Download

1 / 43

430 likes | 578 Views

Central banks in chaotic times. Implications of the financial crisis for central bank procedures and our understanding of monetary theory. Outline. The operations of the Fed and the US Treasury The operations of the Bank of Canada and the Canadian government.

E N D

Central banks in chaotic times Implications of the financial crisis for central bank procedures and our understanding of monetary theory

Outline • The operations of the Fed and the US Treasury • The operations of the Bank of Canada and the Canadian government

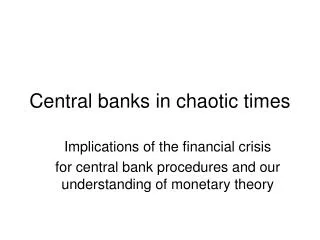

The explosion of the balance sheet of the Fed January 2008 July 2008 January 2009 July 2009

The timeline at the Fed I • Financial pressures started in mid-August 2007. • Real financial pressures started at the end of December 2007. The Fed is forced to make use of its lending facilities, providing loans (liquidity) to banks. • The expansionary effects of the central bank loans are neutralized by open market operations. • Until 12 September 2008, the Fed is able to move the federal funds rate next to the FMOC target interest rate (2%). • It is able to do so because the neutralizing operations of the Fed keep reserves at their approximate required level.

Initially, the Fed keeps the supply of reserves on line with the demand for them, and the expected fed funds rate is the target rate S Lending rate Target Fed rate Expected Fed funds rate Demand for reserves Deposit rate Reserves

Timeline at the Fed II • On 15 September 2008, the Lehman Brothers investment bank is let go and declares chapter 11 bankruptcy. • From then on, the Fed is unable to achieve its target (fed funds rate is at first too high) • From 19 September 2008, the Fed decides to inject huge amounts of liquidities (provide huge lending facilities to the banks (and AIG)), without neutralizing them. • This is when the balance sheet of the Fed starts exploding. • The Fed loses control of the fed funds rate.

The demand for excess reserves explodes as the banks lose confidence in each other: the fed funds rate rises S Lending rate Fed funds rate Target rate Demand for reserves Deposit rate Reserves

The demand for excess reserves keeps exploding: the Fed stops neutralizing its lending facilities: fed funds rate drops S S’ Lending rate Target rate Fed funds rate Demand for reserves Deposit rate Reserves

Timeline at the Fed III • On 6 october 2008, the Fed gets the authority to set interest rates on (excess) reserves, thus setting up a corridor system, with a ceiling (the discount rate) and a floor (the interest rate on reserves). • On October 22, the corridor gets reduced from 100 basis points to 50 basis points, as in Canada. • Despite this, the Fed lost control of the federal funds rate, with a target at 1.50% and fed funds rate hovering between 0.67% and 1.04%.

This is what should have happened with the corridor system: the fed funds rate is at least equal to the deposit rate S S’’ S’ Lending rate Target Fed funds rate Demand for reserves Deposit rate Reserves

Timeline at the Fed IV • On 6 November 2008, the Fed interest rate on all reserves is set as the target fed funds rate (1%). • Despite this, the fed funds rate hovers between 0.10% and 0.62%, getting ever lower. • Finally, on 17 December 2008, the Fed announces a target between 0 and 0.25%, with a rate on reserves at 0.25%, and actual fed funds rate in 2009 between 0.10 and 0.24%.

This is what should have happened with the target rate set at the deposit rate, and with a large amount of reserves : the fed funds rate is exactly equal to the deposit rate S’ Lending rate Demand for reserves Target rate and Deposit rate Reserves

Why doesn’t the fed funds rate stay at the bottom of the corridor? • Not all participants (GSEs) to the fed funds market are eligible to receive interest on their reserve balances. • There are also foreign institutions that hold balances at the Fed that don’t get interest on reserves. • They may thus lack bargaining power and being forced to lend their surplus funds at a rate below the floor.

The Bank of Canada • During the whole chaotic period, with very few exceptions, the BOC achieved its target interest rate. Why? • Because in contrast to the Fed, the BOC knows both the demand for reserves (settlement balances) and the amounts that it is supplying.

