Download

1 / 29

290 likes | 326 Views

Visit https://simplehai.axisdirect.in/ for more information.

E N D

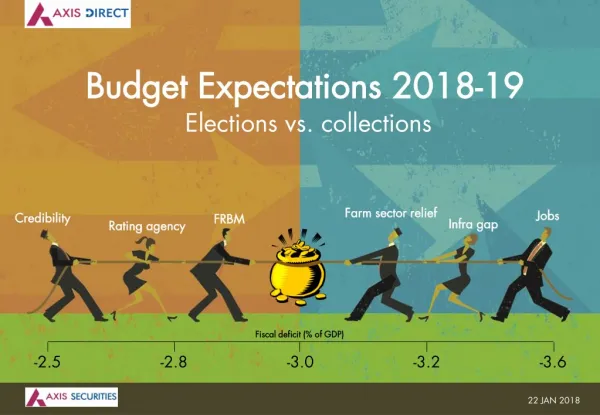

Budget Budget Expectations 2018 Expectations 2018- -19 Elections vs. collections 19 Farm sector relief Farm sector relief Jobs Jobs Credibility Credibility FRBM FRBM Infra gap Infra gap Rating agency Rating agency Fiscal deficit (% of GDP) Fiscal deficit (% of GDP) -2.5 -2.8 -3.0 -3.2 -3.6 22 JAN 2018

22 JAN 2018 22 JAN 2018 Key things to watch for in this Budget Key things to watch for in this Budget BUDGET EXPECTATIONS 2018-19 The finance minister faces an interesting dilemma. The finance minister faces an interesting dilemma. The union government’s fiscal position can be judged to be in fantastic health purely based on taxes collected but the fact is not all of these taxes accrue to the Center !! So the finance minister will have to decide how to present the truth! The IGST conundrum The IGST conundrum: The Center’s tax growth is primarily from IGST. Purists will argue that only half of IGST accrues to the Center and only that must be considered. Fiscal practitioners could argue that IGST is like a holding account and that there would be a base level of taxes in transit at all times. Some level of IGST could be a permanent feature in the union government’s float. We think a middle ground would be shown. We think a middle ground would be shown. What will the FM present: What will the FM present: The budget will show a miss in FY18; 3.4% of GDP fiscal deficit instead of 3.2% target and below 3.5% achieved in FY17. FY19 is likely to be pegged at 3.2% of GDP (same as FY18 target). Revenue: Revenue: Non-tax receipts like spectrum, RBI dividend and divestment would be scaled back slightly. Tax collections to improve on growth and greater compliance on GST. Optimistic tax buoyancy at 1.3 to account for scale back in non-tax targets. Expenditure Expenditure: Subsidy will rise due to food (expansion of price deficit MSP), interest (affordable housing) and fuel (oil @ 65) offsetting benefits from DBT in fertilizers. Capex allocation will see greater thrust on irrigation, rural roads and rural housing. Beneficiaries: (A) Beneficiaries: (A) Rural focus: Cement, FMCG and infra; (B) (C) (C) Corporate tax cut: FMCG, retail. (B) Affordable housing push: Banks, Cement, Realty; Losers: Losers: All insurance companies – If corporate tax rationalization leads to higher tax rate for insurance companies who are currently paying 15%. 2

22 JAN 2018 22 JAN 2018 Sectoral expectations: Summary… Sectoral expectations: Summary… BUDGET EXPECTATIONS 2018-19 Sector Sector Key budget expectations Key budget expectations Impact Impact Financial incentive to replace vehicles older than 10/15 years Long-term measures for agri sector to push farmer productivity/ income levels up Higher JNNURM orders for bus manufacturers and incentives for EVs Little impact Positive: Positive: CV OEMs, Hero, M&M, Maruti Autos Autos Positive Positive ♦ Housing finance companies to benefit from increased demand for affordable housing ♦ Recapitalization to aid large PSU banks with growth capital ♦ Merger of PSU banks to benefit PSU banks under PCA Final blueprint and roadmap of mega recap plan to fund PSU banks Roadmap on merger plan of weak PSU banks Support for ‘Housing for All’ by 2022 Separate tax exemption for term life insurance Increased tax on life insurance companies, bringing it in line with current corporate tax rate Banking and Financial Banking and Financial Services Services 3

22 JAN 2018 22 JAN 2018 …Sectoral expectations: Summary… …Sectoral expectations: Summary… BUDGET EXPECTATIONS 2018-19 Sector Sector Key budget expectations Key budget expectations Impact Impact Positive: Positive: L&T, Dilip Buildcon, Sadbhav, ABB, Siemens, VA Tech and EPC players Capital Capital goods and goods and Infrastructure Infrastructure Higher budgetary allocation towards roads, railways, metro, defense and urban infra (AMRUT) projects ♦ Positive Positive: Industry would benefit from better volume growth Thrust on reviving rural economy through various incentives and higher infra spending Cement Cement ♦ Corporate tax – Positive for ITC, HUL, GSK Cons, Nestle and Colgate ♦ Rural stimulus – Positive HUVR, Dabur, Emami, CLGT and JYL ♦ Customs duty – Positive jewellery companies Positive Outlining of reduction in corporate tax rate from 30% to 25% will benefit full tax paying companies Increased stimulus for rural India in the form of higher allocation to MNREGA and other rural employment initiatives Some relief to the jewellery industry in terms of lower custom duty on gold import (custom duty was increased from 2% to 10% in 2012-13) Positive for FMCG & Retail FMCG & Retail Positive for 4

