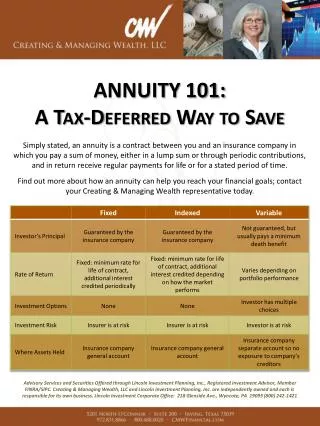

Deferred Tax Examples

Acct 414. Deferred Tax Examples. Nice to have on paper as we work problems during class. Fundamentals of Accounting for Income Taxes.

Deferred Tax Examples

E N D

Presentation Transcript

Acct 414 Deferred Tax Examples Nice to have on paper as we work problems during class

Fundamentals of Accounting for Income Taxes Illustration Assume the company reports revenue in 2007, 2008, and 2009 of $130,000, respectively. The revenue is reported the same for both GAAP and tax purposes. For simplification, assume the company reports one expense, depreciation, over the three years applying the straight-line method for financial reporting purposes (GAAP) and MACRS (IRS) for the tax return. What is the effect on the accounts of using the two different depreciation methods? LO 1 Identify differences between pretax financial income and taxable income.

Book vs. Tax Difference GAAP Reporting 2007 2008 2009 Total Revenues $130,000 $130,000 $130,000 $390,000 Expenses (S/L depreciation) 30,000 30,000 30,000 90,000 Pretax financial income $100,000 $100,000 $100,000 $300,000 Income tax expense (40%) $40,000 $40,000 $40,000 $120,000 Tax Reporting 2007 2008 2009 Total Revenues $130,000 $130,000 $130,000 $390,000 Expenses (MACRS depreciation) 40,000 30,000 20,000 90,000 Pretax financial income $90,000 $100,000 $110,000 $300,000 Income tax payable (40%) $36,000 $40,000 $44,000 $120,000 LO 1 Identify differences between pretax financial income and taxable income.

Example – Deferred Tax Liability • Assume that Sales Company recognizes $15,000 gross profit from installment sales for financial accounting in 2006. The gross profit will be taxable at $3,000 each year for the next five years. The company earns $10,000 additional income each year and the tax rate is 40%. The following schedule shows taxable income, income tax payable, financial income, and income tax expense for the five year period.

Example – Deferred Tax Asset Financial Magazine Company received $15,000 of subscriptions in advance for 2006. Subscription revenue will be recognized equally in 2007, 2008, and 2009, for financial accounting purposes but all of the $15,000 will be recognized in 2006 for tax purposes. There is additional income of $50,000 each year and the tax rate is 40%.

South Carolina Corporation E19-1South Carolina Corporation has one temporary difference at the end of 2007 that will reverse and cause taxable amounts of $55,000 in 2008, $60,000 in 2009, and $65,000 in 2010. South Carolina’s pretax financial income for 2007 is $300,000, and the tax rate is 30% for all years. There are no deferred taxes at the beginning of 2007. Instructions • Compute taxable income and income taxes payable for 2007. • Prepare the journal entry to record income tax expense, deferred income taxes, and income taxes payable for 2007.

Columbia Corporation Columbia Corporation has one temporary difference at the end of 2007 that will reverse and cause deductible amounts of $50,000 in 2008, $65,000 in 2009, and $40,000 in 2010. Columbia’s pretax financial income for 2007 is $200,000 and the tax rate is 34% for all years. There are no deferred taxes at the beginning of 2007. Columbia expects to be profitable in the future. Instructions • Compute taxable income and income taxes payable for 2007. • Prepare the journal entry to record income tax expense, deferred income taxes, and income taxes payable for 2007.

Zoop Inc. (NOL) Zoop Inc. incurred a net operating loss of $500,000 in 2007. Taxable income was $200,000 for 2005 and $200,000 for 2006. The tax rate for all years is 40%. Zoop elects the carryback option. Prepare the journal entries to record the benefits of the loss carryback and the loss carryforward.

Zoop Inc. (Variation) Now assume that it is more likely than not that the entire net operating loss carryforward will not be realized by Zoop Inc. in future years. Prepare all the journal entries necessary at the end of 2007.

Valis Corporation (NOL) Valis Corporation had the following tax information. In 2007 Valis suffered a net operating loss of $450,000, which it elected to carry back. The 2007 enacted tax rate is 29%. Prepare Valis’s entry to record the effect of the loss carryback.

Example: Revision of Future Tax Rate At the end of 2002, the corporate tax rate is changed from 40% to 35%. The new rate is effective January 1, 2004. The deferred tax account (1/1/2002) is as follows: Excess tax depreciation: $3 million Deferred tax liability: $1.2 million Related taxable amounts are expected to occur equally over 2003, 2004, and 2005. Provide the journal entry to reflect the change.

Review Problem Zurich Company reports pretax financial income of $70,000 for 2007. The following items cause taxable income to be different than pretax financial income. (1) Depreciation on the tax return is greater than depreciation on the income statement by $16,000. (2) Rent collected on the tax return is greater than rent earned on the income statement by $22,000. (3) Fines for pollution appear as an expense of $11,000 on the income statement. Zurich’s tax rate is 30% for all years, and the company expects to report taxable income in all future years. There are no deferred taxes at the beginning of 2007. Instructions Prepare the journal entry to record income tax expense, deferred income taxes, and income taxes payable for 2007.