Download

1 / 9

90 likes | 110 Views

Find important details on Business Line of Credit in Australia. pros, cons, procedure with details on who can apply for it and how.

E N D

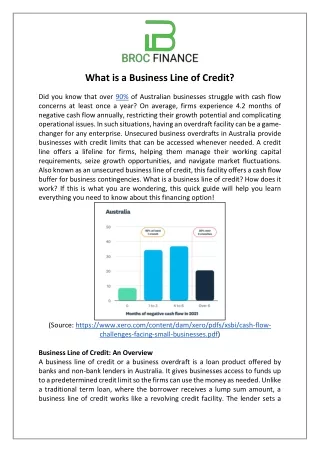

What is a Business Line of Credit? Did you know that over 90% of Australian businesses struggle with cash flow concerns at least once a year? On average, firms experience 4.2 months of negative cash flow annually, restricting their growth potential and complicating operational issues. In such situations, having an overdraft facility can be a game- changer for any enterprise. Unsecured business overdrafts in Australia provide businesses with credit limits that can be accessed whenever needed. A credit line offers a lifeline for firms, helping them manage their working capital requirements, seize growth opportunities, and navigate market fluctuations. Also known as an unsecured business line of credit, this facility offers a cash flow buffer for business contingencies. What is a business line of credit? How does it work? If this is what you are wondering, this quick guide will help you learn everything you need to know about this financing option! (Source: https://www.xero.com/content/dam/xero/pdfs/xsbi/cash-flow- challenges-facing-small-businesses.pdf) Business Line of Credit: An Overview A business line of credit or a business overdraft is a loan product offered by banks and non-bank lenders in Australia. It gives businesses access to funds up to a predetermined credit limit so the firms can use the money as needed. Unlike a traditional term loan, where the borrower receives a lump sum amount, a business line of credit works like a revolving credit facility. The lender sets a

credit limit, and the borrowing firm can withdraw money within that limit and pay interest on the amount they borrow. In most cases, a small business line of credit in Australiafalls under unsecured business loans. However, the borrower may have to offer collateral if they want a significantly high limit for their overdraft facility. A business line of credit in Australia is perfect for enterprises that struggle with short-term cash flow fluctuations. It offers a convenient buffer for such contingencies, easing the financial strain of running the operations. How Does a Business Overdraft Work? A business overdraft is a unique credit facility that provides businesses with a safety net during cash flow challenges. With a line of credit, firms have the freedom to use the funds as needed, whether it is to manage seasonal fluctuations or buy stocks to meet customer demand. Let’s break down how this credit option works: ●A business applies for a credit line according to its anticipated needs. ●The lender evaluates the turnover and financial standing of the applicant. ●The lender approves a stipulated credit limit for a certain number of months/years. ●The firm withdraws funds as needed, provided the total amount remains within the set limit. ●The firm pays interest on the amount they borrow, and not on the approved limit. In most cases, a small business overdraft facility in Australia works on a revolving basis. This means that the line of credit has an open-ended limit, allowing the borrower to withdraw and repay money as many times as they want. For example, let's assume that a small business gets a business overdraft facility with a limit of $100,000. If it has a revolving facility, the firm can borrow $50,000, repay it, and borrow another $70,000 within the same month. As long as the outstanding amount at any point in time is lower than the credit limit, the firm can borrow the sum they need. A line of credit allows borrowers to churn the money more efficiently to leverage the overdraft according to their requirements. Unsecured business overdrafts in Australia ensure convenience and flexibility for SMEs, helping them finance their survival growth. In a country where 99% of

businesses are small or medium-sized, a business overdraft is a valuable facility to ensure stability for thousands of firms. By utilising a line of credit, enterprises can navigate cash flow fluctuations and stay on track towards success. Here are some of the salient features of a small business line of credit in Australia: ●Amount: Lenders determine the credit limit based on business performance and other factors. ●Tenure: A small business overdraft facility in Australia is typically available for up to five years. When firms have constant access to a line of credit for a prolonged period, they can often manage their finances more efficiently. ●Interest Rate: Business overdraft interest rates in Australia depends on the risk score of a business determined by the lender. Lenders usually take into consideration the trading time, industry, credit score and the borrower's financial performance while determining the rate of interest. ●Repayment Frequency: Businesses can make their repayments weekly or monthly. These are amortised over time, ensuring significant flexibility for borrowers. How is a Business Line of Credit Different from Other Business Loan Products? A business line of credit stands out from other business loan products due to its flexibility and convenience. Unlike small business loans that provide a lump sum amount, a business line of credit allows borrowers to access funds on an as- needed basis, similar to a credit card. Businesses pay interest only on the amount they withdraw, saving them money in the long run. With its revolving nature and tailored repayment terms, a business line of credit empowers businesses to effectively manage their cash flow and seize opportunities when they arise. While it is easy to distinguish between a line of credit and traditional business loans, many people struggle to differentiate between an overdraft facility and credit options like invoice financing and debtors financing. Let’s assess how a line of credit differs from these funding solutions: ●Security: Invoice financing options are secured with unpaid invoices while debtors financing is secured with the borrower’s receivables ledger. However, unlike both these options, unsecured business lines of credit require no proof of incoming payments.

