Download

1 / 4

40 likes | 171 Views

Takaful is a Sharia compliant form of insurance that has been around in its modern form for over 25 years now. It is an Islamic alternative to the commercial insurance and is often seen as the ‘ethical insurance option’.

E N D

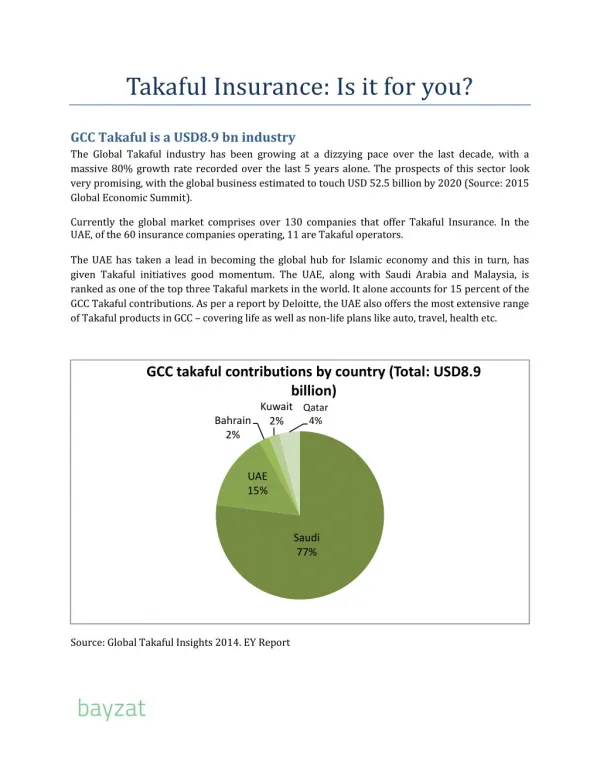

Takaful Insurance: Is it for you? GCC Takaful is a USD8.9 bn industry The Global Takaful industry has been growing at a dizzying pace over the last decade, with a massive 80% growth rate recorded over the last 5 years alone. The prospects of this sector look very promising, with the global business estimated to touch USD 52.5 billion by 2020 (Source: 2015 Global Economic Summit). Currently the global market comprises over 130 companies that offer Takaful Insurance. In the UAE, of the 60 insurance companies operating, 11 are Takaful operators. The UAE has taken a lead in becoming the global hub for Islamic economy and this in turn, has given Takaful initiatives good momentum. The UAE, along with Saudi Arabia and Malaysia, is ranked as one of the top three Takaful markets in the world. It alone accounts for 15 percent of the GCC Takaful contributions. As per a report by Deloitte, the UAE also offers the most extensive range of Takaful products in GCC – covering life as well as non-life plans like auto, travel, health etc. GCC takaful contributions by country (Total: USD8.9 billion) Kuwait 2% Qatar 4% Bahrain 2% UAE 15% Saudi 77% Source: Global Takaful Insights 2014. EY Report

A Primer on Takaful Takaful is a Sharia compliant form of insurance that has been around in its modern form for over 25 years now. It is an Islamic alternative to the commercial insurance and is often seen as the ‘ethical insurance option’. According to Islamic beliefs, commercial insurance is forbidden as it encompasses prohibited elements such as interest, uncertainty and gambling. The term Takaful comes from the Arabic verb ‘kafalah’, which means to help one another, or mutual guarantee. This health insurance offering is designed around concepts of cooperative responsibility, shared guarantee, collective assurance and the notion of mutual undertaking. Contrary to the conventional insurance where once you pay an annual premium, the monetary risk is transferred from the insured to the insurer; in Takaful the risk of insurance is mutually shared by the group of participants. Each participant makes a contributionto a fund, and in the event of loss the affected participant will receive the amount of claim. Mudarabah and Wakala are most popular There are two main Takaful insurance models that are common in the GCC – the Mudarabah model and theWakala model. In Saudi Arabia, companies operate under the Mudarabah model which entitles the Takaful operator to charge a fixed percentage of profit made in the year and all operatingexpenses are borne by the operator from the shareholder fund. Whereas in the UAE the Wakala model is adopted,according to which the Takaful operator just gets an agency fee that is deducted from the contribution pool.

Takaful Versus Conventional Insurance Advantages of Takaful The main value proposition is that Takaful is inherently ethical, which implies that all the money from the insurance pool has to be invested in ethical products. Moreover, Islamic insurance is free from interest and is based on a profit sharing financing technique. In case of surplus in the Takaful fund at the end of the year, the money is divided and given back to the policy holders. Hence it offers you an ethical investment-cum-insurance option with significant profit making potential and price competiveness. It is emerging as a compelling business proposition for Muslims and non-Muslims alike.

Drawbacks The greatest drawback is the lack of standardization in the industry. There are a lot of regional discrepancies in Takaful insurance plans like definition of acceptable risks, insured events and exclusions. This can be primarily attributed to regional specific differences in Shariah interpretations. For example, in more conservative countries, the insurance does not include cover for suicide, AIDS, unmarried pregnancy etc. This is a big concern for policy holders. Summary The Takaful insurance sector is still in its nascent stages with very low market share as compared to conventional insurance. According to a Special Report (2016) by A. M. Best, the level of Takaful penetration (ratio of Takaful contributions to overall insurance revenue) for Middle East is a meager 8%,with the UAE having the lowest penetration rate in the region (6%). Hence, this rapidly evolving sector is still untapped and has great growth potential. The UAE Takaful industry is continuously striving to improve outreach, extend the product lines and improve regulations to facilitate its growth. To explore the Takaful Insurance option and to evaluate if it suits your individual needs, download the Bayzat app. Bayzat gives you an insightful and holistic comparison of the available Takaful options, empowering you to make an informed decision.