Understanding Mortgage Loans: Types, Terms, and Calculations Explained

A mortgage loan is a financial agreement secured by real property, typically used for purchasing land or homes. It involves essential terms like the borrower, lender, collateral, principal, and interest. There are two main types of mortgages: fixed-rate and adjustable-rate, each with distinct characteristics regarding interest rates and payment stability. Understanding how to calculate mortgage payments and the implications of foreclosures is crucial for potential homeowners. This guide offers a comprehensive overview of the mortgage loan process, key terms, and calculation examples.

Understanding Mortgage Loans: Types, Terms, and Calculations Explained

E N D

Presentation Transcript

What is a Mortgage Loan? • A loan secured by real property

What is a Mortgage Loan? • A loan secured by real property • Real Property: Land

What is a Mortgage Loan? • A loan secured by real property • Real Property: Land • Mortgage: the document which shows the property has a debt against it

What is a Mortgage Loan? • A loan secured by real property • Real Property: Land • Mortgage: the document which shows the property has a debt against it • The Mortgage is used to secure the debt

What is a Mortgage Loan? • A loan secured by real property • Real Property: Land • Mortgage: the document which shows the property has a debt against it • The Mortgage is used to secure the debt • Mortgage has become a generic term for the loan itself

Important Terms: Borrower: Lender: Collateral: Principal: Interest:

Important Terms: Borrower: Someone who is receiving money in exchange for a pledge to repay it Lender: Collateral: Principal: Interest:

Important Terms: Borrower: Someone who is receiving money in exchange for a pledge to repay it Lender: Someone who is providing money in exchange for a pledge of repayment Collateral: Principal: Interest:

Important Terms: Borrower: Someone who is receiving money in exchange for a pledge to repay it Lender: Someone who is providing money in exchange for a pledge of repayment Collateral: Property pledged to a lender to secure repayment of a debt Principal: Interest:

Important Terms: Borrower: Someone who is receiving money in exchange for a pledge to repay it Lender: Someone who is providing money in exchange for a pledge of repayment Collateral: Property pledged to a lender to secure repayment of a debt Principal: The amount of money being borrowed Interest:

Important Terms: Borrower: Someone who is receiving money in exchange for a pledge to repay it Lender: Someone who is providing money in exchange for a pledge of repayment Collateral: Property pledged to a lender to secure repayment of a debt Principal: The amount of money being borrowed Interest: Money paid to a lender in excess of the principal

What is Foreclosure? Foreclosure: the lender seizing control of or repossessing the property

What is Foreclosure? Foreclosure: the lender seizing control of or repossessing the property