22 JAN 2018 22 JAN 2018 …Sectoral …Sectoral expectations: expectations: Summary… Summary… BUDGET EXPECTATIONS 2018-19 Sector Sector Key budget expectations Key budget expectations Impact Impact ♦ Positive Positive for Hindalco and Vedanta ♦ Positive Positive for domestic steel producers Import duty on Aluminum to increase to10% from 7.5% Customs duty on coking coal to cut down to nil from 2.5% Metals Metals Cut in cess rate for E&P companies (20% ad valorem currently) Inclusion of natural gas in GST (20-25% tax currently) ♦ Positive Positive: for upstream cos. ♦ Positive Positive: for CGD, GAIL, GSPL, PLNG ♦ Positive Positive for CGD cos. Oil & Gas Oil & Gas Exemption in excise duty for CNG used for natural gas vehicles ♦ Extend R&D sunset clause (150% deduction on R&D) beyond 2020 ♦ Match GST refund rates to previous excise duty refund rates (20-25% lower currently) ♦ Implement proposed reduction in corporate tax rates to 25% in a phased manner for all domestic companies irrespective of turnover/ profit (currently limited to smaller companies) ♦ Positive Positive for companies incurring high R&D expenses ♦ Positive Positive for domestic manufacturers Pharma Pharma 5

22 JAN 2018 22 JAN 2018 …Sectoral expectations: …Sectoral expectations: Summary… Summary… BUDGET EXPECTATIONS 2018-19 Sector Sector Key budget expectations Key budget expectations Impact Impact Positive Positive for all gencos and discoms, as it will reduce cost of power and boost overall power demand Uptick in Power T&D expenditure Inclusion of electricity under GST Down-scaling of clean energy cess Power Power Positive: Positive: For all developers focused on affordable segment. Incentives to REITs positive for annuity players Expanding beneficiaries of Pradhan Mantri Awas Yojana (PMAY) Further tax rationalization in REITs Increase deduction limit on housing interest and principal on housing loan Realty Realty Reduction in customs duty on equipment for timely roll-out of networks Relaxing withholding tax on distributors’ margin on SIM cards and prepaid vouchers Lowering GST on telecom services Neutral Neutral for all telecom service providers. Any cut in custom duty could be positive positive Telecom Telecom 6

Macro backdrop of the budget Macro backdrop of the budget

22 JAN 2018 22 JAN 2018 The concerns that need to be addressed The concerns that need to be addressed BUDGET EXPECTATIONS 2018-19 I Investment rate continues to languish nvestment rate continues to languish Consumer sentiment is souring on employment outlook Consumer sentiment is souring on employment outlook Consumer confidence (1Yr ahead eco expectations) Real PFCE growth (Discretionary itens only*, RHS) GFCF/GDP 40% 60 15 (Net response) 35% (%YoY) 12 40 30% 9 20 6 25% 26.4% 0 3 20% -20 0 May-12 May-13 May-14 May-15 May-16 May-17 Sep-11 Sep-12 Sep-13 Sep-14 Sep-15 Sep-16 Sep-17 Jan-12 Jan-13 Jan-14 Jan-15 Jan-16 Jan-17 Mar-11 Mar-12 Mar-13 Mar-14 Mar-15 Mar-16 Mar-17 Source: CEIC, Axis Capital Source: Source: RBI consumer sentiment survey covering 5000 HHs in 6 metros. India is not outperforming on world trade growth India is not outperforming on world trade growth Farm sector realizations have crashed barring a few vegetables Farm sector realizations have crashed barring a few vegetables 30 Rural wage growth (avg. for Men & Women) (%YoY) 80 India exports (value) World Trade (Value) (YoY%) Food inflation 25 60 Correl = 84% 20 15 40 10 6.4 20 5 0 0 -20 -5 May-13 May-14 May-15 May-16 May-17 Nov-12 Nov-13 Nov-14 Nov-15 Nov-16 Nov-17 -40 00 01 02 03 04 05 06 07 08 09 10 11 12 13 14 15 16 17 *We remove non-discretionary items within private consumption like food & fuel to derive discretionary personal final consumption expenditure (PFCE) 8

22 JAN 2018 22 JAN 2018 Key expectations from the budget this year Key expectations from the budget this year BUDGET EXPECTATIONS 2018-19 For FY18: For FY18: Decide between managing the optics using IGST collections or use 0.5% of GDP buffer space available under N.K.Singh’s FRBM recommendations Fiscal stance Fiscal stance For FY19: For FY19: Stick to the glide path to shore up credibility or alter the glide path to show realistic picture ♦ Lower de facto corporate tax as per glide path ♦ More graded income tax slabs ♦ Scale back asset sales target ♦ Assume modest RBI dividend ♦ Optimistic tax buoyancy assumption Revenue Revenue measures measures ♦ Push for affordable housing through intervention in land market and relaxing eligibility criteria for credit subsidy ♦ Higher capex spending in roads (+18%), irrigation, food supply chain and housing ♦ Tax incentive for buyers of stressed assets Revival of Revival of growth growth ♦ Savings from using DBT to be offset by food and interest subsidy ♦ Given no large incidentals like 7 pay commission, can go slow on revenue expenditure growth and bump up in capex Expenditure Expenditure measures measures ♦ Use of DBT in all subsidy schemes ♦ Rework and implement price-deficit MSP system ♦ Set-up challenge model for allocation of resources to states rather than allocation based on politics ♦ Incentivize defense R&D among MSMEs Reforms Reforms 9 Source: Axis Capital

