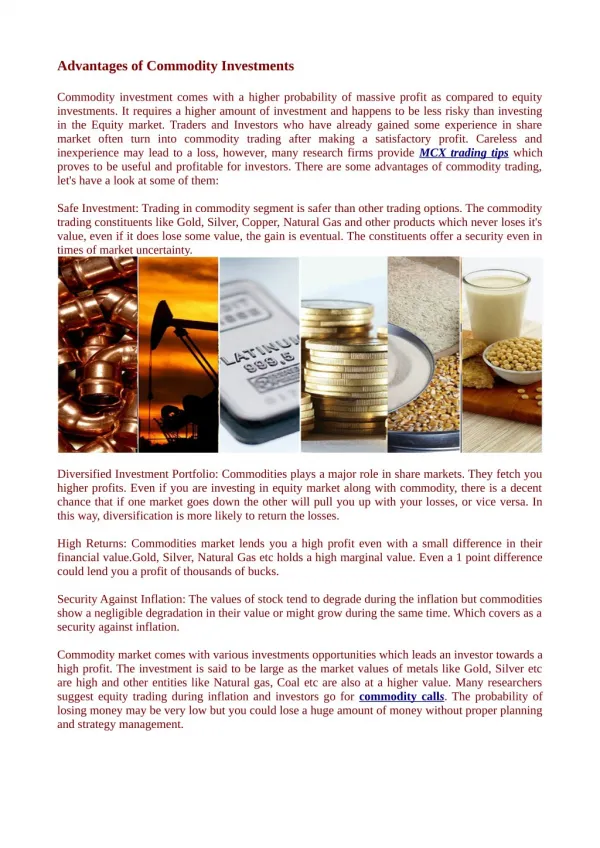

COMMODITY REVIEW

COMMODITY REVIEW. MECHANICAL PARTS PAUL SHELDON. Mechanical Components (P. Sheldon). SCORE CARD FY 06. Mechanical Components (P. Sheldon). STRONG PRESENCE OF SUPPLIERS IN E. EUROPE FY06 ACTION: ‘WESTERNIZE BUSINESS HABITS OF MAIN EE BASE’ REVERSE AUCTIONS PRICES:

COMMODITY REVIEW

E N D

Presentation Transcript

COMMODITY REVIEW MECHANICAL PARTS PAUL SHELDON

Mechanical Components (P. Sheldon) SCORE CARD FY 06

Mechanical Components (P. Sheldon) • STRONG PRESENCE OF SUPPLIERS IN E. EUROPE • FY06 ACTION: ‘WESTERNIZE BUSINESS HABITS OF MAIN EE BASE’ • REVERSE AUCTIONS • PRICES: • CLOSER FOLLOW UP of price vs raw materials • PRODUCTIVITY: especially machined parts (R. Bédard) • ACTION IN MACHINING S/CONTRACTING: as opposed to machined parts inc material • ROTC • LEAN: but most suppliers of Olomouc are already lean… • DPO • IMPACT OF ASIA SUPPLIERS MAINLY IN Q3 & Q4 • Volume deliveries of machined castings & stamped parts. • Difficulty in tracking savings automatically

REVERSE AUCTIONS • REVERSE AUCTIONS • €467k Plastic components (feb 05): €42k savings (RO/F) DONE. €32k (RO: tooling AR done) + €17k (F: transfer in progress) • €113k machined Bronze casting (oct 05): €10k savings (F). Unsuccessful. • €120k Aluminium (dec 05): €20k (HO: 1st tool transfer of 4 done) • €150k. Machining (Jan 06): €5k (CZ) DONE. €20k (CZ) Almost done (first samples delivered, refused. New samples end June) • €202k Bar machining: €12k (F) done, approved. €19k in progress (1st approval refused). 2 other lots didn’t work. • €615k Cast iron (Feb 06): €156k (RO & CZ) in progess, AR done. • €150k Cast iron (Avril 06): €35k (HO & CZ) in progess, AR done. • €220k Cast iron (May 06): €60k (RO, BG, HO, CZ): decision to be made. • €150k Cast iron (June 06): released • €120k Machined parts (July 06): to be done

