Download

1 / 30

310 likes | 728 Views

JOB ORDER COSTING. General Objective : To understand and apply the methods of costing and JOC Specific objectives : I. Explain the various methods of costing 2. Define job order costing correctly.

E N D

JOB ORDER COSTING General Objective : To understand and apply the methods of costing and JOC Specific objectives : I. Explain the various methods of costing 2. Define job order costing correctly.

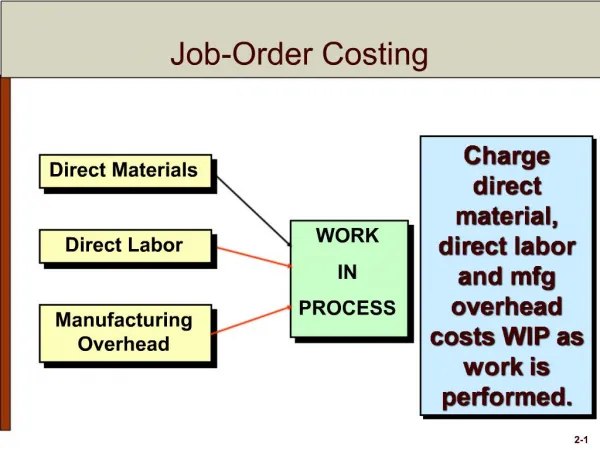

Definition of JOC • This method is used when work is done according to customer’s order. Each job is often of a short duration. • Work must be planned and scheduled because there is no predetermine pattern of work. • This method are popular among enterprises that are engaged in house building, Ships-building, Machinery production and repair. * In Job Costing all cost of directly charge to the specific job of the product.

Characteristics of JOC Job order costing is known by different names such as specific order or production order. Unit cost is computed by dividing total manufacturing costs per job order by the number of good units produced. Cost of a units can be a job order, an individual unit or even a batch of a product. Job cost sheets can be used to control efficiency and estimate future work. Each job cost sheets have a number of the job.

JOB ORDER COSTING Learning Outcome : 1.To explain the procedure of cost accumulation under job order costing. 2. To determine unit cost from the total cost.

What is Job Cost Sheet ? CHANTIQUE FURNITURE JOB ORDER COST SHEET Customer Name :________________Date : _____________ Job Order No : _______ Product Description: __________________________ Selling Price : ________ Total Cost : __________ Cost per Unit: ________

Example 1 : Chantique Furniture manufacturers many products. Each product passes through 2 production dept, which have the following cost structure : Dept A Dept B Normal monthly volume 5,000 DLH 10,000 DLH Budgeted Overhead RM 25,000 RM 60,000 Below was the job went through the factory last month, JobA001: Direct Materials RM 2,400 Direct Labour : Dept A (180 hrs) RM 1,620 Dept B (60 hrs) RM 420 Output 600 units Calculate : i. Total cost ii. Unit cost

Solution : a). Direct materials RM 2,400 Direct Labour : Dept A RM 1,620 Dept B RM 420 Overhead : Dept A (RM5/dlh x 180hrs) RM 900 Dept B (RM6/dlh x 60 hrs) RM 360 Total Cost RM 5,700 b). Unit cost = RM 5,700 = RM 9.50 600 unit Notes : How did the overhead figure derived ??

Example 2 : MEGAH SDN BHD is an office furniture’s manufacturer . It is the company policy to charge factory overhead based on direct labour hour in Dept A and machine hour in Dept B. Dept A Dept B Normal direct labour hour 5,000 DLH 10,000 DLH Normal machine hour 3,000 hrs 6,000 hrs Budgeted Overhead RM 25,000 RM 60,000 Below was the job went through the factory last month, JobA002: Direct Materials RM 2,400 Direct Labour : Dept A (180 hrs) RM 1,620 Dept B (60 hrs) RM 420 Machine hour : Dept A 120 hrs Dept B 100 hrs Output 600 units Calculate : i. Total cost ii. Unit cost

Solution : a). Direct materials RM 2,400 Direct Labour : Dept A RM 1,620 Dept B RM 420 Overhead : Dept A (RM5/dlh x 180hrs) RM 900 Dept B (RM10/dlh x 100 hrs) RM 1,000 Total Cost RM 6,340 b). Unit cost = RM 6,340 = RM 10.57 600 unit Notes : How did the overhead figure derived ??