22 JAN 2018 22 JAN 2018 The IGST conundrum The IGST conundrum BUDGET EXPECTATIONS 2018-19 (Rs (Rs bn) bn) April April- -November November FY17 FY17 9,333 % y % y- -o o- -y y FY18 FY18 10,873 April-Nov indirect tax collection growth is 19% y-o-y, but if we take only 50% of IGST collected, then indirect tax collection run rate falls to 5.5%, which is still better than 4% budget target. Gross tax collected by center 17 ow Direct -Corporate -Income 14 12 15 4,089 2,223 1,867 4,650 2,498 2,152 IGST is an interim account. When a good is finally consumed, the IGST so collected gets equally distributed between CGST and SGST. If the good is exported, then rebates are claimed. ow Indirect -CGST -UTGST -IGST -GST comp cess -Customs -Excise -Service -Others 19 5,243 - - - - 1,485 2,136 1,468 154 6,223 854 1 1,383 309 1,028 1,652 791 204 (31) (23) (46) 32 In the meantime, the center is showing IGST under its books. Given that there would be a base level of IGST at all times, the center could consider showing a little more than half of IGST in its year ending accounts. NCCF (LESS) Assignment to states (LESS) (39) 25 43 26 3,078 - 6,212 8,290 14,502 3,853 - 6,994 9,467 16,461 Even without IGST, states are seeing budget beating tax growth. This data includes taxes from stamp duty. Net tax available to center Tax revenue of states (27 #s) Total tax (Center + State) 13 14 14 Our FY18 fiscal deficit estimates assumes 4% y Our FY18 fiscal deficit estimates assumes 4% y- -o o- -y growth in indirect taxes; so the FM has some leeway to show y growth in indirect taxes; so the FM has some leeway to show fiscal achievement . For FY19, we are more optimistic with 15% indirect tax projection. fiscal achievement . For FY19, we are more optimistic with 15% indirect tax projection. 10 Source: CEIC, Axis Capital

22 JAN 2018 22 JAN 2018 RBI dividend RBI dividend BUDGET EXPECTATIONS 2018-19 RBI profits dipped by INR 352 RBI profits dipped by INR 352 bn bn RBI net injection ( RBI net injection (- -) /absorption (+) ) /absorption (+) Net repo MSS Surplus transferd to the government (LHS) % of gross income less expenditure (RHS) 8 (Rs trn) 700 100 6 (%) (Rs bn) 600 80 4 -352bn 500 60 2 400 300 40 0 200 20 (2) 100 May-17 Jul-17 Mar-17 Sep-17 Feb-17 Oct-16 Oct-17 Dec-16 Dec-17 Jan-17 Jan-18 Jun-17 Apr-17 Nov-16 Nov-17 Aug-17 0 0 2012-13 2013-14 2014-15 2015-16 2016-17 Source: CEIC, Axis Capital Source: RBI RBI profits dropped in FY17 mostly due to excess liquidity in banking system (post demonetization) which the RBI had to absorb by taking deposits at reverse repo rate. The RBI’s dividends to the government therefore suffered. The banking system has been in surplus through FY18, so dividends expectations from the RBI and even the BFSI segment would have to be scaled back. In FY19, tax projections will be scaled up but non In FY19, tax projections will be scaled up but non- -tax collections would be scaled back tax collections would be scaled back 11

22 JAN 2018 22 JAN 2018 PSU recapitalization PSU recapitalization – – details to be provided in the budget details to be provided in the budget BUDGET EXPECTATIONS 2018-19 The impact on fiscal is marginal if The impact on fiscal is marginal if recap outside the balance sheet outside the balance sheet 2 Yr bank recapitalizaton plan 2 Yr bank recapitalizaton plan recap bonds are kept bonds are kept However, public debt figures will rise before taking the path However, public debt figures will rise before taking the path prescribed by prescribed by N.K.Singh’s N.K.Singh’s FRBM recommendation FRBM recommendation (Rs bn) (Rs bn) % of GDP % of GDP Public debt to GDP ratio (in %) Public debt to GDP ratio (in %) From budget 180 0.1% 70% 68% 67%68% Banks capital raising 580 0.3% Recapitalization bonds 1,350 0.8% 65% Total Total 2,110 2,110 1.3% 1.3% 60% Estimated interest cost 101 0.1% 55% FY20t FY21t FY22t FY24t FY25t FY18E FY19E FY23t FY12 FY14 FY15 FY16 FY17 FY13 Source: Axis Capital Source: CEIC, Axis Capital In 2015, PSU banks were busy supporting financial inclusion (Jan Dhan); in 2016, they were busy making provisions (AQR) and supporting demonetization; in 2017, it was all about resolving NPAs. 2018 is likely to show genuine signs of moving towards better health as banks begin to taste resolution on NPA assets and recapitalize with the help of the government and sanguine capital market conditions. Path to 60% public debt to GDP will be delayed by bank recapitalization Path to 60% public debt to GDP will be delayed by bank recapitalization 12

