Download

1 / 11

110 likes | 286 Views

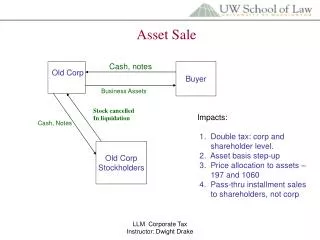

Asset Sale. Cash, notes. Old Corp. Buyer. Business Assets. Stock cancelled In liquidation. Impacts: 1. Double tax: corp and shareholder level. 2. Asset basis step-up 3. Price allocation to assets – 197 and 1060 4. Pass-thru installment sales

E N D

Asset Sale Cash, notes Old Corp Buyer Business Assets Stock cancelled In liquidation Impacts: 1. Double tax: corp and shareholder level. 2. Asset basis step-up 3. Price allocation to assets – 197 and 1060 4. Pass-thru installment sales to shareholders, not corp Cash, Notes Old Corp Stockholders LLM Corporate Tax Instructor: Dwight Drake

Purchase Price Allocations – 197, 1060 197 Anti “Soft Dollar” Rule: All intangible assets amortized over 15 years – information bases, customer lists, patient files, know-how, licenses, franchises, trade names, goodwill, going-concern value, covenants not to compete. 1060 Priority Asset Allocation Rules: Priority One: Cash or cash equivalents. Priority Two: Highly-liquid securities, foreign currencies and CDs. Priority Three: ARs, mortgages, credit card receivables. Priority Four: Inventory and dealer property Priority Five: Other tangible assets (equipment, real estate, etc.) Priority Six: Intangibles except goodwill and going concern value. Priority Seven: Goodwill and going concern value. Note: Parties can agree on values per agreement, but not change priorities. LLM Corporate Tax Instructor: Dwight Drake

Stock Sale Old Corp Buyer 338 Election? Cash, notes Impacts: 1. Shareholder level tax. 2. No asset basis step-up w/o 338 3. 338 gives step-up at huge cost 4. If 338, same allocation issues as asset sale 5. Installment reporting OK at shareholder level. Stock Old Corp Stockholders LLM Corporate Tax Instructor: Dwight Drake

338 Election Concept: Buyer of 80% of more of stock of target corporation over 12 month period can elect to treat as asset purchase. Basis step-up, all new corp attributes, and now corporate level tax. Killer: Demise of general utility doctrine gutted any value of 338 election in most cases. Why take tax hit now to get future benefit of basis step-up? Two Survivors: 338 still works where: - Corp has big NOL can than shelter corporate level tax triggered on deemed asset sale. - Stock of sub is sold and gain on sub stock is more than gain on sub assets. Then, 338(h)(10) election, coupled with 332 and 337, may produce win-win – step-up with lower tax to parent corp. Bottom Line: Demise of General Utilities triggers double tax on nearly all asset sales and stock sales with 338 election. Hence, structure of choice now in most cases is straight stock sale with no 338 election. LLM Corporate Tax Instructor: Dwight Drake

