Download

1 / 50

500 likes | 662 Views

Outline. A Tale of Two Companies 3 Immutable Laws (and their implications) Balanced Scorecard Budgeting Keys to Success Q&A. Sales Growth. 8%. 0%. Gross Margin %. 55%. 35%. SG&A as a % of Sales. 5%. 15%. EBITA as a % of Revenue. 15%. 3%. RONA %. 20%. 2%.

E N D

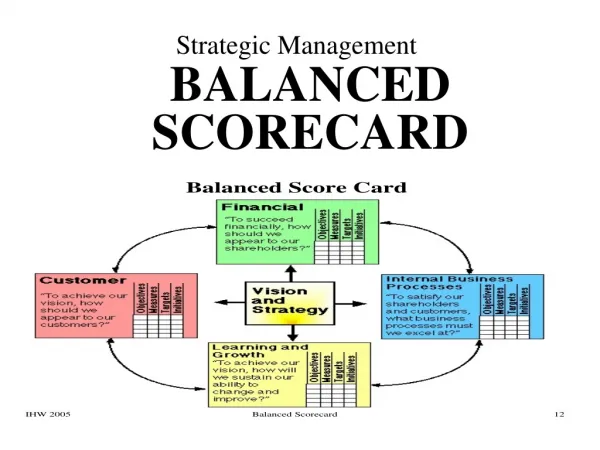

Outline • A Tale of Two Companies • 3 Immutable Laws (and their implications) • Balanced Scorecard Budgeting • Keys to Success • Q&A

Sales Growth 8% 0% Gross Margin % 55% 35% SG&A as a % of Sales 5% 15% EBITA as a % of Revenue 15% 3% RONA % 20% 2% A Tale of Two Companies Company snapshot: which company has been more successful? Company A Company B

Customer Satisfaction Index 90 75 5 20 # Defects per Thousand 70% % On Time Delivery 95% 18 mos. New Product Dev. Cycle Time 6 mos. Employee Satisfaction Index 90% 70% % of Sales Coming From Products Introduced in the Last 2 Years 20% 1% % Product Returns 1% 8% Company snapshot (part 2): why has Company A been more successful? Company A Company B

Sales Growth Customer Satisfaction Index # Defects per Thousand Gross Margin % % On Time Delivery SG&A as a % of Sales New Product Dev Cycle Time Employee Satisfaction Index EBITA as a % of Revenue % of Sales Coming From Products Introduced in the Last 2 Years RONA % % Product Returns Which way should the arrow go? Which set of measures drives the other?

Customer Satisfaction Index # Defects per Thousand % On Time Delivery New Product Dev Cycle Time Employee Satisfaction Index % of Sales Coming From Products Introduced in the Last 2 Years % Product Returns Measures for What ReallyDrives Success in the Business =

Set annual plan targets (numerical) Bake into the budget Report on every month to sr. exec team Analyze variances Set annual plan targets (numerical) Bake into the budget Report on every month to sr. exec team Analyze variances

Most companies manage to the P&L while the actual drivers of business performance “fade into the background”.

Highly successful companies manage to the real drivers of success… …and also understand how and why they impact the P&L

Set annual plan targets (numerical) Bake into the budget Report on every month to sr. exec team Analyze variances Customer Satisfaction Index Customer Satisfaction Index Customer Satisfaction Index # Defects per Thousand # Defects per Thousand # Defects per Thousand % On Time Delivery % On Time Delivery % On Time Delivery Employee Turnover Employee Turnover Employee Turnover Employee Satisfaction Index Employee Satisfaction Index Employee Satisfaction Index % of Sales Coming From Products % of Sales Coming From Products % of Sales Coming From Products Introduced in the Last 2 Years Introduced in the Last 2 Years Introduced in the Last 2 Years % Product Returns % Product Returns % Product Returns Balanced Scorecard Budgeting

Outline • A Tale of Two Companies • 3 Immutable Laws (and their implications) • Balanced Scorecard Budgeting • Keys to Success • Q&A

3 Immutable Laws Immutable Law #1: Strategy has no value on it’s own other than to achieve specific goals. Strategy for strategy’s sake is corporate make work. Implication Set corporate targets first, then build a strategy to meet them. That’s purpose built strategy.

3 Immutable Laws Immutable Law #2: It’s all about execution. A plan exists only in PowerPoint until it’s executed. Implication Build the ongoing monitoring and reporting mechanisms to ensure plans are being followed through on.

3 Immutable Laws Immutable Law #3: Any project, strategic or operational, will die unless resources are allocated to it. Implication The resources necessary to see a project though must be identified and included in the operating budget.