22 JAN 2018 22 JAN 2018 Rural push Rural push – – only a few levers available that can give quick results only a few levers available that can give quick results BUDGET EXPECTATIONS 2018-19 Rural push Rural push - - assessment of policy levers assessment of policy levers In terms of actionable rural stimulus plans, the central government has only a few levers in its control. The problem problem that that the the government government needs address address this this time time is is fall realization realization; for this, increasing credit availability or investment in marketing infrastructure would not help. A direct intervention into the market like increasing MSP procurement is the only way to get quick results. To criticism for procuring and letting the food rot in poor storage units, we think the government can incentivize setting up of ‘soup kitchens’ Canteen in Tamil Nadu and more recently Indira Canteen in Karnataka, which has the added addressing the urban poor. High The key needs to to farm sector sector key Interest subsidy Credit to agri Interest waiver fall in in farm Price deficit MSP Implementable Implementable Loan waivers and raising shield itself from Expand procurement Rural infrastrucutre like Amma Low High Addresses current issue Addresses current issue benefit of Source: Axis Capital Rural push is likely to increase the food and interest subsidy bill Rural push is likely to increase the food and interest subsidy bill 13

22 JAN 2018 22 JAN 2018 Sticking to FRBM has its benefits Sticking to FRBM has its benefits BUDGET EXPECTATIONS 2018-19 Capital costs in the economy depend on fiscal credibility Capital costs in the economy depend on fiscal credibility Net market borrowing (Union Govt.) 10 Gec (RHS) The central government plays an important role in setting long-term funding costs in the economy 8 13 (% of GDP) (%) 6 11 Keeping long-term borrowing costs anchored helps the current deleveraging cycle and the nascent optimism on investment cycle upturn 4 9 2 7 0 5 Mar-00 Mar-01 Mar-02 Mar-03 Mar-05 Mar-06 Mar-08 Mar-09 Mar-11 Mar-12 Mar-14 Mar-15 Mar-17 Mar-04 Mar-07 Mar-10 Mar-13 Mar-16 Mar-18E Mar-19E Source: Axis Capital Borrowing costs in the economy would Borrowing costs in the economy would fall if fall if S&P S&P follows follows through on Moody’s through on Moody’s upgrade last upgrade last year year 14

22 JAN 2018 22 JAN 2018 Working assumptions for Working assumptions for FY19 FY19 budget budget BUDGET EXPECTATIONS 2018-19 (Rs bn) (Rs bn) FY18 BE FY18 BE FY18 (Axis) FY18 (Axis) FY19 (Axis) FY19 (Axis) % y-o-y % y-o-y Abs YoY Abs YoY Comments Comments Gross Tax Revenue Gross Tax Revenue 19,116 19,116 19,140 19,140 22,103 22,103 15 15 2,963 2,963 Tax bouyancy assumed at 1.3 Corporation tax 5,387 5,431 6,137 13 706 Maintain current run rate Income tax 4,413 4,020 4,824 20 804 Maintain current run rate Indirect tax 9,316 9,688 11,142 15 1,453 Improves on growth and measures to raise GST compliance Less: To States & Union Territories & NCCF Less: To States & Union Territories & NCCF 6,846 6,846 6,846 6,846 7,836 7,836 14 14 990 990 Net tax revenues Net tax revenues 12,270 12,270 12,294 12,294 14,267 14,267 16 16 1,973 1,973 Non tax revenues (incl dividend, interest, etc) 2,888 2,744 2,626 (4) (119) Low spectrum estimate and no RBI dividened boost Non-debt capital receipts (incl divestment) Revenue expenditure Revenue expenditure - ow Interest - ow Subsidies - ow Subsidies 844 994 670 (33) 7 7 (324) 1,307 1,307 170 128 128 Rs. 55k divestment figure Post 7th pay comission, there is some space to go slow Impact of bank recapitalization 18,369 18,369 5,231 2,635 2,635 18,669 18,669 5,231 2,707 2,707 19,976 19,976 5,401 2,835 2,835 3 5 5 Food 1,453 1,500 1,600 7 100 Fertilizer 700 700 680 (3) (20) Savings from DBT Petroleum 250 275 300 9 25 Crude oil price @ 65/bbl Crude oil price @ 65/bbl Interest 232 232 255 10 23 67mn individuals used the scheme in FY18, down from 74mn in FY14. Additional allocation can impact 2-5mn individuals - ow MGNREGA 480 480 550 15 70 Capital Expenditure Capital Expenditure 3,098 3,098 2,998 2,998 3,598 3,598 20 20 600 600 Mostly into rural housing, irrigation and urban infrastructure Total Expenditure Total Expenditure 21,467 21,467 21,667 21,667 23,574 23,574 9 9 1,906 1,906 Fiscal deficit (5,465) (5,635) (6,011) (376) Fiscal % of GDP Fiscal % of GDP (3.2) (3.2) (3.4) (3.4) (3.2) (3.2) Source: RBI, Axis Capital 15