Exercise 1 : Below are the information regarding an order from a customer for Pure Inside Manufacturing Co.Ltd : Budgeted cost: Direct Labour Hour Variable Overhead Dept. A 20,000 @ RM 3.25 RM 70,000 Dept. B 18,000 @ RM 3.10 RM 45,000 Dept. C 10,000 @ RM 3.00 RM 20,000 Cost information for a specific job, JOB008: Raw material bought RM 216 Raw materials issued from store RM 270 Labour – Dept. A 80 h - Dept . B 40 h - Dept. C 30 h Delivery Cost RM 60 Administration cost is 10 % from manufacturing cost. Profit margin is15 %. Prepare a quotation for that customer.

Exercise 2 : Kayabaga Ltd is alloy product manufacturer in Ipoh. The business gave a bad reflection of profit and you are instructed to investigate this situation. You have found that a quotation with RM 1,350 for Job A223 have these following cost information : Raw material RM 456 Labour – Dept. X ( 10 h x RM9) 90 - Dept . Y ( 4 h x RM7.50) 30 - Dept. Z ( 15 h x RM9.60) 144 264 Total Cost RM ?? Profit margin is25 %. Selling price ???

Administration & selling overhead is based on 50% of primary cost . Your investigation also found out these cost information : Budgeted direct labour cost and manufacturing overhead for that 3 departments are as follows : Department DL(RM) Overhead (RM) X 390,000 429,000 Y 480,000 240,000 X 300,000 450,000 Required : Recalculate the cost for JObA223 and what is the most suitable price to quote ?

Exercise 3 : Indah Furniture is a company producing quality kitchen cabinet in Semambu. Overhead was absorbed based on machine hour in Design Department and other department were based on direct labour hour. The company policy is to absorb 20% of manufacturing cost as administration & sales overhead. Below are the budgeted data for current year : (RM’000) Design Dept Painting Dept Furnishing Dept Total Raw materials RM2,850 RM150 RM29 RM3,029 DLH (‘000hour) 30 120 23 173 Machine Hour(‘000h) 100 40 - 140 Wages/hour RM4.00 RM 3.25 RM 3.00 Production OH RM200 RM300 RM92 RM592 Admin&Selling OH - - - RM1,050

An order was received from a client for 30 units of kitchen cabinet. The expected cost was accumulated in order to prepare the quotation as follows : Profit margin is 20% of selling price. Required : Calculate production cost for each department Calculate quotation price, and profit from the order

Ledger Cost • To accumulate the cost using ledger cost • Example 1 : Maya Engineering using job ordercosting to accumulate the cost for its product. Below are some data regarding a job : Extract of job cost sheet :

Below were data received from financial department: • Opening stock of raw material RM9,200 • All jobs were finished and invoiced to clients. • Selling & distribution OH were charged based on 10% of cost of finished goods. Based on the information, prepare ledger cost and profit & loss a/c

Exercise 1 : • Indah Ltd had 3 jobs in Jan. Cost related tp that 3jobs are as follows :

Budgeted OH for the year is RM50,000 and budgeted DLH is 25,000 h. Overhead absorbed based on DLH. Actual OH for Jan is RM4,000. • Wages /hour is RM1.00. • Only Job A1 had finished and sent to customer with Selling price of RM7,000. • Prepare: • a. Job cost card for Job A1,A2 and A3 • b. WIP Control A/c and OH Control A/c • c. Profit and Loss

Let’s check the answer : • a.Job Cost Card Don’t forget to show the calculation for OH cost…