●Limit: A business can only borrow upto 80-90% of their invoice amount/receivables ledger under an invoice/debtors finance facility. However, with a line of credit there’s no such limitations or reliance on the debtors/invoices. ●Flexibility and Control: Invoice financing offers the flexibility to draw funds when businesses have high invoice realisation periods. Debtors financing allows borrowers to get funds without waiting for their customers to pay. It also allows them to leverage lower interest rates if their debtors repay early. However, a line of credit offers greater flexibility and control than both these options, allowing businesses to manage their money during contingencies without relying on their creditors’ decisions. A line of credit or overdraft facility is extremely unique, offering businesses a plethora of benefits if managed efficiently. It can be a convenient alternative to traditional working capital loans, allowing firms to manage their urgent expenses with ease. Pros and Cons of Taking a Line of Credit For Your Business Now that you know how a business overdraft works and how it compares to other business loans, it’s time to dive deeper. What are the advantages of getting a line of credit for your firm? Let’s find out: ●Flexibility and Convenience: The flexibility of fund usage is one of the biggest advantages of getting a business overdraft facility. You can use it to address various business needs: like buying inventory, paying wages, marketing, and managing cash flow requirements. With this financial tool at your disposal, you can seize opportunities promptly without the need for lengthy loan applications. ●Do not necessarily require security: SMEs can get unsecured business overdrafts depending on their performance and requirements. If a firm lacks the necessary assets to apply for secured business loans, it may get an unsecured credit line to manage its urgent expenses. However, some lenders also offer secured lines of credit for borrowers who can offer collateral. Business owners can evaluate both options and choose the one that fits their needs.

●Absence of Repayment Penalties: With a business line of credit, you have the flexibility to pay off the borrowed amount early without incurring any penalties. This gives you the freedom to manage your finances efficiently and save on unnecessary interest costs. For example, if you borrow $20,000 out of your $100,000 limit and repay it within ten days, you need not pay any additional charges for the early repayment option. ●Savings on Interest Costs: One of the most significant advantages of a business overdraft facility is that you only pay interest on the amount you use. This aspect often results in substantial savings compared to traditional loans where interest accrues on the entire loan amount from the start. Moreover, business overdraft interest rates in Australia are quite affordable, making this a suitable option for numerous SMEs. ●Continuous Backup for Contingencies: A business line of credit offers peace of mind as lenders provide this facility for up to five years. It acts as a valuable backup during contingencies and helps you navigate business challenges with ease. When you have a line of credit, you can plan and execute your business strategies more efficiently without worrying about immediate repayment deadlines. While a business line of credit provides flexibility and easy access to funds, there are some potential issues to consider. Here are some possible disadvantages of taking this option: ●Credit Score and Monthly Turnover Requirements: Lenders often give preference to borrowers with good credit scores when it comes to approving new lines of credit. Most lenders also require a minimum monthly turnover of $10,000 to provide the overdraft facility to enterprises. These requirements may be challenging for new businesses or those with lower credit ratings, limiting their access to this type of financing. ●Line Fees: Lenders may charge a small line fee on the overall credit limit, in addition to regular interest rates. These fees can impact the cost of borrowing and business owners should take them into account while assessing the affordability of an overdraft facility. ●Possibility for Limit Reduction: Lenders have the right to review and reduce the credit limit for an overdraft facility. They may reduce or withdraw the credit limit if they observe irregularities in repayments, a decline in business turnover, or misuse of funds. Hence, the borrower must be careful in the way they utilise their line of credit.

Potential borrowers must weigh the pros and cons before exploring this business financing tool. If managed effectively, a line of credit can be a valuable resource for managing business requirements and funding expansion and growth. Hence, borrowers should strike a balance between the upsides and downsides to make the most of this option. Who Can Apply for a Business Line of Credit? A business line of credit is available for eligible SMEs that meet the lending criteria for the issuance of this facility. Typically, the lenders accept business overdraft applications from businesses that meet the following requirements: ●An Active ABN: An applicant must have a valid and active Australian Business Number (ABN) to apply for this business loan product. Registered SMEs should provide the ABN during the application stage. ●Business Duration: Lenders typically require businesses to have been operating for at least 12 months. This aspect demonstrates stability and viability in the eyes of the lender. ●Minimum Monthly Turnover: Most lenders require borrowers to have a monthly turnover of $10,000 or more for providing them with lines of credit. This criterion ensures that your business generates sufficient revenue to handle the credit line responsibly. If your enterprise meets these requirements, you can consider getting an overdraft facility. You may consult an experienced financial broker to discuss your eligibility and other factors that affect the approval of a credit line. Why Should a Business Consider Having an Overdraft Facility? If your business has sufficient funds to run day-to-day operations, you may think that there is no need to opt for a credit facility. But having a line of credit can be a game-changer for your firm, providing you with the requisite flexibility to make quick business decisions. Even if you have no immediate need for a loan, you can get a line of credit to act as a financial buffer. An overdraft facility acts as a valuable contingency plan. Unforeseen expenses, sudden market fluctuations,

