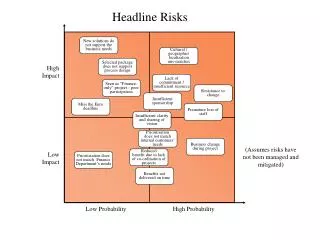

Risks within China

180 likes | 490 Views

Risks within China Lecturer: Zhigang Li Motivation Common Risks: Economic growth is not a smooth process. The uncertainty of economic growth could affect long-term growth rates. What have been underlying the uncertainty of China’s growth? How will they change in the future?

Risks within China

E N D

Presentation Transcript

Risks within China Lecturer: Zhigang Li

Motivation • Common Risks: Economic growth is not a smooth process. The uncertainty of economic growth could affect long-term growth rates. • What have been underlying the uncertainty of China’s growth? • How will they change in the future? • Idiosyncratic risks: Even if the economy is stable, risks may exist in many dimensions that may affect the investment and consumption activities of individuals or firms. • Health risk • Default risks • What could be done to reduce the risks?

Outline • Common risks and growth • Theory • Evidence from the world • Evidence for China • Idiosyncratic risks within China • Evidence for China

Risks Total risks = common risks + idiosyncratic risks

How could risk be measured? • A typical proxy of risk is the realized volatility (or variance) of economic time series • More sophisticated measurement of risk can be inferred using GARCH models and Stochastic Volatility models.

Theory: How could risks affect economic growth? • Neoclassical growth model (Solow, 1956) • Volatility plays no role for growth • Real business cycle (RBC) models (e.g. Kydland and Prescott, 1982) • The volatility of shocks to the economy may affect the level of growth (but not the growth rates of technology)

Theory: How could risk affect economic growth? • Francois and Lloyd-Ellis (2003): Growth and business cycles can be positively linked via creative destruction. • Wen and wang (2006): Because of imperfect competition, firms charge higher prices during periods of larger volatility. Higher markup leads to lower capacity utilization and lower rate of return to capital. • Exchange rate risks could decrease investment and growth (e.g. Aghion et al.). • Inflation uncertainty could also affect growth. • Irriversibility of investments: When investments are irreversible, idiosyncratic investment risks could reduce firms’ investments (Jamet, 2004).

Evidence: How could risks affect economic growth? • Lucas (1987) • Welfare gains of eliminating fluctuations are trivial compared to that of stimulating long-run growth • Ramey and Ramey (1995) • Countries with higher output volatility tend to have lower output growth. • Wang and Wen (2006) • Further stabilizing the U.S. economy can increase welfare by 25% of annual consumption. stabilizing output growth (or capacity utilization) around a potential target.

Exchange Rate Uncertainty • Aghion, Bacchetta, Ranciere and Rogoff • For countries with relatively low levels of financial development, exchange rate volatility generally reduces growth, whereas for financially advanced countries, there is no significant effect. • A 50 percent increase in volatility uncertainty leads to a 0.33 percent reduction in exchange rate volatility.

Common risks of China • Fluctuation due to policy changes • Exchange rate risks • Inflation risks • Efficiency of (physical) capital market (reducing the irreversibility of investments) • Risks of external markets

Sources of idiosyncratic risks within China • Political connection • Political connection disrupts price information in the market • The market for political power is inefficient itself • Presentation by Chunyuan Shi • Contract risk (property rights) • Presentation by Yitian Li • Structural change of economic environment • Presentation by Xiaomeng Li • Health • Poor coverage of commercial health insurance and low quality of health service in rural China

How could risk be reduced? • Economic development itself could actually reduce the effect of political connections • Reduced effect of political forces • Market integration (presentation by Fan Meng) • Government should be an important force • Help reduce exchange rate volatility • Public social insurance (presentation by Hao Liang) • Monitoring the financial sector (presentation by Yuanyuan Cao)

How are the different risks expected to change in the future? • Institutional environment • Policy making process • Contract enforcement • Property rights • Exchange rate scheme • Inflation uncertainty • Globalization • The development of financial market • Social security net

Frankel (2008) • What has the de facto exchange rate regime of China been since 2005? • By mid-2007, the RMB basket had switched a substantial part of the dollar's weight onto the euro. Frankel, Jeffrey A. New Estimation of China's Exchange Rate Regime. 2009, National Bureau of Economic Research, Inc, NBER Working Papers: 14700.

Conditional volatilities of inflation and output for China (Narayan et al., 2009)

Thesmar and Thoenig, 2004 • Capital market development, by improving risk sharing between listed firms, increases the willingness of these firms to take risky bets. This in turn increases firm level uncertainty. • This effect could further diffuse to non-listed firms. • The spillover effect is larger when competition increases, and when labor market institutions are flexible. • Financial Market Development and the Rise in Firm Level UncertaintyPreview Thesmar, David; Thoenig, Mathias; 2004, C.E.P.R. Discussion Papers, CEPR Discussion Papers: 4761