Until April 2009, this was the corridor scheme at the Bank of Canada S Lending rate = TR + 0.25% Target rate TR Demand for balances Deposit rate = TR – 0.25% Settlement balances 0

But the BOC then moved to its new framework, zero-interest rate policy (ZIRP) • Conditional promise to keep the target overnight rate where it is for more than a year • Set the deposit rate on bank balances at the target overnight rate, as in the US • Quantitative easing (unsterilized operations) • Credit easing (sterilized or unsterilized): the Bank purchases certain private sector assets in certain credit markets). This was previously done indirectly through the PRA program where collateral can be ABCP, and through the purchases of the CMHC. This could be done to reduce interest rates on private assets relative to safe government assets.

The new ZIRP framework of the BOC, 21 April 2009 But if things go wrong, there is no incentive to lend on the overnight market; Banks would rather deposit their excess funds at the Bank, at the same rate. Overnight rate S = $3,000M Bank rate = TR+25pts = 0.50 Target rate = Rate on positive balances = 0.25 Settlement balances - (overdraft) + (surplus) 0

The Decoupling Principle • With the target interest rate set at the floor of the corridor, central banks (FED, BOC) can now set the target rate at the level of their choice and simultaneously set the amount of reserves at the level of their choice. There is no relationship anymore between reserves and overnight rates. • This is the decoupling principle (Borio and Disyatat 2009, BIS). • This was recommended (briefly) by Goodfriend (2002). • It was endorsed in New Zealand and Norway before the crisis.

Quiet times until 17 September 2008 • There is a small increase in the balance sheet of the BOC before September 17, but this is because there is a larger stock of currency in the system. • But with the bankruptcy of Lehman Brothers and its world repercussions, the BOC is constrained to provide liquidity. This is done in three ways, one of which will increase the size of the BOC balance sheet.

Three strategies to improve the liquidity of the balance sheet of banks. • First, banks sold some of their mortgages to the CMHC, obtaining bonds. This does not involve the BOC. • Second, the Bank granted 28-day purchase and resale agreements (PRA - repos) backed by the same less liquid assets, sterilizing these purchases by first acquiring T-bills from the federal government, and then selling these T-bills to banks (17 September 2008 to 1 October) • Third, the Bank of Canada granted 28-day purchase and resale agreements (PRA) backed by ABCP and less liquid securities (long-term federal, provincial), sterilizing these purchases by selling its T-bills to banks (1 October to 15 October). • Fourth, the BOC reverted to the second strategy.

Central bank independence is an illusion • During the fight against the financial meltdown: • The balance sheet of the Bank of Canada jumped up from $53 billion in August 2008 to $80 billion in March 2009; • The total amount of Government of Canada securities outstanding jumped up from $402 billion in August 2008 to $497 billion in March 2009. • This was before the government started raking up deficits.

Central bank independence is an illusion • “Just as the boundary between monetary stability and financial stability becomes increasingly blurred in the midst of a financial crisis, so too does the boundary between monetary and fiscal policy actions. It isn’t uncommon for both central bank and governments to initiate credit-easing measures, and it is important that the two work together” (Deputy Governor Murray, 19 May 2009).

Where did the mortgages go? • They were purchased by the Canadian Mortgage and Housing Corporation (CMHC) to the tune of $51 billion as of March 2009, through the Insured Mortgage Purchase Program. • $125 billion has been set aside for this (25 in September 2008, 50 in November 2008 and 50 in the January 2009 Budget) • The program now seems to be stalling.

How did CMHC acquire the mortgages? It got loans from the federal government

Impact of term PRA operations on LVTS balances when the size of the balance sheet of the Bank of Canada is NOT rising

Impact of term PRA operations on LVTS balances when the size of the balance sheet of the Bank of Canada is rising

Composition of the term purchase and resale agreements conducted by the Bank of Canada Billions of dollars

A Paradox • The post-Keynesian view (Kahn, Radcliffe, Moore), whereby central banks act through interest rate targeting, is now called the conventional view by central bankers. • Trying to change the amount of (excess) reserves, directly or indirectly, is now called unconventional policy!

US officials vs Canadian ones • It is clear that officials at the NYFR are fully aware of the required changes in monetary policy, as well as some at the BIS. • It is not so clear that Bernanke and vice-governor Murray fully understands how the monetary system is set up.

Quantitative easing • We are right now in a situation of quantitative easing. • Since 21 April 2009, settlement balances are set each day at $3 B by the central bank (banks have $3B reserves, instead of zero as before). • The only difference is that, instead of the excess settlement balances being provided by moving around government deposits, quantitative easing would provide the excess balances through open market operations (or by purchasing private assets).