or unexpected opportunities can arise at any time. However, firms can rely on their credit lines to navigate these contingencies without disrupting their operations or missing out on opportunities. By having access to readily available funds, businesses can maintain stability and continue their operations seamlessly, even during lean periods. Moreover, an overdraft facility demonstrates financial responsibility and builds a positive credit history. Lenders perceive businesses with an approved overdraft as proactive and well-prepared, making them seem more credible and trustworthy. As a result, it helps open doors to better financing solutions and favourable loan terms in the future. Essentially, having an overdraft facility fosters financial agility and adaptability. In today's competitive landscape, businesses must respond to market demands and swiftly capitalise on growth opportunities. An overdraft facility ensures that firms can seize these opportunities promptly without the delays associated with traditional loan approval processes. How Do Lenders Determine Credit Limits for Businesses? When businesses seek a line of credit, understanding how lenders determine credit limits is crucial. In Australia, lenders assess various factors to determine the maximum amount of credit they can extend to a business. Here are the key considerations that lenders take into account while evaluating applications: ●Financial Position: Lenders assess a business's financial strength by analysing its cash flow position, turnover trends, and repayment capacity. If your business has a high monthly turnover, you may get a proportionately high credit limit as you can afford to repay the funds on time. On the other hand, firms with lower turnover figures get smaller credit lines. ●Business Duration: Your firm can get an overdraft facility if it has been operational for a year or more. Typically, lenders look at the borrower’s time in business to assess the credit risks. They often perceive businesses with more than a year of operation as being more stable, making them more likely to handle additional debt obligations. ●Security: While many firms are likely to qualify for unsecured lines of credit, lenders often favour businesses that can provide assets as collateral. Having assets to offer as security increases the likelihood of obtaining a higher credit limit with more favourable terms.

●Industry Characteristics: The industry in which a business operates plays a role in determining the approved credit limit. Lenders evaluate the risks associated with the borrower’s industry and analyse market conditions before finalising the credit line. They often assess the typical payment cycles within various industries to ascertain whether a borrower can keep up with regular repayments. ●Credit Score: A firm’s credit score helps lenders assess their risk level. A higher credit score instils confidence in lenders, increasing the likelihood of approval for a higher credit limit. Conversely, a lower credit score may lead to a lower credit limit. While bad credit business loans are available for enterprises with poor credit scores, it helps to have a good credit history when looking for overdraft facilities. Analysing these factors can help you estimate how much you can borrow through a credit line. You can discuss your firm’s characteristics with a business loan expert to determine likely credit limits you can get for your business! How to Apply for a Business Line of Credit? Documents and Procedures Now that you know the different aspects of this credit option, you may be wondering about the application process. How to apply for a business overdraft? Let’s break it down: #1 Assess Your Eligibility and Requirements You should consider the lending criteria and determine your eligibility before applying for an overdraft facility. You can also analyse aspects like your time in business, industry characteristics, turnover, and other requirements to ascertain how much you can get in terms of a credit limit. #2 Consult a Finance Broker You can discuss your situation with a financial broker to get their opinion and advice. Experienced consultants provide valuable insights, help you understand the options available, and guide you through the application process. They can also help you compare business loans and determine whether a secured or unsecured line of credit is the best solution for your business! #3 Get an Indicative Quote

Business loan specialists can provide you with an indicative quote to help you estimate the credit limit and interest rates you may get. To get this quote, you can fill up details like your firm’s average monthly turnover and credit requirements. Once you get the estimate, you can make an informed decision about applying for a credit line. #4 Prepare Your Documents Business lines of credit do not require elaborate paperwork for approval and settlement. For credit lines up to $250,000, you can get a low-doc approval with the following documents: ●Bank statements for the past six months. ●The business owner’s valid identification proof. If you want a credit limit higher than $250,000, you may opt for the full-doc approval process. The additional documents required for this process are as follows: ●ATO Statements ●Financial Statements ●Proof of Property Ownership Before filing your application, you should prepare the relevant documents to ensure a seamless application process. #5 Submit Your Application and Wait for Approval The application process is simple and convenient. You can apply online with the help of your broker and upload all the necessary documents. The pre-approval formalities take 24-48 hours while unconditional settlement and approval take one to three days. Once you submit your application, you must wait for a maximum of three days to get a final decision from the lender. When you get the approval, you should review the paperwork carefully to understand the terms and conditions of the credit facility. If you have more questions about how to apply for a business overdraft, you can contact our expert at Broc Finance! Our financial brokers can resolve your queries and help you apply for a credit line. Call our team today to learn more about your loan options! Source: https://www.brocfinance.com.au/blog/what-is-a-business-line-of- credit/