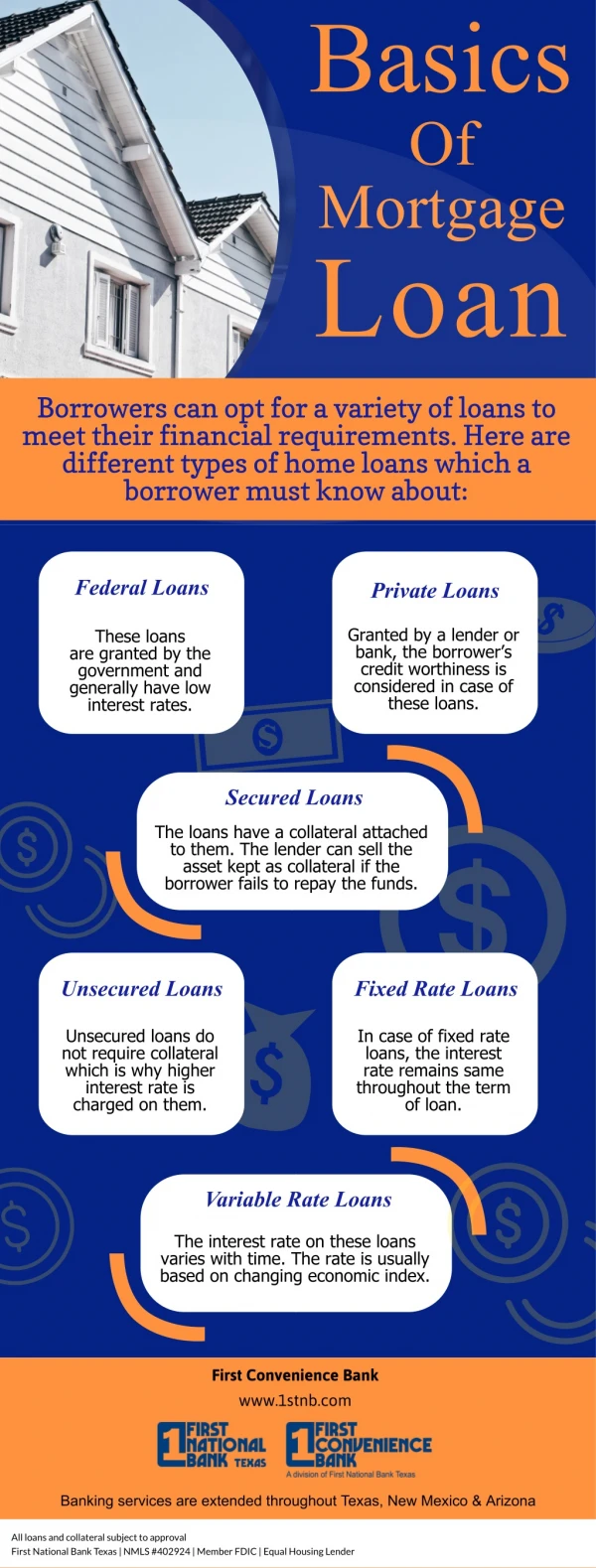

Two Types of Mortgages: • Fixed Rate Mortgage: • Adjustable Rate Mortgage:

Two Types of Mortgages: • Fixed Rate Mortgage: The interest rate is constant for the life of the loan • Adjustable Rate Mortgage:

Two Types of Mortgages: • Fixed Rate Mortgage: The interest rate is constant for the life of the loan • Therefore, the principle and interest payments remain the same for the life of the loan. • Adjustable Rate Mortgage:

Two Types of Mortgages: • Fixed Rate Mortgage: The interest rate is constant for the life of the loan • Therefore, the principle and interest payments remain the same for the life of the loan. • Adjustable Rate Mortgage: The interest rate of the loan resets periodically during the life of the loan

Two Types of Mortgages: • Fixed Rate Mortgage: The interest rate is constant for the life of the loan • Therefore, the principle and interest payments remain the same for the life of the loan. • Adjustable Rate Mortgage: The interest rate of the loan resets periodically during the life of the loan • With the changes to the interest rate, the principle and interest payments also change

Property Values: 3 Methods for determining values Actual Value: Appraisal: Estimated:

Property Values: 3 Methods for determining values Actual Value: The sale price of a property Appraisal: Estimated:

Property Values: 3 Methods for determining values Actual Value: The sale price of a property - Not usually available unless it is being purchased Appraisal: Estimated:

Property Values: 3 Methods for determining values Actual Value: The sale price of a property - Not usually available unless it is being purchased Appraisal: A value determined by a licensed professional Estimated:

Property Values: 3 Methods for determining values Actual Value: The sale price of a property - Not usually available unless it is being purchased Appraisal: A value determined by a licensed professional Estimated: A value obtained by the lender using an internal method

Formula for Calculating a Mortgage Payment Amount: c = the monthly principal and interest payment amount P = the principal balance of the loan r = the interest rate ÷ 12 N = the number of principal and interest payments

Example 1: You obtain a $200,000 mortgage loan at a rate of 5.25%. The loan is to be repaid over a 30 year period. What is the monthly principal and interest payment amount for the loan?

Example 2: You obtain a $375,000 mortgage loan at a rate of 6%. The loan is to be repaid over a 30 year period. What is the monthly principal and interest payment amount for the loan?

Calculating the Total Interest Paid Over the Life of the Loan: I = cN – P I = the total interest paid to the lender c = the monthly principal and interest payment amount N = the number of principal and interest payments P = the initial principal balance of the loan

Example 1: You obtain a $200,000 mortgage loan at a rate of 5.25%. The loan is to be repaid over a 30 year period. What is total interest paid over the life of the loan?

Example 2: You obtain a $375,000 mortgage loan at a rate of 6%. The loan is to be repaid over a 30 year period. What is the total interest paid over the life of the loan?