Download

1 / 15

150 likes | 294 Views

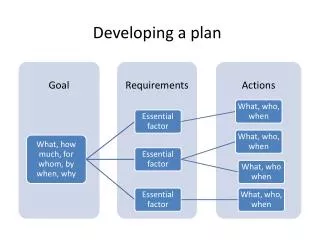

Developing A Plan: Preliminary Inputs To The Investment Program. February 2006 CSMFO Annual Conference Kay Chandler, CFA. Establish Policy Objectives, Constraints. Evaluate Plan and Execution, Changes. Identify Strategies, Benchmarks. Execute the Plan.

E N D

Developing A Plan:PreliminaryInputs To The Investment Program February 2006 CSMFO Annual Conference Kay Chandler, CFA

Establish Policy Objectives, Constraints Evaluate Plan and Execution, Changes Identify Strategies, Benchmarks Execute the Plan The Cycle of Portfolio Management

Establish Policy Objectives, Constraints Evaluate Plan and Execution, Changes Identify Strategies, Benchmarks Execute the Plan Objectives + Constraints = Policy

Establishing Objectives • Safety—maintain appropriate level of exposure to risk • Liquidity • Sufficient short-term investments • Marketable securities • Targeted maturities • Extra layer • Yield (Return,Growth) • Income • Long-term growth

Safety: The Relationship Between Risk and Return Market Risk

Safety: The Relationship Between Risk and Return Market Risk Higher Duration Portfolios Have Greater Volatility of Return

Treasuries are the safest, considered to have ZERO credit risk Federal agency securities considered next safest AAA and AA A No credit research necessary Monitor agency news, rating agency actions Understand the business—risks and opportunities; monitor news and rating agency watch lists With greater diligence--understand the business—risks and opportunities; monitor news and rating agency watch lists. Be quick to act on credit changes Safety: Assuming Credit Risk Can Improve Returns …When resources are available to monitor credit quality appropriately.

Liquidity: Having cash when you need it. • Liquidity risk (I) 1. The risk that the portfolio won’t provide adequate cashflow for the agency • Match maturities to known cash needs • Prepare cash flow forecasts • LAIF • Readily marketable securities • Extra layer of short-term investments

Liquidity: Having cash when you need it. • Liquidity risk (II) 2. The risk that a security is not readily marketable, that is, can’t be sold, if necessary, at a good price • Often measured by the difference between the price at which you can buy (offer or ask) and the price at which you can sell (bid) • Treasuries, large agency issues, large corporate issues are most liquid • Small issue sizes, securities with unusual features, are least liquid

Establish Policy Objectives, Constraints Evaluate Plan and Execution, Change Identify Strategies, Benchmarks Execute the Plan Yield: DevelopingInvestment Strategies

Liquidity Component Meets specific liquidity needs Invests in short-term securities Average maturity short Very low volatility Cash flow matching LAIF Growth Component Targeted to highest suitable duration Longer-term securities Normally not used for liquidity, but invested in highly marketable securities, in case Greater volatility Total Portfolio Growth Liquidity Yield Strategy: Two components for Liquidity and Growth

Passive Management • Buy and Hold • Money is invested when it is available to a date when cash is needed. • There is no further activity with that investment, except for reinvestment of income • Maturity Ladder • Funds are invested in equal amounts to staggered maturity dates • When securities reach maturity, the funds are reinvested into the longest permitted maturity

Active Portfolio Management • Creating and maintaining a portfolio structure with acceptable exposure to risk. • Striving to achieve a “better” return using one or more of the following strategies: • Duration management • Yield curve placement • Sector weighting decisions • Individual security selection • Timing • Relative to a chosen market benchmark, or to some other comparative measure

Resource for Public Fund Investing in California CALIFORNIA PUBLIC FUND INVESTMENT PRIMER Published by the State Treasurer California Debt and Investment Advisory Commission http://www.treasurer.ca.gov/cdiac/invest/primer.pdf

Establish Policy Objectives, Constraints Evaluate Plan and Execution, Change Identify Strategies, Benchmarks Execute the Plan On to Plan Execution and Evaluation