22 JAN 2018 22 JAN 2018 Working assumptions for Working assumptions for FY19 general government financing FY19 general government financing BUDGET EXPECTATIONS 2018-19 Particulars Particulars Fiscal deficit (% of GDP) Fiscal deficit (% of GDP) Central Govt FY15 FY15 FY16 FY16 FY17 FY17 FY18BE FY18BE FY18RE FY18RE FY19E FY19E Comments Comments (4.1) (3.9) (3.5) (3.2) (3.4) (3.2) We see a strong chance that states will do better than budget in FY18. Tax collection for 27 states is collectively growing at 14% y-o-y (Apr-Nov) versus budget target of 12%. State Govt (2.6) (3.6) (3.0) (2.6) (2.6) (2.5) Total govt Fiscal deficit (INR bn) Fiscal deficit (INR bn) Central Govt State Govt Total govt Mkt. borrowing (INR bn) Mkt. borrowing (INR bn) Central Govt borrowings (6.7) (7.5) (6.5) (5.8) (5.9) (5.7) (5,108) (3,272) (8,380) (5,274) (4,934) (10,208) (5,351) (4,495) (9,846) (5,465) (4,310) (9,775) (5,635) (4,310) (9,945) (6,011) (4,688) (10,700) Total financing requirement 4,547 4,406 4,082 3,502 4,052 4,508 Improved states fiscal health could translate to lower borrowing next year State Govt borrowings 2,360 2,612 3,293 3,468 3,468 3,751 Total govt requirement Mkt. borrowing % a GDP Mkt. borrowing % a GDP 6,907 7,018 7,375 6,970 7,520 8,259 Central Govt borrowings State Govt borrowings Total govt requirement Sources of funding for market borrowing (INR bn) Sources of funding for market borrowing (INR bn) 3.7% 1.9% 5.6% 3.2% 1.9% 5.1% 2.7% 2.2% 4.9% 2.1% 2.1% 4.1% 2.4% 2.1% 4.5% 2.4% 2.0% 4.4% Banks Insurance Companies Financial Institutions (PDs, MF, PF, Corp+FIIs) Reserve Bank of India Total Funding gap (INR bn) Funding gap (INR bn) 1,887 2,750 2,634 2,412 2,451 2,679 3,029 3,332 Assumes 15% growth in FY18 and 10% in FY19 3,001 3,301 Assumes 12% growth in FY18 and 10% in FY19 Takes into account opening up of FII space in FY18 and 10% growth in FY19 (900) 7,130 8,833 1,946 2,099 1,891 2,000 2,200 5,881 7,806 8,304 (364) 505 1,099 Surplus/deficit (1,026) 788 928 (390) 574 16 Source: RBI, Axis Capital

Sectoral Sectoral expectations expectations

22 JAN 2018 22 JAN 2018 Auto Auto BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Vehicle modernization scheme - Financial incentive to replace vehicles over 10/15 years old Positive Positive for CV players CV players Farm income/ productivity - Long-term measures in agri sector to improve farmer productivity/ income levels Positive Positive for Tractor OEMs (M&M and Escorts) (M&M and Escorts) and OEM’s with higher rural dependence (Maruti and Hero) (Maruti and Hero) JNNURM orders (STU bus procurement program) - Increased allocation under the scheme for STU procurement of buses, and incentives for electric buses Positive Positive for Ashok Leyland Ashok Leyland (>45% market share in STU), and Tata Motors Tata Motors Largely positive, as always Largely positive, as always 18

22 JAN 2018 22 JAN 2018 Financials Financials BUDGET EXPECTATIONS 2018-19 Sector Sector Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Positive Positive – PSU banks (especially for large PSU banks like SBIN, BOB that require growth capital) Final blueprint on types of bonds or interest rates on these bonds; Specific roadmap of funding Capital allocation to PSU banks A mega recap plan of Rs 2.1 trn Banks Banks Associate banks of SBI and Bhartiya Mahila bank merged with SBI Roadmap on merger plan of weak PSU banks Positive Positive for PSU banks under PCA Merger of PSU banks Additional tax sops; Increase in ticket sizes/ current limits; Using of land bank of PSUs for affordable housing Positive Positive for housing finance lenders (Banks and HFCs) Housing for All by 2022 and affordable housing 4% subsidy on interest rate for home loans NBFC NBFC Creating a separate tax exemption for term life insurance Positive Positive for Life Insurance companies (SBI Life) Separate tax exemption for term life insurance Part of 80C with ceiling of Rs 0.15 mn Insurance Insurance Increase in tax rate on life insurance companies Raising it to bring it in line with corporate tax rate Negative Negative for all Life Insurance companies At ~15% currently 19

22 JAN 2018 22 JAN 2018 Capital Goods and Infrastructure… Capital Goods and Infrastructure… BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Road capex (urban + rural + NHAI) FY18 outlay on road at Rs 1.43 trn (up 10% YoY) boosted by MoRTH allocation To further increase by 20-25% in FY19 Positive Positive for EPC companies EPC companies with strong balance sheets with strong balance sheets Railway capex FY18 at Rs 1.31 trn (up 8% YoY) To further increase by 10-15% in FY19 Positive Positive for L&T, ABB, Siemens, L&T, ABB, Siemens, and other EPC companies Capital outlay for metro rail FY18 at Rs 180 bn (up 15% YoY) To further increase by 10-15% in FY19 Positive Positive for L&T, J Kumar, L&T, J Kumar, BEML, Siemens, Simplex BEML, Siemens, Simplex etc. Capital outlay on defense FY18 at Rs 887 bn (modest increase of 8% YoY) Modest growth of 5-10% in FY19 Positive Positive for BEL, Cochin BEL, Cochin Shipyard, L&T, Reliance Shipyard, L&T, Reliance Defence Defence Capex for urban Infrastructure Rs 196 bn in FY18, up 7% YoY To increase further by 15-20% in FY19 Positive Positive for ABB, Siemens, ABB, Siemens, VA Tech, Schneider VA Tech, Schneider etc. Higher capital outlays in infra positive for EPC companies Higher capital outlays in infra positive for EPC companies 20

