why, Why, Why Must I Understand the Cost Report? • The cost report is the only mechanism to determine Medicare reimbursement for organs. • Organ acquisition is reimbursed at cost. • The managed care industry uses the data as a benchmark. • Getting it right on the cost report gives everyone useful information in transplant

Medicare Reimbursement of Transplant Services at Every Stage

What Exactly Does Medicare Pay For at Cost? • Program cost and time spent evaluating all patients referred to the center for transplant • Program cost and time listing, managing and maintaining patients on transplant waiting list • All ancillary testing and physician services needed to make an adequate decision on potential recipients and living donors • All expenses necessary to obtain the organ • All expenses necessary in harvesting organs at your facility regardless of whether or not one of your patients becomes the recipient

Does that Mean Carte Blanche Spending? • Costs need to be reasonable and necessary in the delivery of patient care. • Remaining competitive in the market dictates we must remain frugal about how we spend money. • We must have policies and procedures in place that explain the need for the costs especially ancillary services testing. • We must ensure that the cost is related to evaluation & management of the patient and the organ procurement during the pre-transplant phase.

What’s Reasonable and Necessary in Pre-Acquisition Cost? • Salary & Benefits for Pre-Transplant time/ services • Tissue Typing/ HLA cost • All potential recipient evaluation & testing • All living donor evaluation & testing • Professional meetings & memberships • Space & office cost for pre-transplant services • OPO Organ Acquisition Costs • OPTN new patient registration fees • Square footage for pre-transplant space • Donation related complications of a living donor • Costs to administer the transplant programs according to licensing, certification and regulatory requirements

What is a Cost Center? • According to CMS – PRM 15 2302.8, a cost center is: “An organizational unit, generally a department or its subunit, having a common functional purpose for which direct and indirect costs are accumulated, allocated and apportioned.” • Generally a “cost center” involves: • Space where the service is provided. • Involves staff dedicated to provide the service within that space • Is a service which reports to hospital management and subject to facility policies.

What Expenses Are In An Organ Cost Center? • Salaries & Benefits of program personnel • OPO costs and other organ direct costs • HLA /Tissue Typing • Purchase services expenses (such as physician evaluation, outside ancillary testing) • Dues and other charges from UNOS for participating in the OPTN • Medical Director Expenses • Incidental expenses involved in taking care of the patient such as office supplies, telephone, freight, equipment and/or space rentals, repairs & maintenance, staff education, etc.

So Why are Organ Cost Centers so Important? • Organ acquisition is one of the very few services left that are reimbursed at cost on the Medicare cost report. • The transplant program’s involvement with a patient transcends through three different payment stages in the transplantation process. • Special Analysis and cost redirection must occur in order to report pre-transplant and organ acquisition costs on the cost report.

CMS’ Expectations of Hospital Accounting • The hospital has an accepted method for allocating cost correctly to the different areas of service within a transplant program. Time studies are the accepted method for cost allocation in the absence of dedicated personnel and services. • Proper analysis of any amounts reported in the cost report as being pertinent to the providers operations and allowed under the Medicare program as a service related to the care of patients. • Any information included in a Medicare cost report is subject to audit including non-ledger items such as statistics and the financials/ledger of anyone providing/ selling services to a Medicare Provider.

Other Organ Acquisition Expenses • Other Ancillary Services, Donor Stays, Harvests • These are not included in the organ cost center but they get added to the organ cost through a cost report analysis based on the charges for these services and the ratio of cost to charges of these different hospital areas. For the room & board the formula is based on the cost per patient day. (D-6 Parts I & II) • Indirect/ Overhead Costs • These costs are added to the direct expense of the organ cost center based on statistics that adequately demonstrate the use of the cost. (Example: Admin & general oversight, Cafeteria, Medical Records, Nursing Admin, etc. (D-6 Part III Line 51, w/organ direct expense)

Sample D-6 Part I – Computation of Organ Acquisition Costs (Inpatient Routine and Ancillary Services KIDNEY Computation of Inpatient Routine Service Costs Applicable to Organ Acquisition Routine Cr Loc Per-Diem Organ Cost Charges D-1 Cost D-1 Acq Days (Col 3x4) 1. 2. 3. 4. 5. Adults & Pediatrics 7,300 38. 716.24 10 7,162 ICU 1,800 43. 1,445.41 1 1,445 Total 9,100 11 8,607 Computation of Ancillary Service Cost Applicable to Organ Acquisition Ratio of Organ Acq. Organ Acq. Cost/Charges Anc Charges Anc. Costs 1. 2. 3. (Col 1x2) 4. Operating Room 37. .538023 70,086 37,708 5. Recovery Room 38. .625307 2,225 1,391 6. Radiology Diagnostic 41. .146996 318,369 46,799 ….. Total 1,885,283 378,509

Sample D-6 Part III – Summary of Cost and Charges • KIDNEY -------Cost--------- ----Charges---- Part A Part B Part A Part B • 48. Routine & Ancillary (Part I) 387,116 1,894,383 • 49. Interns & Residents (Inpatient) • 50. • 51.Direct Organ Acquisition 3,396,661 2,250,000 • 53.Total (sum lines 48-52) 3,783,777 4,144,383 • 54.Total Usable Organs 30 • 55.Medicare Usable Organs 25 • 56.Ratio Medicare to Total 0.833333 • 57.Medicare Cost/Charges 3,153,146 3,453,651 • 58.Revenue for Organs Sold 127,048 • 59.Subtotal 3,026,098 3,453,651 • 60.Organs Furnished Part B • 61.Net Organ Acquisition 3,026,098 3,453,651