Download

1 / 15

160 likes | 187 Views

Explore the EU's agricultural trade policy within a global context, focusing on CAP reforms, trade evolution, and objectives. Delve into the impact of reforms on exports, WTO position, bilateral agreements, and GIs protection. Understand how the reformed CAP promotes development-friendly practices and fosters international trade relations. Discover the EU's strategic objectives and the significance of FTAs in shaping future trade dynamics. Presented at the IFAJ Congress in Brussels on April 22, 2010.

E N D

The Common Agricultural Policy in a World Context Jerzy Plewa Deputy Director-General for International Affairs DG Agriculture and Rural Development European Commission

CAP in a World Context • Evolution of EU agricultural trade • Impact on trade of CAP reforms • Main objectives of EU agricultural trade policy • Multilateral, bilateral/bi-regional, unilateral

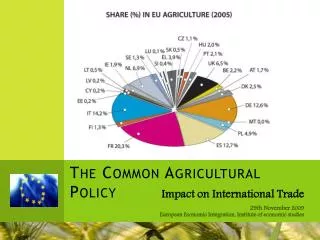

Evolution of EU • agricultural trade <<<< Import | Export >>>> Source: EUROSTAT - COMEXT IFAJ Congress – Brussels, 22 April 2010 3

Evolution of EU • agriculturaltrade EU27 US Brazil Source: EUROSTAT - COMEXT and Global Trade Information Services, Inc., GTA IFAJ Congress – Brussels, 22 April 2010 4

Evolution of EU • agriculturaltrade EU27 US Japan China

Impact on trade of CAP reforms Reductions in EU price support, bringing EU prices in line with world prices Source: European Commission – DG AGRI IFAJ Congress – Brussels, 22 April 2010 6

Export refunds, bn € and % of agricultural expenditure and exports 35% 12,0 30% 10,0 25% 8,0 20% % EAGGF and exports Bn EUR 6,0 15% 4,0 10% 2,0 5% 0% 0,0 1992 1993 1994 1995 1996 1997 1998 1999 2000 2001 2002 2003 2004 2005 2006 2007 2008 2009 EU-12 up to 1994 EU-15 up to 2004 EU-25 up to 2006, then EU-27 Refunds Refunds/exports Refunds/expenditure pillar1 Impact on trade of CAP reforms IFAJ Congress – Brussels, 22 April 2010 7

Domestic support - WTO boxes (bn €) Impact on trade of CAP reforms IFAJ Congress – Brussels, 22 April 2010 8

Main objectives of EU agricultural trade policy IFAJ Congress – Brussels, 22 April 2010 9

WTO Doha Round - the EU position Thanks to the CAP reforms, the EU has been in a position to support a high level of ambition in the DDA: on market access: at least 54% ofaverage tariff cuts; on domestic support: 80% reduction of OTDS (Overall Trade-Distorting Support); on export subsidies: 100% elimination of subsidies and other forms of export support by 2013. 10 IFAJ Congress – Brussels, 22 April 2010

Bilateral agreements (including GIs) Norway Canada Canada CH Ukraine Azerbajan CH Moldova W. Balkans Armenia Georgia USA EUROMED Korea GCC Mexico Cariforum China India ACP/EPAs ASEAN CA Concluded CAN Mercosur Ongoing Australia Chile SA Future 49% of EU agricultural exports 70% of EU agricultural imports IFAJ Congress – Brussels, 22 April 2010

Main objectives of GIs agreements Protect as many EU GIs as possible in Partners’ territories Achieve a high level of protection for EU GIs in Partners’ territories Solve difficult cases: conflicting generic use conflicting TMs IFAJ Congress – Brussels, 22 April 2010 12

Reformed CAP- “Development Friendly” • EU - largest market for developing countries (value of the EU agricultural import from DCs > 50 billion EURO (more than US, JAP, CAN, AUS and NZ together) • DFQF access to the EU market (EBA, EPA, GSP+) • Export refunds and trade distortion supports substantially reduced • EU supports to the regional integration of DCs IFAJ Congress – Brussels, 22 April 2010 13

Conclusions • The EU remains the leading agricultural trader in the world; • EU exports are essentially processed high value-added products; in imports final products also dominate but commodities and intermediates play important role; • High quality is the main feature and the future of our products in the global market; • Reformed CAP- more trade and development – friendly; • Strategic objectives: DDA remains a priority, but FTAs (and GI agreements)become increasingly important. IFAJ Congress – Brussels, 22 April 2010 14

Thank you for your attention! IFAJ Congress – Brussels, 22 April 2010 15