Outline • A Tale of Two Companies • 3 Immutable Laws (and their implications) • Balanced Scorecard Budgeting • Keys to Success • Q&A

Balanced Scorecard Budgeting KPIs Plan Monitor Budget

Balanced Scorecard Budgeting KPIs Step 1: Identify Company KPIs

Step 1: Identify Company KPIs Best KPIs Worst KPIs Used to make better decisions Shelfware Embraced by line managers Seen as not really relevant to line managers Reflects what actually drives success in the business Nothing but Financial Stats Cocktail Napkin Telephone Directory

Step 1: Identify Company KPIs The Value Driver Workshop Who: The Senior Management Team (or designates) What: A one day Workshop to identify what really drives success in the business (e.g, Innovation, being the Low Cost Producer, etc.) How: A series of facilitated workshop exercises Next

Step 1: Identify Company KPIs Identification of KPIs Who: The project work team What: A Workshop to translate what Senior Management has identified as driving the success of the business into Key Performance Indicators (KPIs) How: A series of facilitated brainstorming exercises

Step 1: Identify Company KPIs Customer Satisfaction Index # Defects per Thousand % On Time Delivery New Product Dev Cycle Time Employee Satisfaction Index % of Sales Coming From Products Introduced in the Last 2 Years % Product Returns Step 1 Deliverables: A Company Scorecard of KPIs

Balanced Scorecard Budgeting KPIs Plan Step 2: Establish targets for the KPIs

Step 2: Establish Targets for KPIs KPI Target Setting Who: KPI Teams What: Benchmarking and historical analysis to determine both long term (strategic) and short term targets for each KPI How: After a kick off meeting led by the KPI team leader, the group conducts benchmarking and historical trend analysis to establish long term (i.e., 3 to 5 years) targets as well as targets for the upcoming year. Depending upon the circumstances, this may take a few days to a few weeks.

Step 2: Establish Targets for KPIs Step 2 Deliverables: Targets for KPIs 2005 2006 2007 80 85 90 Customer Satisfaction Index # Defects per Thousand % On Time Delivery New Product Dev Cycle Time Employee Satisfaction Index % of Sales Coming From Products Introduced in the Last 2 Years % Product Returns

Balanced Scorecard Budgeting KPIs Plan Step 2: Establish targets for the KPIs Step 3: Develop Strategy to Achieve Targets

Step 3: Develop Strategy to Achieve Targets Develop Strategy to Achieve Targets Who: KPI Teams & SMEs (subject matter experts) What: Each KPI team develops a strategy that is designed to achieve the targets for their KPIs. This is a long term view that incorporates strategic initiatives. How: Each KPI team, working with internal experts and other subject matter experts develops a strategy, including long term initiatives, that if executed will achieve the targets established for the KPIs.

Step 3: Develop Strategy to Achieve Targets Step 3 Deliverables: Strategic Initiative Summary KPI: Employee Satisfaction ‘05-’07 Targets 2005: 80 2006: 85 2007: 90 Strategy Description Through investments job rotation and other programs, we will make our employees the most sought after in the industry. Clearly this will be “a win” for our employees, but it will also be a “win” for the company. If, in fact, our employees are the most sought after in the industry, that will be a major selling point in recruiting new talent. It also serves as an acid test for us, for in fact our employees are the most sought after in the industry, they most sought after skills and know how. We will be known as the company that enables employees to build their marketable skills and understanding of the business. Leader Hans Bergen [V.P., Career Development] • Integrate the goal of developing employees into each manager’s bonus calculation • Develop a career rotation program • Set standards for hours of training per year for each job level and monitor • Create a job shadowing program • Launch an alumni network Strategic Initiatives

Balanced Scorecard Budgeting KPIs Plan Step 2: Establish targets for the KPIs Step 3: Develop Strategy to Achieve Targets Step 4: Develop Action Plans to Achieve Near Term Targets

Step 4: Create Action Plans to Achieve Near Term Targets Develop Action Plans Who: KPI Teams What: Each KPI team develops Action Plans that are designed to achieve the targets for their KPIs. Particular attention is paid to what can be done in the first year. How: Each KPI team, working with internal experts and other subject matter experts develop Action Plans; complete with Activities, Tasks, and Milestones.

Step 4: Create Action Plans to Achieve Near Term Targets Develop Action Plans Who: KPI Teams What: Each KPI team develops Action Plans that are designed to achieve the targets for their KPIs. Particular attention is paid to what can be done in the first year. How: Each KPI team, working with internal experts and other subject matter experts develop Action Plans; complete with Activities, Tasks, and Milestones.