Problem 385 T Corp balance sheet – is a C Corp. A.B. FMV Cash 200k 200k Liabilities 300k Inventory 50k 100k Equip 100k 200k A Stock (50k basis) 500k Building 50k 300k B Stock (40k basis) 400k Securities 400k 300k C Stock (140k basis) 100k Goodwill 0 200k Total 800k 1,300k 1,300k (a) T adopts liquidation plan, sells all assets except cash (subject to debt) to P for 800k cash and then liquidates. T Corp income and loss: LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (a) Continued - Inventory 50k ordinary income - Equipment 100k 1245 ordinary income - Building 250k 1231 gain - Securities (100k) LTCL - Goodwill 200k LTCG Total 500k income Tax to corp 175k (35% of 500k). Balance of assets less 300k liabilities (net 825k) to shareholders, who would have collective gain LTCG of 825k less 230k basis. For A, gain would be 362.5k (412.5k less 50k basis), which at 15% triggers tax of 54.375k. LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (b) T liquidates, all assets to shareholders pro rata, followed by asset sale to P. T Corp ordinary income 150k (inventory 50k and equip 1245 of 100k) and LTCG of 350k (250k building, 200k goodwill less 100k securities). Tax to corp 175k (35% of 500k). Balance of 1,125k assets less 300k liabilities (net 825k) to shareholders, who would have collective gain LTCG of 825k less 230k basis. For A, gain would be 362.5k (412.5k less 50k basis), which at 15% triggers tax of 54.375k. Results same as in (a) at both corporate and shareholder level. (c) Same as (a) but P pays 200k cash and gives 600k note, market rate payable annually, principal due in 5 yrs. Cash and note distributed to shareholders. T Corp recognizes all 500k gain now because distributes note to shareholder – thus no 453 available to T Corp. C has loss, so not concerned with 453. A & B may each use 453 treatment on full note, even inventory portion because part of bulk sale. 453(h)(1)(B). LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (d) T sells all assets to P as in (b) - $1 mill cash – but does not liquidate and instead invests in stock portfolio. T still have 500k taxable gain and 175k tax. E & P increased by 325k (excess of 500k gain over 175k tax) to 725k. T would become personal holding company, subject to penalty tax if not distribute investment earnings. Only possible justification is desired 1014 stock basis step-up on death of shareholder to eliminate 331 gain on future liquidation. LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (e) P purchases T stock from shareholders for 800k (800 per share) and makes 338 election. - Shareholder capital gain based on 800k paid: 400k to A (50k LTCG); 320k to B (280k LTCG); 80k to C (60k LTCL). - Since “qualified stock purchase” under 338 (one-shot 100% stock purchase), 338 election is deemed sale of assets from T to P. Formula for amount of purchase (“aggregate deemed sales price” or ADSP) is: ADSP = Grossed up stock price + T liabilities + [tax rate x (ADSP – T’s tax basis in deemed assets sold)] ADSP = 800k + 300k + [.35 (ADSP – 800k)] ADSP = 1,261,538. (Roughly 800k for stock, 300k liabilities and 175k tax burden in (a)). - T must report gain on deemed asset sale on final return and pay tax. ADSP allocated to assets in new corp – first to non-goodwill up to FMV and balance to goodwill. P reduces price because it bears tax hit on deemed sale. LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (f) P purchases T stock for cash, no 338 election. How much to pay? Price will be discounted for present value of lost tax benefits due to low basis carryover. Negotiated somewhere between $1 mill and 800k. (g) If P and T indifferent, which best: Straight asset purchase? Stock with 338 election? Stock without 338 election? Best deal stock without 338 election because no corporate level tax now. Non-tax factors may be big deal. (h) What impact is 600k NOL in T? NOL could shelter corporate tax on sale of assets or 338 election. Thus, step-up basis possible with no corporate level tax now. Good use of NOLs because may be otherwise limited due to 382 limitations on carryover of NOLs with change of ownership. (i) T wholly-owned sub of S Inc., which has 200k basis in T stock. All T assets (subject to debt) distributed to S, who sells to P. Liquidation tax free to T and S under 332 and 337. S takes T basis in assets per 334(b) and potential gain on T stock held by S is eliminated. On sale of assets, S picks up 500k income (150 ordinary and 350 capital). P takes new 1012 cost basis. Identical result if T first sold assets, then liquidated. LLM Corporate Tax Instructor: Dwight Drake

Problem 385 (j) Same as (i) but P insists transaction be structured as acquisition of T stock from S Inc. Per 338(h)(10), T and S (members of consolidated group) may treat as sale of assets, not sale of stock. This will always be advantage if gain on asset sale less than stock sale, due to basis differences or NOL. Result is P gets stepped-up basis and T and S pay less tax. Lesson: 338 usually only works where big NOL or parent-sub situation exists and gain in sub assets less than gain in sub stock held by parent. LLM Corporate Tax Instructor: Dwight Drake