Download

1 / 22

220 likes | 337 Views

Join us for an insightful workshop hosted by Bob Schwartz from Baruch College to delve into the complexities of market structure and volatility. This workshop will address the centrality of risk and uncertainty in finance, examining how they contribute to market behavior. Learn about high intra-day volatility patterns, the impact of price discovery, and liquidity creation, and explore regulation and corporate stabilization programs. This event promises critical insights into navigating today's unpredictable markets.

E N D

WFE Workshop on Market Structure & Statistics Paris, December 1-2 Markets at Risk Bob Schwartz Zicklin School of Business Baruch College, CUNY

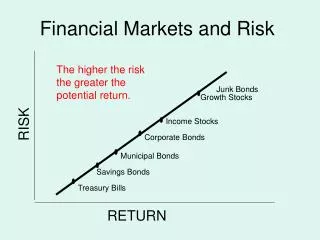

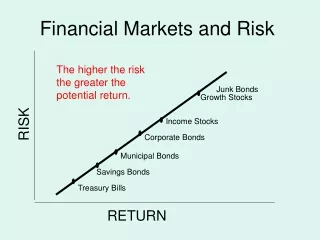

Volatility and Risk • Central importance in Finance • Risk has a well defined meaning • Risk is not the only contributor to volatility

Uncertainty • We do not know the probability distribution • We might not even know all of the outcomes • Uncertainty is a major contributor to volatility • We have not paid sufficient attention to uncertainty as a cause of volatility

An Ant A Little Red or Black Animal That Can Crawl Around and Annoy Us Individually so dumb, collectively very smart

Security Traders Individually very smart, collectively so dumb

Why So Dumb? • There is a great deal about volatility that we do not understand • There is quite a bit that we thinkwe understand but don’t! That’s dangerous!

High Intra-day Volatility • Really high volatility has been with us for over a year • I do not mean long-run vol (weeks, months, or years) but… • Intra-day vol! • Price changes of 1%, 2% or more are common • A 1% daily price change 250% annual change! • What does intra-day volatility look like?

The First 1/2 Hour INTRA-DAY VOLATILITY NYSE

The First 1/2 Hour INTRADAY VOLATILITY NASDAQ

INTRADAY VOLATILITY LONDON STOCK EXCHANGE The First 1/2 Hour

INTRADAY VOLATILITY EURONEXT PARIS The First 1/2 Hour

The First 1/2 Hour INTRADAY VOLATILITY DEUTSCHE BÖRSE

My Current Nasdaq Study “The Quality of Price formation at Market Openings & Closings: Evidence from the Nasdaq Stock Market” Michael Pagano, Lin Peng, and Robert Schwartz • 52 large cap Nasdaq firms • Time period: Feb 04 and Feb 05 • We examined per day: • 390 1-minute intervals (9:30-16:00) • 30 10-second opening intervals (9:30-9:35) • 30 10-second closing intervals (15:55-16:00) • Volatility measured by high-low range for the interval

60 bps Feb 2005 (Post-Calls) Nasdaq Volatility Differences Between Feb 2004 and Feb 2005One-minute Volatility 60 bps Feb 2004 (Pre-Calls) w

Nasdaq Volatility DifferencesBetween Feb 2004 And Feb 200510-Second Volatility 40 bps Feb 2005 (Post-Calls) 40 bps Feb 2004 (Pre-Calls) 5 Min After Opening 5 Min Before Close 5 Min Before Close 5 Min After Opening

What Explains Accentuated Vol? • Reason One: Price discovery • Reason Two: Liquidity creation doesn’t just happen • Volatility in opening minutes:Price discovery • Volatility in closing minutes: End of day effects • Volatility at any time of the day: One-sided markets

Reason One: Price Discovery • A difficult process • Especially complex when some investors are influenced by what they see other investors doing… • That is when we get information cascades

Reason Two: Liquidity Creation • Markets are generally two-sided under a spectrum of conditions • But sometimes they are one-sided…. • Liquidity dries up on one side of the market and volatility spikes… • Information cascades… • And, when prices head south, who wants to catch the falling knife?

What To Do About It?1. Market Structure • Transparency vs. opacity • Consolidation vs. fragmentation • Temporal consolidation and call auctions • Circuit breakers and volatility interruptions • Stabilization programs

Corporate Stabilization Programs • A corporation can set up a STABILIZATION FUND • Doing so is VOLUNTARY • The fund is RUN BY A FIDUCIARY • Shares and capital are put into the fund • Shares are purchased in a falling market but… • Shares are also sold in a rising market • All orders are entered at pre-announced price points in pre-announced sizes according to an algo formula that is common knowledge • Orders are executed in call auction trading only • I proposed this in Fall 1988. I still believe in it.

What To Do About It?2. Regulatory Structure • We have been hit by tidal waves of volatility • Regulation is indeed needed • But it must be appropriate • Will it be? • One thing is for sure…

The financial turbulence of 2008 has given us all a great deal to think about! Thank You!