Download

1 / 49

490 likes | 637 Views

This lesson explores the concepts of journalizing purchases using a purchases journal and the cash payments journal. It covers essential vocabulary such as merchandise, merchandising businesses, retailers, and wholesale operations. Key terms include capital stock, stockholders, purchase on account, purchase invoices, cash discounts, and trade discounts. The lesson emphasizes the importance of special journals for recording specific types of transactions, saving time, and ensuring accuracy in accounting practices within retail and wholesale contexts.

E N D

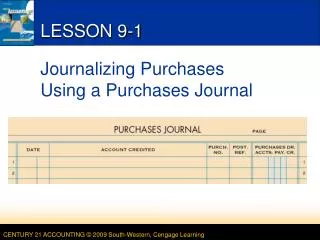

LESSON 9-1 Journalizing Purchases Using a Purchases Journal

New Vocabulary • Merchandise: Goods that a business purchases to sell • Merchandising business: A business that purchases and sells goods • Retail business: A merchandising business that sells to those who use or consume the goods • Wholesale merchandising business: A business that buys and resells merchandise to retail merchandising businesses Chapter 9

New Vocabulary • Corporation: An organization with the legal rights of a person and which many persons may own • Share of stock: Each unit of ownership in a corporation • Capital stock: Total shares of ownership in a corporation • Stockholder: An owner of one or more shares of a corporation Chapter 9

New Vocabulary • Special journal: A journal used to record only one kind of transaction • Cost of merchandise: The price a business pays for goods it purchases to sell • Markup: The amount added to the cost of merchandise to establish the selling price • Vendor: A business from which merchandise is purchased or supplies are others assets are bought Chapter 9

New Vocabulary • Purchase on account: A transaction in which the merchandise purchased is to be paid for later • Purchases Journal: A special journal used to record only purchases of merchandise on account • Special amount column: a Journal amount column headed with an account title • Purchase invoice: An invoice used as a source document for recording a purchase on account transaction Chapter 9

PURCHASING MERCHANDISE page 236 Chapter 9

PURCHASES ON ACCOUNT page 236 Chapter 9

PURCHASES JOURNAL page 237 Chapter 9

2 PURCHASE INVOICE page 238 1 4 3 1. Stamp the date received andpurchase invoice number. 3. Initials of the person whochecked the invoice. 2. Place a check mark by each amount. 4. Review the vendor’s terms. Chapter 9

PURCHASING MERCHANDISE ON ACCOUNT page 239 November 2. Purchased merchandise on account from Crown Distributing, $2,039.00. Purchase Invoice No. 83. 2 1 3 4 Chapter 9

1 6 TOTALING AND RULING A PURCHASES JOURNAL page 240 4 5 3 2 Chapter 9

Audit Your Understanding What kinds of transactions are recorded in a purchases journal? • Purchases of merchandise on account For what are special amount columns in a journal used? • Frequently occurring transactions Why are there two account titles in the amount column of the purchases journal? • Because the same two accounts are always affected by purchase on account transactions What is the advantage of having special amount columns in a journal? • Time is saved because it eliminates writing the account title Chapter 9

Work Together & OYO • P. 241 Chapter 9

LESSON 9-2 Journalizing Cash Payments Using a Cash Payments Journal

CASH PAYMENTS JOURNAL page 242 Cash Payments Journal: A special journal used to record only cash payment transactions Chapter 9

1 2 3 4 5 CASH PAYMENT OF AN EXPENSE page 243 November 2. Paid cash for advertising, $150.00. Check No. 292. Chapter 9

BUYING SUPPLIES FOR CASH page 243 November 5. Paid cash for office supplies, $94.00. Check No. 293. Chapter 9

CASH PAYMENTS FOR PURCHASES page 244 November 7. Purchased merchandise for cash, $600.00. Check No. 301. Chapter 9

New Vocabulary • Cash Discount: A deduction that a vendor allows on the invoice amount to encourage prompt payment • Purchases Discount: A cash discount on purchases taken for paying early • General amount column: A journal amount column not headed with an account title Chapter 9

New Vocabulary • List price: The retail price listed in the catalog or on an Internet site • Trade discount: A reduction in the list price granted to customers • Contra account: An account that reduces a related account on a financial statement Chapter 9

CASH PAYMENTS ON ACCOUNT WITH PURCHASES DISCOUNTS page 245 November 8. Paid cash on account to Gulf Craft Supply, $488.04, covering Purchase Invoice No. 82 for $498.00, less 2% discount, $9.96. Check No. 302. Chapter 9

CASH PAYMENTS ON ACCOUNT WITH NO PURCHASES DISCOUNTS page 246 November 13. Paid cash on account to American Paint, $2,650.00, covering Purchase Invoice No. 77. Check No. 303. Chapter 9

Audit Your Understanding Why would a vendor offer a cash discount to a customer? • To encourage early payment What is recorded in the general amount columns of the cash payments journal? • Cash payment transactions that do not occur often Chapter 9

Audit Your Understanding What is the difference between purchasing merchandise and buying supplies? • A business purchases merchandise to sell but buys supplies for use in the business. Supplies are not intended for sale. What is meant by the terms of sale 2/10, n/30? • Two ten means that 2% of the invoice amount may be deducted if the invoice is paid within 10 days of the invoice date. Net 30 means the total invoiced amount must be paid within 30 days. Chapter 9