Step 4: Create Action Plans to Achieve Near Term Targets Step 4 Deliverables: Action Plans (Summary View) Career Rotation Program DEADLINE PROJECT LEADER Margaret Cho December BRIEF DESRIPTION Enable employees to rotate through various business units/ functional areas to build their skills and understanding of the business. (HIGH LEVEL) RESOURCE REQUIREMENTS KEY MILESTONES 1) Organize a cross functional team – April ’05 2) Draft a complete project charter (Objectives, Scope, Approach, Structure) – May ’05 3) Complete RFP process for outside expert – July ’05 4) Develop program blueprint – Oct ’05 5) Validate program with Sr. Management – Nov ’05 6) Implement program -- 2006 • INTERNAL • 8 Person cross functional team (on average 2 hours a week for 9 months) • 1 Procurement specialist to help us through the RFP process • EXTERNAL • HR Specialist (TBD)

Step 4: Create Action Plans to Achieve Near Term Targets Step 4 Deliverables: Action Plans (Gant Chart)

Balanced Scorecard Budgeting KPIs Plan Step 5: Develop Action Plan Budgets Budget

Step 5: Develop Action Plan Budgets Develop Action Plan Budgets Who: KPI Teams, working closely with Finance What: Each KPI team works with the Finance build budgets for their Action Plans How: Each KPI team, working with Finance, identifies the resources they need to execute their Action Plans. Finance then translates these resource requirements into SG&A line item detail and CAPEX requests for budget purposes.

Step 5: Develop Action Plan Budgets Step 4 Deliverables: Action Plans Budgets

Balanced Scorecard Budgeting KPIs Plan Step 5: Develop Action Plan Budgets Budget Step 6: Combine with the Baseline Budget

Step 6: Combine with the Baseline Budget Create a Baseline Budget Who: Finance and budget managers What: The Finance area facilitates the development of a baseline budget (“keep the lights turned on”) that can then be combined with the Action Plan budgets to produce a total company plan How: Working with managers, the Finance area develops a baseline budget, that incorporates all elements of the annual plan P&L, that is then combined with the Action Plan budgets.

Step 6: Combine with the Baseline Budget Step 6 Deliverables: A Combined Budget (Incorporating both Action Plan Budgets and the Baseline Budget

Balanced Scorecard Budgeting KPIs Plan Monitor Budget Step 7: Establish ongoing reporting and review

Step 7: Establish Ongoing Reporting Establish Ongoing Reporting & Review Who: Finance and IT work team. What: Finance and IT work together to build an ongoing reporting mechanism for: Financial Results, KPIs and the progress of the Action Plans. How: A combined Finance and IT work team identify requirements and select the tools that will enable monthly monitoring of results (both financial and KPIs). In addition, the work team will develop a process for the monthly review of progress of Action Plans alongside of the financial results.

Step 7: Establish Ongoing Reporting Step 7 Deliverables: Reporting and monitoring tools for KPI results

Step 7: Establish Ongoing Reporting Step 7 Deliverables: Reporting and monitoring tools for progress of Action Plans Career Rotation Program DEADLINE PROJECT LEADER Margaret Cho December BRIEF UPDATE We’ve slipped 60 days due to a delay in reaching a decision on our RFP vendor, but we should be able to make up half that time. KEY QUESTIONS KEY MILESTONES 1) Organize a cross functional team – April ’03 2) Draft a complete project charter (Objectives, Scope, Approach, Structure) – May ’03 3) Complete RFP process for outside expert – July ’03 4) Develop program blueprint – Oct ’03 5) Validate program with Sr. Management – Nov ’03 6) Implement program -- 2004 Project on Schedule? NO # Days Delayed: 60 Reasons? Senior management approval of vendor by 60 days. Actions to get back on track? Streamlining brainstorming and documentation should result in a savings of 30 days

Outline • A Tale of Two Companies • 3 Immutable Laws (and their implications) • Balanced Scorecard Budgeting • Keys to Success • Q&A

Keys to Success Keys to Success #1: Benchmark your company against national averages to quantify if your organization could benefit (or not): • Do people know what the strategy is? • Do they know how it links to the plan/budget? • Do they know what the company’s key performance measures are? • Do they think they have anything to do with them? • Do goals really cascade down through the organization? • Are we any different from national averages?

Keys to Success Keys to Success #2: Don’t create a separate budget exercise; bring balanced scorecard budgeting into your current process • Many companies make the mistake of creating a separate process for budgeting balanced scorecard initiatives. • But the “real” budgeting process still dictates how resources are allocated.

Keys to Success Keys to Success #3: Know thyself.Customize Balanced Scorecard Budgeting to suit your culture & planning processes • If you currently employ a rolling six quarter forecast, for example, then tailor the Balance Scorecard Budgeting approach to synch up with it. • If your strategic planning process looks out five years, for example, then your KPI targets should go out five years.

Keys to Success Keys to Success #4: Pick the right technology tools to enable Balanced Scorecard Budgeting. • After designing your Balanced Scorecard Budgeting process, develop a set of requirements for a planning/reporting system. • Determine if your current set of tools can meet the requirements • If the current set of tools will not adequately meet the needs, conduct a vendor selection process (with a minimum of three vendors).

Outline • A Tale of Two Companies • 3 Immutable Laws (and their implications) • Balanced Scorecard Budgeting • Keys to Success • Q&A