PRICING • ACTIONS ENGAGED IN Q1 / Q2 on existing base • Scrape back some of high price hikes of FY05 in Q1 & Q2 • TES (€71k), Trie Château (€27k), Koopron (€25k), PBS (€8k) • Productivity in machining • ZLKL: 3% to 5% on targeted parts • PRICE TENSION SINCE JAN 06: Low profile / defensive position adopted in Q3 & Q4 • Energy costs up 8% to 27% depending on the country • Raw material prices go up again • Many EE mechanical companies back in a ‘production economy’: • At full capacity, they ‘clean up’ their portfolios • Big price rises asked for on small volume (5% to 20%)

KEY OBJECTIVE FY 06: CASH FLOW • DPO improvement: • Targetting of suppliers between 0 & 45 days • High sales • Targetting criteria (tailor to the situation): • Group or family company? • Take account of customer portfolio of the suppliers (esp direct competitors of LS) • Do not create fragile situation at good suppliers’ (eg. family companies) • Talk it over with them & listen: cash flow isn’t managed the same way in small companies • Target suppliers with increasing sales (esp with LS) • Agree to go ther step by step: • Don’t add extension of DPO to big price reduction requests • Get E. European suppliers used to participating in our ROTC improvement effort

IMPACT OF ASIA • Big savings from FY05 auctions in stampings & cast –iron • Only kicks in in Q3 & Q4 • Stamping savings clearly identified in inflation tracking • Castings not so easy: raw + machined in Europe, but supplied finished (mchined) from Asia • Manual tracking necessary • Example of Alternator division (castings) • Manual tracking necessary • Top 6 castings in sales value = €3000k raw + €1600k machining = €4600k • €700k savings in FY06 unidentified automatically (Asia) • €320k savings identified automatically, piece / piece rough castings (LCC / VLCC EE) • New castings introduced in mid FY05 (global alternator design) • €150k savings in FY06 (Q3 & Q4): VLCC EE (Uk, BG, RO)

MECHANICAL PARTS ANALYSIS BY COMPONENT FAMILY

PUS FY 06 / FY 07 • TARGET INFLATION FY 07 : -2 % • MARKET TREND: risks & opportunities • Steel prices fluctuate less, but remain high • Castings index similar • New machines cost same price in LCCs as in West • Energy prices continue to rise much faster than inflation: moderate prce hike requests of FY06 (+0 to 2%) could be higher in FY07 • LS in market trend toward purchasing more added value (eg. Machined castings) • China attractive for high volumes • A few EE companies invest in more modern machinery, but the majority have too much (old) capacity • EE & China have different supply bases: • China is organised between mechanical / foundries & machining companies • EE is not

PUS FY 06 / FY 07 • STRATEGY & ACTION PLAN • Share our markets between EE & China via separate auctions if possible • Keep an eye on $/€ rates • Enlarge strategy to subcon machining (same supplier base) • Reduce number of suppliers by consolidation • Wisconsin CZ (€400k), UNEKO (€300k) & ISH (€250k) not strategic: consolidate in existing & VLCC base • Continue toward more added value in purchase • Casting suppliers pre-informed of machining requirement • Enlarge machining base / partnerships with foundries to create market for future auctions • Replace Tafonco (major price rise in FY06)

PMO FY 06 / FY 07 • TARGET INFLATION FY 07 : -3 % • MARKET TREND: risks & opportunities • CZ still pretty saturated: several foundries closed in 05 & 06 • Casting material prices remain high (autumn/winter 04 level) • No raw material shortage today, but we remain vigilant • CZ, SK, RO: currency revaluation 8% to 10% in 2005. • ‘Unhealthy’ EE suppliers have cash problems • W. Europe staggered price rises in 05 & 06: 3-5% in 05, 1-5% in 06 • EE imposed almost full impact in 05, moderation in 06 • 0% - 3% inflation from Asia