Work Together & OYO • P. 247 Chapter 9

LESSON 9-3 Performing Additional Cash Payments Journal Operations

New Vocabulary • Cash short: A petty cash on hand amount that is less than the recorded amount • Cash over: A petty cash on hand amount that is more than a recorded amount • Cash Short and Over Account Chapter 9

1 3 4 5 6 7 PETTY CASH REPORT page 248 1. Write the date and custodian name. 2. Write the fund total. 3. Summarize petty cash payments. 2 4. Calculate and write the total payments. 5. Calculate and write the recorded amount on hand. 8 6. Write the actual amount of cash on hand. 7. Subtract the actual amount on hand from the recorded amount on hand and write the amount. 8. Write the total of the replenish amount. Chapter 9

REPLENISHING A PETTY CASH FUND page 249 1. Date 2. Account titles 3. Check number 4. Expense amounts 5. Cash short as a debit; cash over as a credit 6. Total cash payment 4 5 6 1 3 2 Chapter 9

TOTALING, PROVING, AND RULING A CASH PAYMENTS JOURNAL PAGE TO CARRY TOTALS FORWARD page 250 Chapter 9

STARTING A NEW CASH PAYMENTS JOURNAL PAGE page 251 Chapter 9

TOTALING, PROVING, AND RULING A CASH PAYMENTS JOURNAL AT THE END OF A MONTH page 252 Chapter 9

Audit Your Understanding When journalizing a cash payment to replenish petty cash, what is entered in the account title column of the cash payments journal? • The titles of the account for which the petty cash fund was used. Example: Supplies, Misc. Expense, etc. What is the usual balance of the account cash short and over? • The balance is usually a debit because the petty cash fund is more likely to be short than over Chapter 9

Work Together & OYO • P. 253 Chapter 9

LESSON 9-4 Journalizing Other Transactions Using a General Journal

New Vocabulary • Purchases returned: Credit allowed for the purchase price of returned merchandise, resulting in a decrease in the customer’s accounts payable • Purchases allowance: Credit allowed for part of the purchase price of merchandise that is not returned, resulting in a decrease in the customer’s accounts payable • Debit memorandum: A form prepared by the customer showing the price deduction taken by the customer for returns and allowances Chapter 9

MEMORANDUM FOR BUYING SUPPLIES ON ACCOUNT page 254 Chapter 9

BUYING SUPPLIES ON ACCOUNT page 255 November 6. Bought store supplies on account from Gulf Craft Supply, $210.00. Memorandum No. 52. Chapter 9

DEBIT MEMORANDUM FOR PURCHASES RETURNS AND ALLOWANCES page 256 Chapter 9

JOURNALIZING PURCHASES RETURNS AND ALLOWANCES page 257 November 28. Returned merchandise to Crown Distributing, $252.00, covering Purchase Invoice No. 80. Debit Memorandum No. 78. Chapter 9

Audit Your Understanding What journal is used to record transactions that cannot be recorded in special journals? • General journal Why is a memorandum used as the source document when supplies are bought on account? • To specify that the invoice is for store supplies and not for purchases, ensuring that no mistake is made when journalizing the transaction. Chapter 9

Work Together & OYO • P. 258 Chapter 9

Today’s Chuckle • Mr. and Mrs. Fenton are retired, and Mrs. Fenton insists her husband go with her to Wal-Mart. He gets so bored with all the shopping trips. He prefers to get in and get out, but Mrs. Fenton loves to browse. One day Mrs. Fenton gets this letter from Wal-Mart: Chapter 9

Dear Mrs. Fenton,Over the past six months, your husband has been causing quite a commotion in our store. We cannot tolerate this behavior and may ban both of you from our stores. We have documented all incidents on our video surveillance equipment. The complaints against Mr. Fenton are listed below: • Things Mr. Bill Fenton has done while his spouse was shopping in Wal-Mart: Chapter 9

June 15: Took 24 boxes of condoms and randomly put them in people's cart when they weren't looking. • July 2: Set all the alarm clocks in House wares to go off at 5-minute intervals. • July 7: Made a trail of tomato juice on the floor leading to the ladies rest rooms. • July 19: Walked up to an employee and told her, in an official tone, 'Code 3' in house wares. . . . . and watched what happened. Chapter 9

August 4: Went to the Service Desk and asked to put a bag of M&M's on layaway. • September 14: Moved a 'CAUTION - WET FLOOR' sign to a carpeted area. • September 15: Set up a tent in the camping department and told other shoppers he'd invite them in if they'll bring pillows from the bedding department. • September 23: When a clerk asks if they can help him, he begins to cry and asks, 'Why can't you people just leave me alone?' • October 4: Looked right into the security camera; used it as a mirror, and picked his nose. Chapter 9

November 10: While handling guns in the hunting department, asked the clerk if he knows where the antidepressants are. • December 3: Darted around the store suspiciously loudly humming the "Mission Impossible" theme. • December 6: In the auto department, practiced his "Madonna look" using different size funnels. • December 18: Hid in a clothing rack and when people browse through, yelled "PICK ME!" "PICK ME!" Chapter 9

December 21: When an announcement came over the loud speaker, he assumes the fetal position and screams "NO! NO! It's those voices again!!!!" • And last, but not least—December 23: Went into a fitting room, shut the door, waited awhile, and then yelled very loudly, "There is no toilet paper in here!" Chapter 9

The End Chapter 9