22 JAN 2018 22 JAN 2018 …Capital Goods and Infrastructure …Capital Goods and Infrastructure BUDGET EXPECTATIONS 2018-19 Capex for key schemes Capex for key schemes Growth YoY (%) Growth YoY (%) (Rs bn) (Rs bn) FY15 FY15 FY16 FY16 FY17 RE FY17 RE FY18 BE FY18 BE FY18 FY18 FY19E FY19E Defence Capex 820 815 818 887 8 5-10 Railways 643 935 1,210 1,310 8 10-15 Metro (Under Min. of Urban Development) 61 93 157 180 15 10-15 Roads (MORTH) 274 469 524 649 24 20-25 Rural Roads (PMGSY) 142 183 190 190 0 20-30 Rural Housing Urban Infra Renewable Energy 111 43 20 101 77 40 160 183 39 230 196 50 44 7 27 30-40 15-20 20-30 Urban T&D (Int. Power Development Scheme) 6 10 45 58 29 15-20 Rural Electrification (DDUGJY) 34 45 34 48 43 20-30 Total budget allocation Total budget allocation 2,154 2,154 2,768 2,768 3,360 3,360 3,798 3,798 13 13 Growth (%) 9 29 21 13 Source: Budget documents, Axis Capital 21

22 JAN 2018 22 JAN 2018 Commodities Commodities BUDGET EXPECTATIONS 2018-19 Sector Sector Item Item Current status Current status Possible changes in Budget Possible changes in Budget Impact Impact Cement Cement Thrust on reviving rural economy by various incentives and higher infra spending NA Tax benefit/ interest rate concession to new projects and higher allocation for rural schemes/ loan waiver Positive Positive – industry to benefit from volume growth Metals Metals Import duty on Aluminum Current duty at 7.5% Increase it to 10% Positive Positive for Hindalco, Vedanta and NALCO Reduction in custom duty on coking coal Current custom duty at 2.5% Reduce it to nil Marginally positive Marginally positive for steel companies Higher allocation to housing/infra positive for cement Higher allocation to housing/infra positive for cement 22

22 JAN 2018 22 JAN 2018 FMCG and Retail FMCG and Retail BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Increased spending in rural As part of infrastructure development, central government along with state government runs various schemes. These initiatives are also focused on generating employment Expectation of a populist budget given general elections in 2019; increased budgetary allocation likely for rural India Positive Positive for rural-focused companies like Emami (50% of sales), Dabur (45% of sales), Bajaj Corp (42% of sales), Jyothy Lab (40% of sales), Colgate (38% of sales) and HUL (35% of sales) Corporate tax Tax rate of 30% (excluding cess) Outlining of reduction in corporate tax rate from 30% to 25% Positive Positive for high tax paying companies like ITC, HUL, Nestle, GSK Consumer, Colgate HUL, Nestle, GSK Consumer, Colgate ITC, Custom duty on gold import Current duty at 10% Jewellery association has demanded lowering the custom duty to 4-5% Positive Positive for all jewellery companies Positive for FMCG and Retail companies Positive for FMCG and Retail companies 23

22 JAN 2018 22 JAN 2018 Oil & Gas Oil & Gas BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Cut in cess rate for E&P companies E&P companies are required to pay cess at 20% of realized crude oil price Cut in cess rate to 5-8% of realized crude, as rise in crude pushed the cess up much beyond earlier fixed rate of Rs 4,500/t Positive Positive for ONGC, Oil India ONGC, Oil India and Cairn Cairn Inclusion of natural gas in GST Natural gas along with key petroleum products (petrol, diesel, jet fuel) and crude oil is not included in GST Natural gas inclusion in GST, possibly in the 5% slab in line with GST on coal Positive Positive for CGD GAIL, GSPL and PLNG, as GST inclusion makes natural gas competitive vs. other fuels (coal, petrol and diesel), pushing gas demand up CGD companies, Exemption in excise duty for CNG used for natural gas vehicles Compression of gas is viewed as “manufacturing” of goods and attracts excise duty of 14.4% Cut/ exemption in excise duty charged on CNG volumes of CITY GAS DISTRIBUTION (CGD) companies Neutral Neutral for CGD cut in excise will be passed on. However, lowering of retail gas price may boost consumption CGD companies as Promoting natural gas as principal fuel by giving tax benefits to CGD players; Promoting natural gas as principal fuel by giving tax benefits to CGD players; Petrol and diesel inclusion in GST may take more time, as it requires states’ consensus Petrol and diesel inclusion in GST may take more time, as it requires states’ consensus 24

22 JAN 2018 22 JAN 2018 Power Power BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Power T&D expenditure ~Rs 106 bn spent on such schemes in FY18 BE Increase by 20-25% Positive Positive for power gencos, as higher capex helps reduce T&D losses and, improve power demand by SEBs Include electricity in GST Not included Likely to be included Positive Positive for gencos and SEBs as it will reduce cost of power due to offset on input credit. This will also boost power demand in manufacturing sector (40% of power consumption) Clean energy cess Current cess at Rs 400/ton Down-scaling of the cess Positive Positive for gencos, as it would reduce cost of power 25