Misleading claims on behalf of quantity easing • “The expansion of the amount of settlement balances available to [banks] would encourage them to acquire assets or increase the supply of credit to households and businesses. This would increase the supply of deposits” (Bank of Canada, Monetary Policy Report, Annex, 23 April 2009). • “[Quantitative easing injects] additional central bank reserves into the financial system, which deposit-taking institutions can use to generate additional loans” (Deputy Governor John Murray, May 2009)

Quantitative easing = mistaken textbook story • “Although quantitative easing is now referred to as an unconventional monetary policy tool, the purchase of government securities is, in fact, the conventional textbook approach to monetary policy…. In practice, most central banks have chosen to conduct monetary policy by targeting the price of liquidity because the relationship between the amount of liquidity provided by the central bank and monetary aggregates on the one hand, and between monetary aggregates and aggregate demand and inflation on the other, are not very stable.” (Bank of Canada, Monetary Policy Report, Annex, 23 April 2009).

Quantitative easing = monetarism • “All quantitative easing is, by definition, ‘unsterilized’. Although this is correctly viewed as unconventional, it closely resembles the way monetary policy is described in most undergraduate textbooks, and is broadly similar to how it was conducted in the heyday of monetarism” (Deputy Governor John Murray, May 2009).

Quantitative easing is useless • It assumes that credit is supply-constrained. • It assumes that banks will grant more loans because they have more settlement balances. • The only effect might be to lower interest rates on some assets. Will this have an impact on lending rates or on the exchange rate? • Experience with the Bank of Japan: “Given that the interest rate is zero, no policy measures are available to lift the inflation rate to positive territory… The Bank did not have the tools to achieve it” (BoJ arguments as assessed by Ito, 1994).

The Bank of Canada claims that conventional monetary policy is now helpless • The inflation rate is approaching negative territory and the overnight interest rate is nearly at zero, so that the real overnight rate can’t be negative anymore. • The spreads between the overnight rate and market rates are much higher than they used to, so that the reduction in the overnight rate has not been as effective as if spreads had remained constant. • Since 2007 QIII, loan officers have been tightening lending conditions, and just stopped doing it.

Overall business-lending conditions: Balance of opinions Bank of Canada website, Senior Loan Officer Survey, January 2010.

Clinging to inflation targeting • While the rest of the world is plunging into financial chaos and depression, the Bank of Canada still claims that: • “Low, stable, and predictable inflation is the best contribution that monetary policy can make to the economic and the financial welfare of Canadians” (Monetary Policy Report, April 2009, p. 25; same sentence in Carney’s speech of 1st of April 2009). • “Any unconventional action initiated by the Bank must have as its primary objective the achievement and maintenance of the Bank’s 2 per cent inflation target” (Deputy Governor Murray, May 2009)

The problem of central banks today • Standard theory says that reserves create money, and money creates price inflation. • So if there are large reserves, we should soon have inflation, because interest rates should be too low. • But the decoupling principle shows there is no relation between reserves and interest rates, and hence no relation with prices. • « There is a concern that markets may at some point, possibly based on the ‘wrong model’, become excessively concerned about the potential inflationary implications of these policies » ((Bordo Disyatat, p. 22). • Gone are models of rational expectations within a single model of the macroeconomy!

Central bank communications • There is a big effort by central bankers in the US to convince financial experts that the correct monetary theory has changed. • Keister and McAndrews claim that no inflationary pressures can arise when the target fed rate is the deposit rate. • They reluctantly give some credibility to the multiplier story when a corridor system is in place.

Keister (NYFR) in personnal communication • I agree with you on the money multiplier, but I would state things in a slightly different way. In order for the money-multiplier story to make sense, it must be the case that it (implicitly, at least) works through lowering interest rates. The process must go just as you described, with the increase in reserves lowering market rates, which makes more potential projects profitable.

Keister continued • I understand your comment to be that this mechanism is not the "money multiplier" as commonly described. We decided to be more generous to the textbooks and say that this mechanism must be what they had in mind, even if they left out the part about interest rates to simplify things for the students. Importantly, I think we agree on the point that discussions of the money multiplier have done more harm than good in terms of helping people understand what is going on.