Download

1 / 24

240 likes | 722 Views

Value Chain Analysis (VCA) Target Costing (TC). Value Chain Analysis (VCA). Michael Porter’s Value-Chain. Developed in 1985 by Michael E. Porter in Competitive Advantage Highlights cost advantages and distinctive capabilities --the value processes

E N D

Value Chain Analysis (VCA) Target Costing (TC) STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value Chain Analysis (VCA) STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Michael Porter’s Value-Chain • Developed in 1985 by Michael E. Porter in Competitive Advantage • Highlights cost advantages and distinctive capabilities--the value processes • But note that there is no one template. STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value Chain and the QCT Triangle • VC allows alignment of processes with customers. This generates a quality advantage. • VC focuses cost management efforts. • VC provides for efficient processes which improves the timeliness of operations. STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value Chain Benefits • Identifies value processes • Identifies areas for cost improvement STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

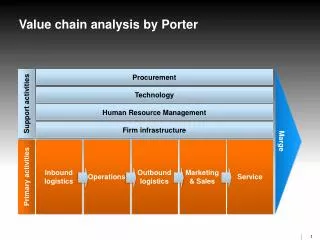

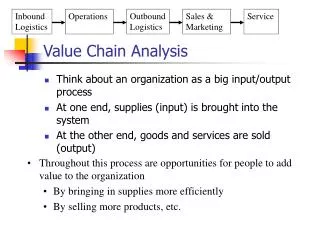

Value Chain Modelfrom Michael E. Porter’s Competitive Advantage SUPPORT ACTIVITIES Firm Infrastructure (General Management) Human Resource Management Customer Value Margin Technology Development Procurement Inbound Logistics Outbound Logistics Sales & Marketing Service and Support Ops. Margin Customer Value PRIMARY ACTIVITIES STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Customer value added Margin orientation Primary activities Inbound logistics Operations Outbound logistics Sales and marketing Service and support Support Activities Human resources (general and admin.) Tech. development Procurement Value Chain Elements STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Goal of Value Chain • Driven by customer perceptions • Increase margins • Focus on value processess • Distinctive capabilities • Cost advantages • Some examples • Southwest Airlines • Intel Corporation STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value Chain Analysis • Document the activities • Understand the cost and margins at each step. • Use Activity Based Costing • Map the value chain to the industry value chain • Look for core competencies • Map the cost structure • Note that external values drive cost advantages STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Discovering Your Own Value Processes • Distribute a summary of the value chain model. • Create functional process lists. • Transfer lists to color-coded labels. • “Pin the process” on a large VC diagram. • Identify appropriate processes as: • $ (cost advantage) • CC (core competency) STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Using the Value Chain • Helps you to stay out of the “No Profit Zone” • Presents opportunities for integration • Aligns spending with value processes • Provides for reconfiguration of the value chain • outsourcing • off-shoring • co-location with customers or suppliers • redesign for efficiency • Involves chain partners: customers & suppliers STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value Chain and the TBC Triangle • Technical: • Increases knowledge of no profit zones • Increases knowledge of forward and/or backward integration opportunities • Identifies value processes • Identifies win-win alliance opportunities • Behavioral: • Focus shifts to “the customer” • Focus shifts from conflict to partnering with customers & suppliers • Cultural • Creates externally focused mindset • Generates information sharing environment with respect for confidentiality STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Target Costing (TC) STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Life Cycle Costing Product SpecificationTarget PriceTarget ProfitTarget CostMajor Product and Process Design ChangesDoes the designmeet target cost?Estimate LifeCycle CostIs project life cycle cost acceptable?Put product into productionMinor Product and Process Design ChangesProduct Abandonment TargetCosting On-goingimprovement Abandonment STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Product Cost Life Cycle • R & D • Design • Production • Marketing & Distribution • Customer Service Upstream(focus for earlysettlement here) Downstream STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Shift in Strategic Impact • Shift focus from manufacturing costing to… • Upstream or downstream focus using the value chain STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Target Costing • Customer Orientation • Sets costs in the commitment phase-concurrent engineering • Supports keiretsu model via the value chain • Price led costing • Cross functional product teams • Focuses on life cycle costing STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Target Costing Process • Establishment phase • Market research • Competitor analysis • Niche definition • Customer requirement definition • Product feature definition • Market price determination • Profit rate STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Target Costing Process • Attainment phase • Cost gap computation • Design costs out • Design release and continuous improvement STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Cost Reduction • Cost analysis • Components list • Functional analysis • Customer requirement ranking • QFD Matrix • Relative functional rankings • Value engineering • Identify components for cost reduction • Generate cost reduction ideas • Testing and implementation • Cost estimates required at each design iteration STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

Value-Index Analysis • Choose features and options based upon customer preference • Value-Index = Cust. Preference % Feature Cost % • VI > 1…increase spending • VI < 1…decrease spending STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

TC-Strategic Implications • Quality is improved through the customer focus of target costing • Cost reduction is the heart of target costing • Time reduction is a natural by-product due to concurrent engineering STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

TC-Attribute Implications • Technical • Decision relevance improves (quality, cost and time issues are integrated) • Process understanding improves • Behavioral • Early finance involvement and teamwork are mandated • Undesirable attributes of longer development, burnout, feature creep & internal conflict can be managed STRATEGIC COST MANAGEMENT - BA122B – Spring 2011

TC-Attribute Implications, cont. • Cultural • Organizational culture must be prepared • Commitment to sustaining values must be established • Customer focus • Cross-functional cooperation • Open sharing of information STRATEGIC COST MANAGEMENT - BA122B – Spring 2011