22 JAN 2018 22 JAN 2018 Real Estate Real Estate BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Extend provisions of section 80IBA (income tax exemption) to housing units up to 150 sqm carpet area (MIG category) Provisions of section 80IBA are applicable for affordable housing units up to 60 sqm carpet area for EWS and LIG Extend the benefit to MIG category, which is already covered in PMAY for mortgage interest subvention Positive: Positive: For all developers with mid-income housing projects REIT REIT: Reduce holding period for LTCG Holding period for LTCG is 36 months Reduction in holding period to 12 months Positive: Positive: For realty companies with strong annuity portfolios such as DLF, Phoenix Mills, DLF, Phoenix Mills, Prestige Estates Prestige Estates and Brigade Brigade REIT REIT: Exemption of stamp duty on transfer of assets into REIT Stamp duty is applicable while transferring assets into REIT One-time exemption while transferring assets into REIT will make it a more viable product for both developers and investors Positive Positive for realty companies with strong annuity portfolios such as DLF, Phoenix Mills, DLF, Phoenix Mills, Prestige Estates Prestige Estates and Oberoi Oberoi Realty Realty Higher tax deduction on home loans Rs 2,00,000 on interest and Rs 1,50,000 on principal To be increased further Positive: Positive: For all developers Focus to remain on Focus to remain on government’s vision of government’s vision of Housing Housing for for All All by by 2022 and REITs 2022 and REITs 26

22 JAN 2018 22 JAN 2018 Telecom Telecom BUDGET EXPECTATIONS 2018-19 Item Item Current status Current status Possible changes in budget Possible changes in budget Impact Impact Customs duty on equipment Currently at 29.8% Cut it below 25% Positive Positive for telecom service providers and infrastructure companies Relaxing withholding tax on distributors’ margin Currently at 10% Cut it down to 1% Positive Positive for telecom service providers Lowering GST on services Currently at 18% Reduce it to 12% Positive Positive for telecom service providers 27

Disclaimer Disclosures Disclosures: : The following Disclosures are being made in compliance with the SEBI Research Analyst Regulations 2014 (herein after referred to as the Regulations). 1. Axis Securities Ltd. (ASL) is a SEBI Registered Research Analyst having registration no. INH000000297. ASL, the Research Entity (RE) as defined in the Regulations, is engaged in the business of providing Stock broking services, Depository participant services & distribution of various financial products. ASL is a subsidiary company of Axis Bank Ltd. Axis Bank Ltd. is a listed public company and one of India’s largest private sector bank and has its various subsidiaries engaged in businesses of Asset management, NBFC, Merchant Banking, Trusteeship, Venture Capital, Stock Broking, the details in respect of which are available on www.axisbank.com. 2. ASL is registered with the Securities & Exchange Board of India (SEBI) for its stock broking & Depository participant business activities and with the Association of Mutual Funds of India (AMFI) for distribution of financial products and also registered with IRDA as a corporate agent for insurance business activity. 3. ASL has no material adverse disciplinary history as on the date of publication of this report. 4. I/We, author/s (Research Team) and the name/s subscribed to this report, hereby certify that all of the views expressed in this research report accurately reflect my/our views about the subject issuer(s) or securities. I/We (Research Analyst) also certify that no part of my/our compensation was, is, or will be directly or indirectly related to the specific recommendation(s) or view(s) in this report. I/we or my/our relative or ASL does not have any financial interest in the subject company. Also I/we or my/our relative or ASL or its Associates may have beneficial ownership of 1% or more in the subject company at the end of the month immediately preceding the date of publication of the Research Report. Since associates of ASL are engaged in various financial service businesses, they might have financial interests or beneficial ownership in various companies including the subject company/companies mentioned in this report. I/we or my/our relative or ASL or its associate does not have any material conflict of interest. I/we have not served as director / officer, etc. in the subject company. E E- -mail mail Sr. No Sr. No Name Name Designation Designation 1 2 3 4 5 6 7 Sunil Shah Pankaj Bobade Suvarna Joshi Siji Philip Hiren Trivedi Kiran Gawle Rohit Chawla Head of Research Research Analyst Research Analyst Research Analyst Research Associate Associate Research Associate sunil.shah@axissecurities.in pankaj.bobade@axissecurities.in suvarna.joshi@axissecurities.in Siji.philip@@axissecurities.in hiren.trivedi@axissecurities.in kiran.gawle@axissecurities.in rohit.chawla@axissecurities.in 5. ASL has not received any compensation from the subject company in the past twelve months. ASL has not been engaged in market making activity for the subject company. 6. In the last 12-month period ending on the last day of the month immediately preceding the date of publication of this research report, ASL or any of its associates may have: i. Received compensation for investment banking, merchant banking or stock broking services or for any other services from the subject company of this research report and / or; ii. Managed or co-managed public offering of the securities from the subject company of this research report and / or; iii. Received compensation for products or services other than investment banking, merchant banking or stock broking services from the subject company of this research report; ASL or any of its associates have not received compensation or other benefits from the subject company of this research report or any other third-party in connection with this report. Term& Term& Conditions Conditions: : This report has been prepared by ASL and is meant for sole use by the recipient and not for circulation. The report and information contained herein is strictly confidential and may not be altered in any way, transmitted to, copied or distributed, in part or in whole, to any other person or to the media or reproduced in any form, without prior written consent of ASL. The report is based on the facts, figures and information that are considered true, correct, reliable and accurate. The intent of this report is not recommendatory in nature. The information is obtained from publicly available media or other sources believed to be reliable. Such information has not been independently verified and no guaranty, representation of warranty, express or implied, is made as to its accuracy, completeness or correctness. All such information and opinions are subject to change without notice. The report is prepared solely for informational purpose and does not constitute an offer document or solicitation of offer to buy or sell or subscribe for securities or other financial instruments for the clients. Though disseminated to all the customers simultaneously, not all customers may receive this report at the same time. ASL will not treat recipients as customers by virtue of their receiving this report.