PMO FY 06 / FY 07 • STRATEGY & ACTION PLAN • New supplier base in VLCC (Romania, Bulgaria, Ukraine) • Capacity suppliers in Central Europe (Croatia) to help CZ short term • Auctions of high volume parts : • Do not mix EE & China in auctions: EE not mature / competitive. Strategic share of markets. • Always include tooling in auctions: 25% - 50% savings possible • Take care with Asia in FY07: direct RFQ with newly developed suppliers gives same prices in FY06 for (machined) castings as in FY05 • Not sure to get this containment on open market / auctions (+10% to 15% mat’l price rise since then) • Auction potential limited in FY07: • Top 5 parts all auctioned / double auctioned in last 18 months • 24 month contracts preferred • Reduce number of suppliers in W Europe: target 2 or 3 strategic foundries • Be opportunistic when raw material costs drop • Be close to CZ / Olomouc = big volume buys of LS • Seek partners capable of machining (even if not yet ready) • Problems with low volume parts: pruning by EE foundries

PMA FY 06 / FY 07 • TARGET INFLATION FY 07 : -2 % (w/o aluminium variation) • MARKET TREND: risks & opportunities • Fast & furious Aluminium price increase early 2006. Dec 05 to March 06 +40%. Impact: • Pressure: + 20% (raw 50%) • LP gravity: + 12% (raw 30%) • sand: + 8% (raw 20%) • Expect severe carry over in FY07 (lagged price rises on past 3 months) • So far, impact Q3/Q2 = 7%

PMA FY 06 / FY 07 STRATEGY & ACTION PLAN Replace Diace by LCC supplier • Auction dec 05: first tooling transferred Increase coquilla volume in Romania Find new sources in LCC/VLCC in 3 types of aluminium castings: Romania, Bulgaria, Turkey Auctions if enough volume (but LS not so attractive) Investigate Dourlet: hard to put in auction - single, critical customer - value analysis - engineering / purchasing approach

PLA FY 06 / FY 07 • TARGET INFLATION FY 07 : -5% • MARKET TREND: risks & opportunities • Increase in materials linked to petroleum: +5% to +10% • Price tension on finished components +2% to + 6% • LS had reasonable price increase with Schulman in Jan 06 (8% on ABS = +1.7% total from Schulman) • Several W European component mfrs have moved to EE • CZ, SK, RO: revaluation of currency 8% to 10% 05/06 • No problem finding capacity on plastics market • Price reductions possible if ready to change suppliers

PLA FY 06 / FY 07 • STRATEGY & ACTION PLAN • Develop 1 or 2 sources in E Europe • SK, RO, HO….. • Several sources identified • Build on good savings following FY05 auction: new sources in Romania • Reduce number of suppliers in LS factories • Plan new auctions if volume permits: good markets for auctions • Use auctions for tooling: 35% to 50% savings in March 05 • Continue working group to find available raw materails for RM auctions • Big problem in FY06: captive market too large (ULs)

PDE FY 06 / FY 07 • TARGET INFLATION FY 07 : -5% • MARKET TREND: risks & opportunities • Price of steel remains high • Temporary shortage in 05 but OK in 06 / 07 • Cold rolled (+40%) & hot rolled (+50%) in 05/04: same level today • % Raw material in finished product now at much higher levels • W. European companies coming back into the game on volume markets: • Well equipped: productivity • Sometimes competitive vs EE (eg. New account TCIN)

PDE FY 06 / FY 07 • STRATEGY & ACTION PLAN • Continue to contain price rise requests in EE: suppliers passed on 70% of raw increase in 05 • Use Asian pressure from previous auctions • Price savings • Helps in containment elsewhere • Think twice before doing new auctions in Asia • Big material inflation since 05 auctions… • Find new suppliers in VLCC for high volume: RO, BG, UK? • Logistic costs an issue • Target newly approved LCC suppliers for medium volume: eg. Hundec Hungary • prices –20% to –40% depending on factories (DEI, IMI, GP) • Subsidiary of French company: already has logistic circuit to France • €200k account in FY07 / 08?

KPI / PDE FY 05 FY 06 FY 07 Spend in K€ 3,010 K€ 4,461 K€ 4,237 K€ Net Material Inflation 4.2% -1.0% -5.0% LCCS (%) 51.0% 60.0% e-Sourcing K€ (M) Bid 660 K€ 0 K€ 250 K€ average Results -40.0% -20.0% Direct Material DPO Total Averge Days 73 Days 72 Days 72 Days K€ less than 30 days 1,361 K€ 13 K€ 100 K€

![[Commodity Name] Commodity Strategy](https://cdn3.slideserve.com/6088618/commodity-name-commodity-strategy-dt.jpg)