Disclaimer DEFINITION OF RATINGS DEFINITION OF RATINGS Ratings Ratings Expected absolute returns over 12 months Expected absolute returns over 12 months BUY BUY More than 10% HOLD HOLD Between 10% and -10% Disclaimer Disclaimer: : SELL SELL Less than -10% Nothing in this report constitutes investment, legal, accounting and tax advice or a representation that any investment or strategy is suitable or appropriate to the recipient’s specific circumstances. The securities and strategies discussed and opinions expressed, if any, in this report may not be suitable for all investors, who must make their own investment decisions, based on their own investment objectives, financial positions and needs of specific recipient. This report may not be taken in substitution for the exercise of independent judgment by any recipient. Each recipient of this report should make such investigations as it deems necessary to arrive at an independent evaluation of an investment in the securities of companies referred to in this report (including the merits and risks involved), and should consult its own advisors to determine the merits and risks of such an investment. Certain transactions, including those involving futures, options and other derivatives as well as non-investment grade securities involve substantial risk and are not suitable for all investors. ASL, its directors, analysts or employees do not take any responsibility, financial or otherwise, of the losses or the damages sustained due to the investments made or any action taken on basis of this report, including but not restricted to, fluctuation in the prices of shares and bonds, changes in the currency rates, diminution in the NAVs, reduction in the dividend or income, etc. Past performance is not necessarily a guide to future performance. Investors are advice necessarily a guide to future performance. Investors are advised to see Risk Disclosure Document to understand the risks associated before investing in the securities markets. Actual results may differ materially from those set forth in projections. Forward-looking statements are not predictions and may be subject to change without notice. ASL and its affiliated companies, their directors and employees may; (a) from time to time, have long or short position(s) in, and buy or sell the securities of the company(ies) mentioned herein or (b) be engaged in any other transaction involving such securities or earn brokerage or other compensation or act as a market maker in the financial instruments of the company(ies) discussed herein or act as an advisor or investment banker, lender/borrower to such company(ies) or may have any other potential conflict of interests with respect to any recommendation and other related information and opinions. Each of these entities functions as a separate, distinct and independent of each other. The recipient should take this into account before interpreting this document. The Research reports are also available & published on AxisDirect website. ASL and / or its affiliates do and seek to do business including investment banking with companies covered in its research reports. As a result, the recipients of this report should be aware that ASL may have a potential conflict of interest that may affect the objectivity of this report. Compensation of Research Analysts is not based on any specific merchant banking, investment banking or brokerage service transactions. ASL may have issued other reports that are inconsistent with and reach different conclusion from the information presented in this report. Neither this report nor any copy of it may be taken or transmitted into the United State (to U.S. Persons), Canada, or Japan or distributed, directly or indirectly, in the United States or Canada or distributed or redistributed in Japan or to any resident thereof. If this report is inadvertently sent or has reached any individual in such country, especially, USA, the same may be ignored and brought to the attention of the sender. This report is not directed or intended for distribution to, or use by, any person or entity who is a citizen or resident of or located in any locality, state, country or other jurisdiction, where such distribution, publication, availability or use would be contrary to law, regulation or which would subject ASL to any registration or licensing requirement within such jurisdiction. The securities described herein may or may not be eligible for sale in all jurisdictions or to certain category of investors. The Disclosures of Interest Statement incorporated in this document is provided solely to enhance the transparency and should not be treated as endorsement of the views expressed in the report. The Company reserves the right to make modifications and alternations to this document as may be required from time to time without any prior notice. The views expressed are those of the analyst(s) and the Company may or may not subscribe to all the views expressed therein. Copyright in this document vests with Axis Securities Limited. Axis Securities Limited, SEBI Single Reg. No.- NSE, BSE & MSEI – INZ000161633, ARN No. 64610, CDSL-IN-DP-CDSL-693-2013, SEBI-Research Analyst Reg. No. INH 000000297, SEBI Portfolio Manager Reg. No.- INP000000654, Main/Dealing off.- Unit No. 2, Phoenix Market City, 15, LBS Road, Near Kamani Junction, Kurla (west), Mumbai-400070, Tel No. – 18002100808, Reg. off.- Axis House, 8th Floor, Wadia International Centre, Pandurang Budhkar Marg, Worli, Mumbai – 400 025.Compliance Officer: Anand Shaha, E-Mail ID: compliance.officer@axisdirect.in,Tel No: 022-42671582.